Get Certified for

Capital Markets (CMSA®)

From equities and fixed income to derivatives, the CMSA certification bridges the gap from where you are now to where you want to be — a world-class capital markets analyst.

A series of expansion and contraction in economic activity

A business cycle is a cycle of fluctuations in the Gross Domestic Product (GDP) around its long-term natural growth rate. It explains the expansion and contraction in economic activity that an economy experiences over time.

A business cycle is completed when it goes through a single boom and a single contraction in sequence. The time period to complete this sequence is called the length of the business cycle.

A boom is characterized by a period of rapid economic growth, whereas a period of relatively stagnated economic growth is a recession. These are measured in terms of the growth of the real GDP, which is inflation-adjusted.

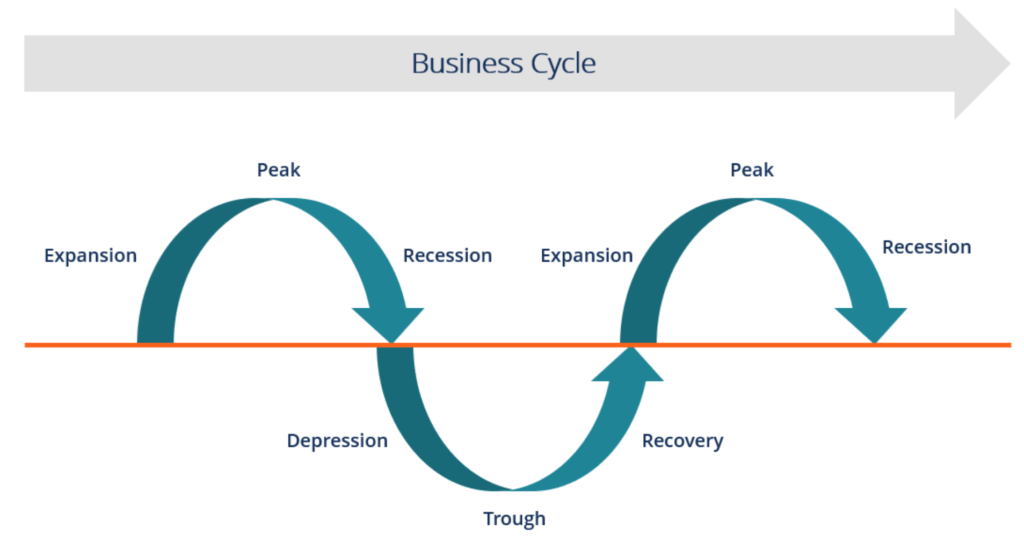

In the diagram above, the straight line in the middle is the steady growth line. The business cycle moves about the line. Below is a more detailed description of each stage in the business cycle:

The first stage in the business cycle is expansion. In this stage, there is an increase in positive economic indicators such as employment, income, output, wages, profits, demand, and supply of goods and services. Debtors are generally paying their debts on time, the velocity of the money supply is high, and investment is high. This process continues as long as economic conditions are favorable for expansion.

The economy then reaches a saturation point, or peak, which is the second stage of the business cycle. The maximum limit of growth is attained. The economic indicators do not grow further and are at their highest. Prices are at their peak. This stage marks the reversal point in the trend of economic growth. Consumers tend to restructure their budgets at this point.

The recession is the stage that follows the peak phase. The demand for goods and services starts declining rapidly and steadily in this phase. Producers do not notice the decrease in demand instantly and go on producing, which creates a situation of excess supply in the market. Prices tend to fall. All positive economic indicators such as income, output, wages, etc., consequently start to fall.

There is a commensurate rise in unemployment. The growth in the economy continues to decline, and as this falls below the steady growth line, the stage is called a depression.

In the depression stage, the economy’s growth rate becomes negative. There is further decline until the prices of factors, as well as the demand and supply of goods and services, contract to reach their lowest point. The economy eventually reaches the trough. It is the negative saturation point for an economy. There is extensive depletion of national income and expenditure.

After the trough, the economy moves to the stage of recovery. In this phase, there is a turnaround in the economy, and it begins to recover from the negative growth rate. Demand starts to pick up due to low prices and, consequently, supply begins to increase. The population develops a positive attitude towards investment and employment and production starts increasing.

Employment begins to rise and, due to accumulated cash balances with the bankers, lending also shows positive signals. In this phase, depreciated capital is replaced, leading to new investments in the production process. Recovery continues until the economy returns to steady growth levels.

This completes one full business cycle of boom and contraction. The extreme points are the peak and the trough.

John Keynes explains the occurrence of business cycles is a result of fluctuations in aggregate demand, which bring the economy to short-term equilibriums that are different from a full-employment equilibrium.

Keynesian models do not necessarily indicate periodic business cycles but imply cyclical responses to shocks via multipliers. The extent of these fluctuations depends on the levels of investment, for that determines the level of aggregate output.

In contrast, economists like Finn E. Kydland and Edward C. Prescott, who are associated with the Chicago School of Economics, challenge the Keynesian theories. They consider the fluctuations in the growth of an economy not to be a result of monetary shocks, but a result of technology shocks, such as innovation.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.