Perfect Competition

A market wherein both producers and consumers are price-takers

What is Perfect Competition?

In a market with perfect competition, both producers and consumers are price-takers. Such a characteristic implies production and consumption decisions that individual producers and consumers face do not affect the market price of the good or service.

A perfectly competitive market can be characterized as a market where there is an abundance of well-informed buyers and sellers, there is an absence of monopolies, and each firm is a price-taker.

Summary

- A perfectly competitive market is defined by both producers and consumers being price-takers. Price-takers are unable to affect the market price because they lack substantial market share.

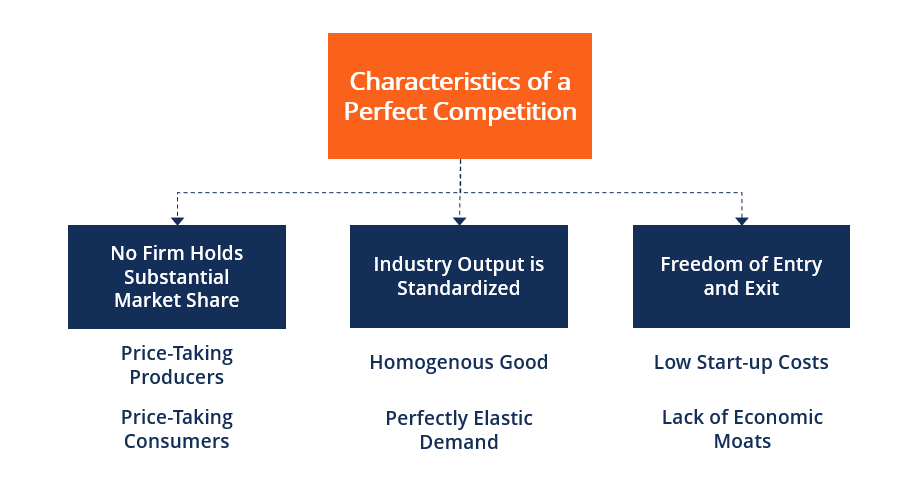

- The three primary characteristics of perfect competition are (1) no company holds a substantial market share, (2) the industry output is standardized, and (3) there is freedom of entry and exit.

- The efficient market equilibrium in a perfect competition is where marginal revenue equals marginal cost.

What are Price-Takers?

Price-takers are market participants that are unable to affect the market price of goods through their production and consumption decisions. The two types of price-takers are:

1. Price-taking producers

A price-taking producer is a producer that cannot affect the market price of the product or service they are selling.

2. Price-taking consumer

A price-taking consumer is a consumer that cannot affect the market price of a good or service.

Prerequisites of Perfect Competition

1. No individual firm possesses a substantial market share

For an industry to be perfectly competitive, no individual producers must have a large market share. Market share is the proportion of the total industry’s output that belongs to a single firm.

For example, consider the wheat market. Many farmers grow wheat, and market share is dispersed among them. There are no farmers that could potentially affect the price of wheat on the market.

2. The industry output is a standardized product

Perfect competition can only occur when consumers perceive the products of all producers to be equivalent. Therefore, it can only occur when the industry output is a commodity, otherwise known as a standardized product.

Since standardized products are homogenous, a single producer cannot increase the price of their good or service without losing all sales to the competition. It implies that price-taking firms face perfect price-elasticity of demand.

3. Freedom of entry and exit

The majority of perfectly competitive industries allow firms to easily enter and exit the industry. The arrival of new firms into an industry is referred to as market entry. Market entry is enabled by the absence of obstacles posed by government regulation or low start-up costs.

The departure of firms out of an industry is referred to as a market exit. Firms can easily exit the market if there are no additional costs attributable to shutting down the business. For example, consider the mining industry.

In the mining industry, firms must recognize an Asset Retirement Obligation (ARO) to restore the property to its previous state after the desired metals are extracted. An ARO refers to a liability that is amortized throughout the investment horizon and exemplifies an exit cost for mining firms.

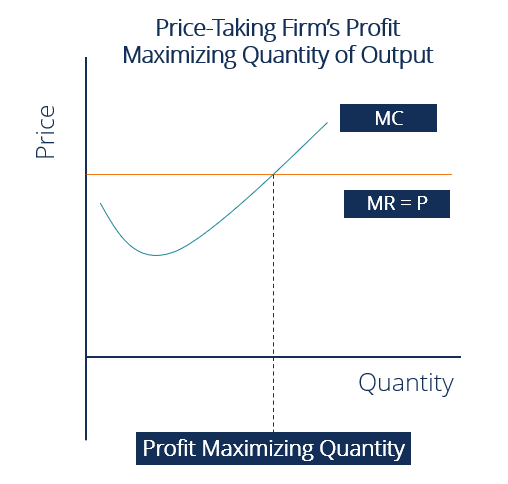

Optimal Production Output in a Perfect Competition

In order for firms to generate maximum profits, they must determine their optimal output to produce. In a perfect competition, firms produce an output quantity where the marginal cost of the last unit produced is equal to the marginal revenue of the product.

For a price-taking firm, the marginal revenue is equal to the market price. It is because no firm can affect the market price; therefore, the additional revenue generated by producing one more unit is the market price.

Consequently, an individual firm faces a perfectly elastic demand curve. The price-taking firm’s demand curve is equal to its marginal revenue. The demand and marginal revenue curve can be illustrated by a horizontal line drawn at the market price.

Example of Market Equilibrium in a Perfect Competition

Consider a wheat farmer who intends to sell his wheat to customers. The current market price of wheat is $100 a bushel. The farmer’s marginal cost function is:

MC = 25 + 2.5Q

Given the market price and the farmer’s marginal cost function, what is the profit-maximizing quantity to produce?

100 = 25 + 2.5Q

Q = 30

Therefore, the farmer should produce 30 bushels of wheat.

Related Readings

CFI is the official provider of the Commercial Banking & Credit Analyst (CBCA)™ certification program, designed to transform anyone into a world-class financial analyst.

In order to help you become a world-class financial analyst and advance your career to your fullest potential, these additional resources will be very helpful: