Get Certified for

Commercial Banking (CBCA®)

Stand out and gain a competitive edge as a commercial banker, loan officer, or credit analyst with advanced knowledge, real-world analysis skills, and career confidence.

The ability to take on and repay corporate debts

Debt capacity refers to the total amount of debt a business can incur and repay according to the terms of a debt agreement. A business takes on debt for several reasons – such as boosting production or marketing, expanding capacity, or acquiring new businesses. However, incurring too much debt or taking on the wrong type can result in damaging consequences.

How do lenders make decisions on which businesses to lend their money to? In this article, we will explore the most commonly used financial metrics to evaluate how much leverage a business can handle. At the end of the day, lenders wish to have comfort and confidence in lending their money to businesses that can internally generate enough earnings and cash flow to not only pay the interest but also the principal balance.

Source: CFI’s free Introduction to Corporate Finance course.

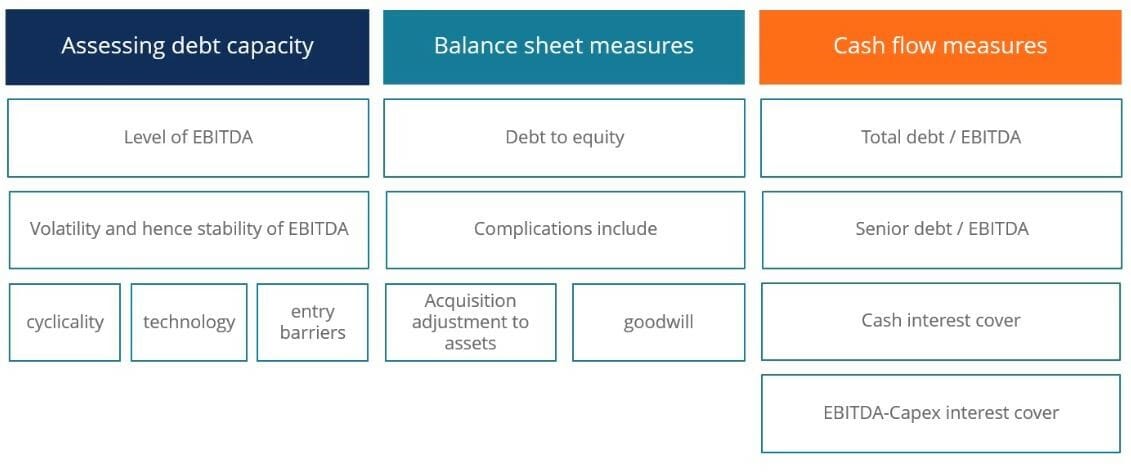

The two main measures to assess a company’s debt capacity are its balance sheet and cash flow measures. By analyzing key metrics from the balance sheet and cash flow statements, investment bankers determine the amount of sustainable debt a company can handle in an M&A transaction.

One measure to evaluate debt capacity is EBITDA, or Earnings Before Interest, Tax, Depreciation, and Amortization. To learn more about EBITDA, please see our EBITDA Guide.

The level of EBITDA is important to assess the debt capacity, as companies with higher levels of EBITDA can generate more earnings to repay their debt. Hence, the higher the EBITDA level, the higher the debt capacity. However, although the level of EBITDA is crucial, the stability of a company’s EBITDA level is also important in assessing its debt capacity. There are a few factors that contribute to a company’s EBITDA stability – cyclicality, technology, and barriers to entry.

Cyclical businesses inherently have less debt capacity than non-cyclical businesses. For example, mining businesses are cyclical in nature due to their operations, whereas food businesses are much more stable. From a lender’s point of view, volatile EBITDA represents volatile retained earnings and the ability to repay debt, hence a much higher default risk.

Industries with low barriers to entry also have less debt capacity compared to industries with high barriers to entry. For example, tech companies that have low barriers to entry can easily be disrupted as competition enters. Even if tech companies are legally protected through patents and copyrights, competition will eventually enter as the patent term expires or with newer and more efficient innovations. On the other hand, industries with high barriers to entry, such as long-term infrastructure projects, are less likely to be disrupted by new entrants and, therefore, can sustain a more stable EBITDA.

Learn more in CFI’s free introduction to corporate finance course.

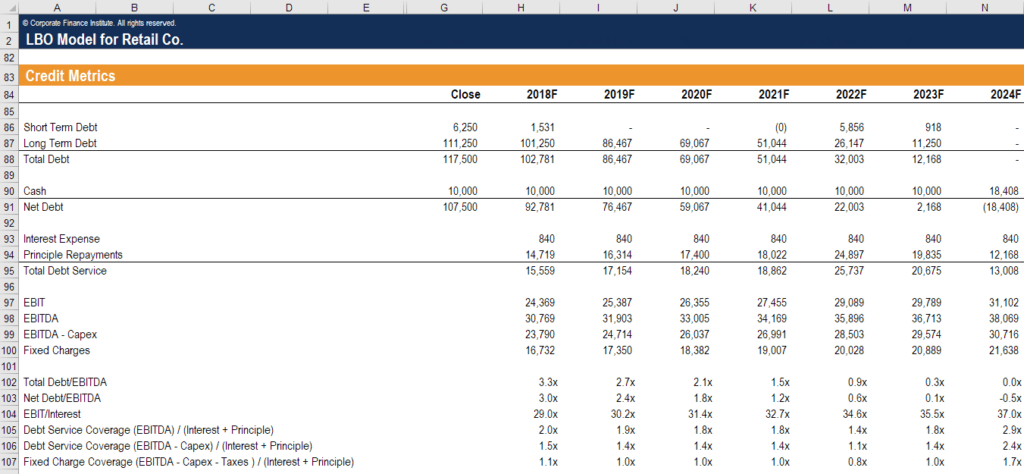

Credit metrics are extremely useful to determine debt capacity, as they directly reflect the book values of assets, liabilities, and shareholder equity. The most commonly used balance sheet measure is the debt-to-equity ratio. Other common metrics include debt/EBITDA, interest coverage, and fixed-charge coverage ratios.

As you can see in the screenshot from CFI’s financial modeling course below, an analyst will look at all of these credit metrics in assessing a company’s debt capacity.

Debt-to-equity ratios provide investment bankers with a high-level overview of a company’s capital structure. However, this ratio can be complicated, as there can be a discrepancy between the book value and the market value of equity. Acquisitions, adjustments to assets, goodwill, and impairment are all influential factors that may create a discrepancy between the book value and market value of debt-to-equity ratios.

Another set of measures investment bankers use to assess debt capacity is cash flow metrics. These metrics include total debt-to-EBITDA, which can be broken down further to senior debt-to-EBITDA, cash interest coverage, and EBITDA-Capital Expenditures interest coverage.

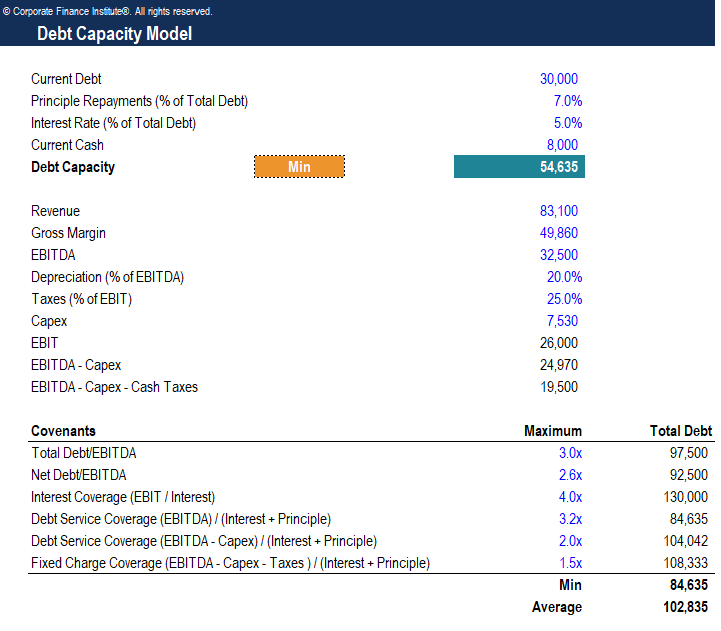

The Debt-to-EBITDA measure is the most common cash flow metric to evaluate debt capacity. The ratio demonstrates a company’s ability to pay off its incurred debt and provides investment bankers with information on the amount of time required to clear all debt, ignoring interest, taxes, depreciation, and amortization. Total debt-to-EBITDA can be broken down into the senior or subordinated debt-to-EBITDA metric, which focuses on debt that a company must repay first in the event of distress.

The cash interest coverage measure depicts how many times the cash flow generated from business operations can service the interest expense on the debt. This is a key metric, as it shows not only a company’s ability to pay interest but also its ability to repay principal.

Learn more in CFI’s free introduction to corporate finance course.

By taking the EBITDA, deducting capital expenditures, and examining how many times this metric can cover the interest expense, investment bankers can assess a company’s debt capacity. This metric is specifically useful for companies with high capital expenditures, including manufacturing and mining firms.

The fixed-charge coverage ratio is equal to a company’s EBITDA – CapEx – Cash Taxes – Distributions. The ratio is very close to a true cash flow measure and thus very relevant for assessing debt capacity.

Download CFI’s free Excel template now to advance your finance knowledge and perform better financial analysis.

Thank you for reading CFI’s guide to Debt Capacity. To help you advance your career, check out the additional CFI resources below: