Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

Calculates the amount of time that it will take for a project to "break even"

The discounted payback period is a modified version of the payback period that accounts for the time value of money. Both metrics are used to calculate the amount of time that it will take for a project to “break even,” or to get the point where the net cash flows generated cover the initial cost of the project. Both the payback period and the discounted payback period can be used to evaluate the profitability and feasibility of a specific project.

Other metrics, such as the internal rate of return (IRR), profitability index (PI), net present value (NPV), and effective annual annuity (EAA) can also be used to quantify the profitability of a given project. To make the best decision about whether to pursue a project or not, a company’s management needs to decide which metrics to prioritize.

Management then looks at a variety of metrics in order to obtain complete information. Usually, companies are deciding between multiple possible projects. Comparing various profitability metrics for all projects is important when making a well-informed decision.

The discounted payback period is used to evaluate the profitability and timing of cash inflows of a project or investment. In this metric, future cash flows are estimated and adjusted for the time value of money. It is the period of time that a project takes to generate cash flows when the cumulative present value of the cash flows equals the initial investment cost.

The shorter the discounted payback period, the quicker the project generates cash inflows and breaks even. While comparing two mutually exclusive projects, the one with the shorter discounted payback period should be accepted.

There are two steps involved in calculating the discounted payback period. First, we must discount (i.e., bring to the present value) the net cash flows that will occur during each year of the project.

Second, we must subtract the discounted cash flows from the initial cost figure in order to obtain the discounted payback period. Once we’ve calculated the discounted cash flows for each period of the project, we can subtract them from the initial cost figure until we arrive at zero.

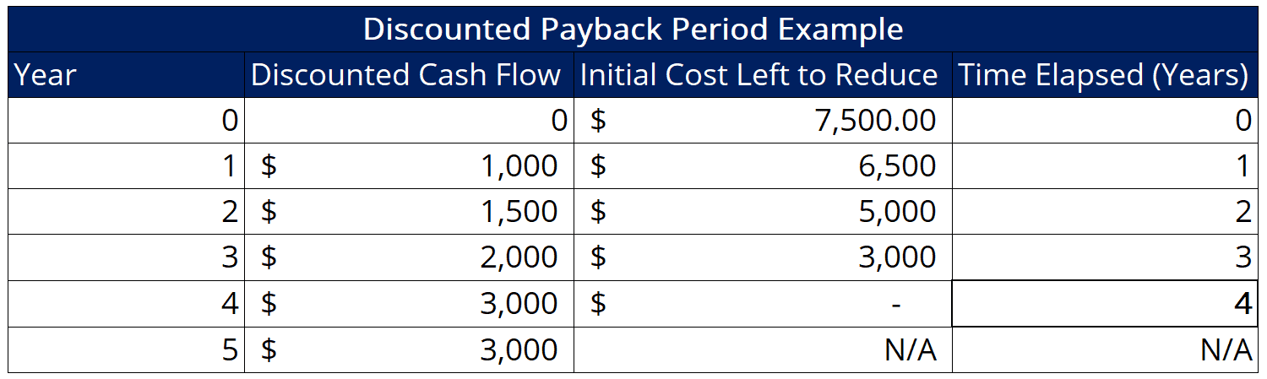

Assume a business that is considering a given project. Below are some selected data from the discounted cash flow model created by the company’s financial analysts:

As we can see here, the project returns a positive discounted cash flow in its first year and sees its yearly discounted cash flow grow to $3,000 in later years. We also learn that the project cost is $7,500. Using the given information, we can calculate the discounted payback period as follows:

In this case, we see that the project’s payback period is 4 years. Since the project’s life is calculated at 5 years, we can infer that the project returns a positive NPV. Thus, the project will likely add value to the business if pursued.

One observation from the example above is that the project’s discounted payback period is reached exactly at the end of a year. Obviously, that may not always be the case. In other circumstances, we may see projects where the payback occurs during, rather than at the end of, a given year.

In such situations, we will first take the difference between the year-end cash flow and the initial cost remaining to be reduced. Next, we divide the number by the year-end cash flow to get the percentage of the remaining time period after the project has been paid back.

The next step is to subtract the number from 1 to obtain the percent of the year at which the project is paid back. Finally, we proceed to convert the percentage in months (e.g., 25% would be 3 months, etc.) and add the figure to the last year in order to arrive at the final discounted payback period number.

The discounted payback period indicates the profitability of a project while reflecting the timing of cash flows and the time value of money. It helps a company to determine whether to invest in a project or not. If the discounted payback period of a project is longer than its useful life, the company should reject the project.

One of the disadvantages of discounted payback period analysis is that it ignores the cash flows after the payback period. Thus, it cannot tell a corporate manager or investor how the investment will perform afterward and how much value it will add in total. It may lead to decisions that contradict the NPV analysis.

A project may have a longer discounted payback period but also a higher NPV than another if it creates much more cash inflows after its discounted payback period. Such an analysis is biased against long-term projects.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

We hope you enjoyed reading CFI’s explanation of the Discounted Payback Period. To keep learning and advancing your career, the following CFI resources will be helpful: