Get Certified for

Financial Planning & Wealth Management Professional (FPWMP®)

Learn financial analysis & planning, portfolio management, and risk assessment.

Premiums earned on the portion of an expired insurance contract

An earned premium represents premiums earned on the portion of an insurance contract that has expired. The premiums associated with the active portion of an insurance contract are considered unearned, as the insurance company is still taking on a risk in order to generate the premiums.

When an insurance company writes an insurance contract, they assume financial risk during the time of that contract. For example, if you buy insurance on your car and your car is hit and damaged, the insurer would need to pay a certain amount of money towards paying for that damage.

For this reason, insurance companies consider premiums on an insurance contract unearned until the contract has expired. Once the contract has expired, the insurance company is no longer assuming any financial risk, and the premium is considered earned.

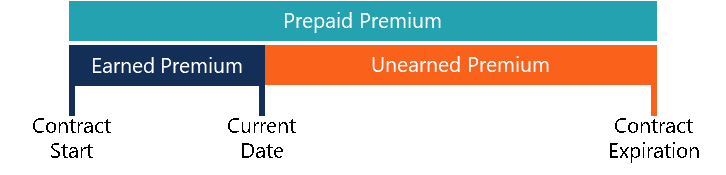

The diagram above can help to understand how earned premiums work. While the insurer might have collected a prepaid premium on the contract start date, the earned premium is only the pro-rated amount of that premium until the current date.

Unearned premiums are premiums that have been collected by the insurance company, where the underlying portion of the insurance contract has not expired. In the case that the contract is ended prematurely, the premiums would be returned to the policyholder.

For example, assume that a customer bought a one-year auto insurance policy and prepaid for six months of premiums at $100 per month. However, after one month, the car figures in an accident, requiring the insurer to reimburse the policyholder. The insurer makes $100 as earned premiums and returns $500 to the insured party as unearned premiums.

There are two main methods for calculating the earned premium:

The accounting method takes the number of days since the beginning of an insurance contract and multiplies the figure by the premium earned each day. It is the most common method for calculating earned premium and accurately reflects the amounts insurance companies made on specific contracts.

The exposure method is much more complex and data-driven than the accounting method. It uses historical data to estimate the value of insurance contracts. It looks at the risk of payout and the estimated collection of premiums.

Assume an insurer writes a one-year auto insurance contract with a premium of $100 per month. The policyholder prepays for six months worth of premiums. After three months, what would the earned premium be under the accounting method and the exposure method?

Using the accounting method, you would simply multiply the monthly premium by the number of months expired. Therefore, the earned premium would be $300 (3 months x $100/month). The remainder amount of prepaid premiums would be returned to the policyholder and would be considered unearned premiums ($300).

Using the exposure method, the customer would need to look at historical risk levels. If the company decided that the chance of payout of the given contract is 5% with a payout of $1,000, the level of risk would need to be factored into the earned premium calculation by looking at the unearned portion.

$1,000 x 5% = $50 and $100 x 95% = $95; $45 (the difference between the expected value of premium earned and the expected value of payouts) would be the insurer’s monthly expected value of profit from the insurance policy.

While the above examples of calculating earned premiums can help consumers to understand them, they are simplifications of models that are used by insurers. Insurance companies continue to become more accurate and data-driven in the way they structure policies.

Additionally, insurance contracts contain stipulations that can void them and affect earned premiums. For example, if a customer took out a life insurance policy and didn’t specify a serious medical condition, the contract would be void. Therefore, the insurer would keep the unearned premiums as earned premiums.

To keep advancing your career, the additional resources below will be useful: