Get Certified for

Capital Markets (CMSA®)

From equities and fixed income to derivatives, the CMSA certification bridges the gap from where you are now to where you want to be — a world-class capital markets analyst.

When investors in equity shares fail to comply with pre-specified purchase agreements or restrictions

Forfeited shares often result from when investors in equity shares fail to comply with pre-specified purchase agreements or restrictions. The end result of share forfeiture is that the shareholder no longer needs to comply with the pre-specified purchase agreement or restrictions but loses the opportunity to realize gains on their equity stake.

Moreover, the shareholder will not possess the right to recover their previous expenditure on the equity. Forfeited shares are a common by-product of employee stock option plans.

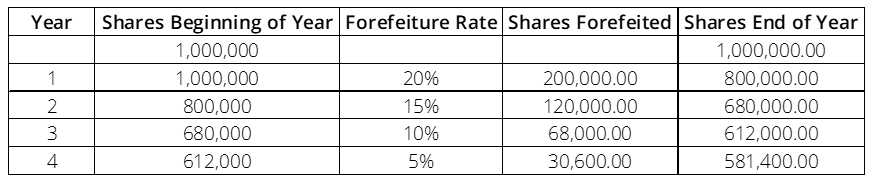

The forfeiture rate refers to the percentage of options that you expect to cancel in a year based on historical cancellation data. For every year that options are granted, you must estimate the forfeitures for the following four years. The amount of forfeitures generally trends downwards after every year.

For example, consider that you grant options for the equivalent of one million shares in 2020, and in the first year of vesting (2021), approximately 20% of the shares are forfeited. The estimated forfeiture rates from historical data of years 2, 3, and 4 are 15%, 10%, and 5%, respectively.

Therefore, at the date of options granting, the estimated shares to be forfeited in a four-year period are 200,000 + 120,000 + 68,000 + 30,600 = 418,600

The forfeiture rate is applied to the shares at the beginning of the year to calculate the number of shares forfeited. The difference between shares at the beginning of the year and shares forfeited will equal the shares at the end of the year.

When a corporation is expensing a stock option, two major steps must be followed:

The FAST defines fair value as the price that would be realizable at the sale of an asset or the amount paid to transfer a liability between market participants at the measurement date. Therefore, the fair value is the price at which the option would be purchased in an open market at the measurement date.

There are several ways to calculate an option’s fair value – a few methods include:

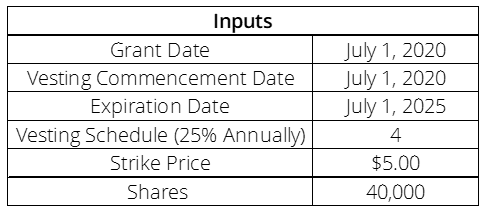

The most commonly applied method is the Black Scholes Merton Model because of its relative simplicity. In the Black Scholes Merton model, you require five inputs. The inputs are:

Utilizing the Black Scholes Calculator template provided by the Corporate Finance Institute found here, we find that the fair value of the option is $1.60.

The next step is to find the total expense, which can be calculated as $1.60 * 40,000 = $64,000. The expense is now recorded over the useful economic life of the option grant. Here, we know that the period is 5 years. The most common way to allocate the expense is through the straight-line allocation method.

The percentage of economic life passed each year is a fifth of the total 5-year life. The proportion is applied to the total stock-based compensation expense.

If the employee receiving stock-based compensation is terminated from their role before the shares vest, it creates complexity in financial reporting. However, expenses are not final until the options vest, but once vested, the expense is final. It is where the vested options are considered as “earned,” and the employee should be compensated because they have the right to exercise.

If an employee is terminated or leaves the company, the future stock-based compensation will not be incurred. Generally accepted accounting principles allows companies to apply a forfeiture rate – usually based on historical rates – to any expense associated with unvested shares that are being expensed.

CFI is the official provider of the global Capital Markets & Securities Analyst (CMSA)® certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional CFI resources below will be useful: