Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

A decision-making tool used to assess financial information and derive a decision between two or more alternatives

Incremental analysis (also referred to as the relevant cost approach, marginal analysis, or differential analysis) is a decision-making tool used to assess financial information and derive a decision between two or more alternatives.

Incremental analysis is used by businesses to analyze any existing cost differences between different alternatives. The method incorporates accounting and financial information in the decision-making process and allows for the projection of outcomes for various alternatives and outcomes. Through incremental analysis, the revenues, costs, and possible outcomes of the alternatives can be identified.

The example below briefly illustrates the concept of incremental analysis; however, the analysis process can be more complex depending on the scenario at hand.

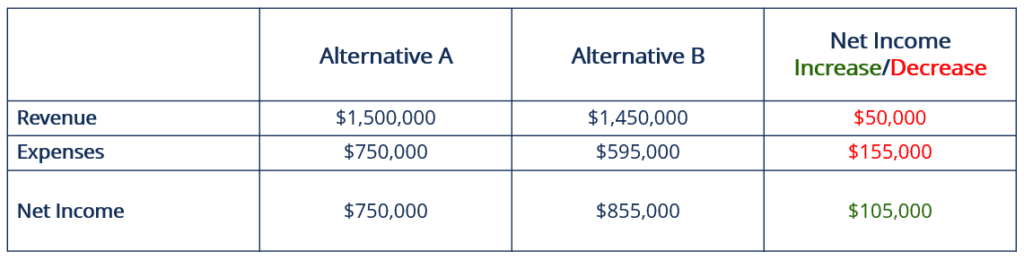

Company ABC is considering and evaluating two new business segments to add to their existing revenue streams. For educational purposes, these two segments will be called Alternative A and Alternative B, with the following information:

The revenues for each segment are $1.5 million and $1.45 million, respectively. The expenses for each segment amount to $750,000 and $595,000, respectively. To determine which segment is more attractive in the long run, the net income must be calculated, as seen in the diagram below:

Alternative A reports a net income amounting to $750,000, while Alternative B’s net income totals $855,000. Based purely on the available financial information, the management team should decide to take on Alternative B as a new and/or additional segment.

Another example can be seen below:

A company receives an order from a customer for 1,000 units of a green widget for $12 each. The company controller looks up the standard cost for a green widget and finds that it costs the company $14. Of the $14, $11 is variable cost and $3 is fixed cost.

Since the fixed cost is being incurred regardless of the proposed sale, it is classified as a sunk cost and ignored. It means that the incremental cost of the widget is $11. The company should accept the order since it will earn $1 ($12-$11) per unit sold, or $1,000 in total.

To fully comprehend the concept of incremental analysis, one has to understand its underlying concepts. The three main concepts are relevant cost, sunk cost, and opportunity cost.

The concept of relevant cost describes the costs and revenues that vary among respective alternatives and do not include revenues and costs that are common between alternatives. The revenues that are generated between different alternatives are referred to as relevant benefits in some studies or texts.

Relevant costs are also referred to as avoidable costs or differential costs. For a cost to be considered a “relevant cost,” it must be incremental, result in a change in cash flow, and be likely to change in the future. Hence, a relevant cost arises due to a particular management decision. The concept does not apply to financial accounting but can be applied to management accounting.

The concept of sunk costs describes a cost that’s already been incurred and does not impact any decision made by management or between alternatives. The cost is unlikely to increase in the future or disappear completely. Other terms that refer to sunk costs are sunk capital, embedded cost, or prior year cost.

The concept of opportunity cost describes the reward or loss resulting from a decision made between respective alternatives.

The opportunity cost refers to the value of what is lost when a decision between two or more alternatives is made. Hence, opportunity cost is “the loss taken to make a gain, or the loss of one gain for another gain.”

Since incremental analysis makes use of financial information to derive decisions, the following are examples of scenarios to which incremental analysis can be applied:

CFI is the official provider of the Financial Modeling & Valuation Analyst (FMVA®) certification program, designed to transform anyone into a world-class financial analyst.

In order to help you become a world-class financial analyst and advance your career to your fullest potential, these additional resources will be very helpful: