Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

A profitability measure that assesses the profit or loss generated by a particular product, line of business, or geographic location

Segment margin is a profitability measure that assesses the profit or loss generated by a particular product line of a business, or a particular geographic location. The segment margin is mainly used to compare the profitability of different components of a company. The measure is extremely helpful for large companies with several business lines or that maintains a presence in numerous geographic regions.

From the analysis of the segment margins, the company’s management may identify the strength or weakness of each business component. The analysis of segment margins can be helpful even if the company is profitable overall. It can help address the issues of business segments with lower-than-average profitability or whose profitability has experienced a significant decline.

Segment margin analysis is valuable for management’s decision-making, as it helps to evaluate past management decisions and to identify major operating problems within different segments of the company.

Most publicly-traded companies disclose their financial results according to business segments and geographic locations. The information is disclosed on the company’s reports or regulatory filings (e.g., 10-K).

The segment margin is calculated using the following formula:

![]()

or

The revenues and costs used in the calculation of the segment margin should be attributable to the segment. It is not recommended to include costs traceable to overall corporate expenses, since those costs are usually irrelevant to the operations of a segment. Inclusion of the corporate costs can distort the calculations of the segment margin and the conclusions drawn from it.

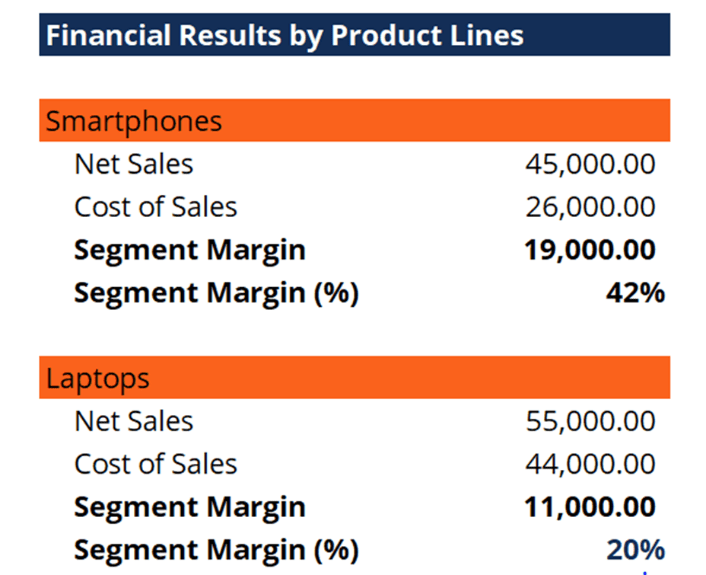

Orange Inc. is a technology company that produces two main products: smartphones and laptops. The table below is the summary of the company’s financial results broken down by products:

Due to intense competition in the market, the company decided to improve operations by investing more in one of the product lines. To choose the most suitable product line, the management chose to evaluate the segment margins of each product line.

Based on the company’s segment analysis, it is obvious that the smartphones offer a much larger segment margin (42%) than the laptops (20%). Investing in the smartphone product line is a better option than investing in the laptop product line because the former will generate larger profits.

CFI is the official provider of the Financial Modeling and Valuation Analyst (FMVA)™ certification program, designed to transform anyone into a world-class financial analyst. To keep learning and developing your knowledge of financial analysis, we highly recommend the additional CFI resources below:

Below is a break down of subject weightings in the FMVA® financial analyst program. As you can see there is a heavy focus on financial modeling, finance, Excel, business valuation, budgeting/forecasting, PowerPoint presentations, accounting and business strategy.

A well rounded financial analyst possesses all of the above skills!

CFI is the global institution behind the financial modeling and valuation analyst FMVA® Designation. CFI is on a mission to enable anyone to be a great financial analyst and have a great career path. In order to help you advance your career, CFI has compiled many resources to assist you along the path.

In order to become a great financial analyst, here are some more questions and answers for you to discover: