Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

Public disclosures about public companies

SEC filings are financial statements, periodic reports, and other formal documents that public companies, broker-dealers, and insiders are required to submit to the U.S. Securities and Exchange Commission (SEC).

The SEC was created in the 1930s with the aim to curb stock manipulation and fraud that was taking place among companies. The regulatory body collects financial and operational information of publicly traded domestic and foreign companies. It verifies the information contained in submitted SEC forms to ensure that it meets the set standards.

By making it mandatory for publicly traded companies to make SEC filings, the US government enables investors to review a company’s history and forecast future performance. Investors and finance professionals rely on these filings to get reliable information about companies that they are evaluating for investment purposes. This helps investors to make informed investment decisions when planning to sell, buy, or hold a company’s securities.

The following are the most common types of SEC filings:

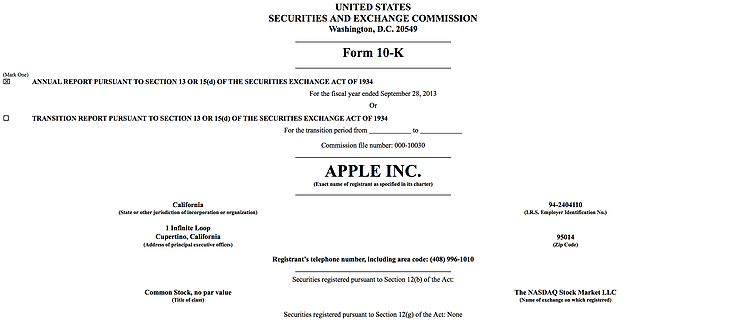

Form 10-K is a report that provides a comprehensive summary of a company’s performance for the year. It is more detailed than the annual report that is sent to shareholders during the annual meeting to elect directors. The form outlines the company’s history, equity, subsidiaries, organizational structure, audited financial statements, and other relevant information. Companies are required to submit this filing within 90 days after the end of their fiscal year.

The 10-K is organized in a way that makes it easy to consistently find the same information across multiple companies in the same place on each form. The main sections include:

Part I provides an overview of the company’s business and the risk factors that investors should know when investing in the company. In this section, the company should disclose any material legal proceedings that the firm is part of or to which any of the company’s property is subject. Also, this section should disclose any unresolved comments from SEC staff about the company’s report(s) in prior periods. If applicable, the company should provide information concerning mine safety violations or other regulatory issues.

Part II provides a comparative presentation of financial data for the five immediately prior years, making it easy for investors to measure the company’s latest performance against past data. It also includes the audited financial statements reviewed by a registered CPA firm.

The financial statements comprise the independent auditor’s report, a consolidated balance sheet, a consolidated statement of operations, and other accounting reports and notes. The management discussion and analysis of the company’s performance provides a clear overview of the financial and operational issues that influenced the operational results.

Part III includes material disclosures relating to directors, executive officers, executive compensation, and corporate governance. Firms should also reveal the beneficial ownership of management and significant shareholders, certain relationships and related transactions, director’s independence, and accountant fees and services.

Companies should list the financial statements, schedules, and exhibits that are filed in Part II. The exhibits include all material contracts, the company’s organizational documents, a list of significant subsidiaries, and applicable certifications. Also, this is where the management — CEO, CFO, and members of the board of directors — append their signatures, certifying that the SEC 10-K filing is accurate.

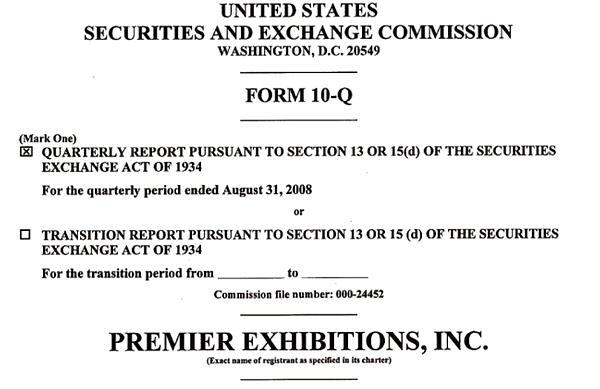

Form 10-Q is an abbreviated version of form 10-K and contains a company’s results by quarter, allowing comparison between a company’s previous financial quarter and its current financial quarter. It contains unaudited financial statements, and the reports are less detailed than Form 10-K.

The filing documents company management’s dissection and analysis of the company’s financial statements, as well as their notes about any abnormalities or points of interest in regard to the financial statements.

There are three classes of 10-Q filers, each subject to a different requirement regarding when its Form 10-Q must be filed.

Companies that are known as large accelerated filers — those with a float of $700 million or more — or accelerated filers — those with a $75 million to $699 million float — must file a Form 10-Q within a certain number of days from the end of their fiscal quarter. For large accelerated filers, it’s 40 days; accelerated filers are given an additional five days to file.

The third and final class of filer is the non-accelerated filer. They are companies with a public float that is less than $75 million. Such companies are, like accelerated filers, given 45 days from the end of their fiscal quarter to file their form.

While not directly related to Form 10-Q, the term “float” is important in the context of the filing because it determines how companies are classified, which determines when they must file a Form 10-Q.

Public float — otherwise known as free float — is the percentage or number of shares a company holds by public investors. It means that the shares aren’t currently being held by officers of the company, investors with a controlling interest in the company (which is often the same as company officers), governments, or promoters. Essentially, the float is comprised of all of a company’s freely traded common stock shares.

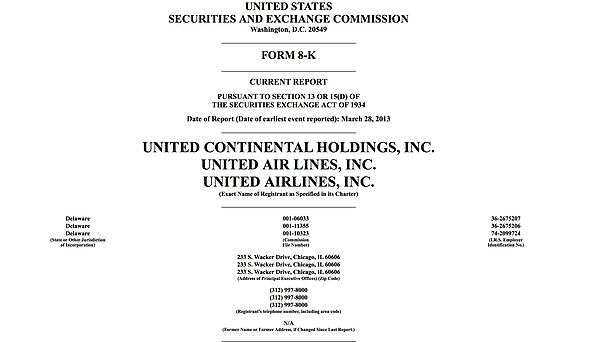

Unscheduled events that are important to the shareholders, investors, and the SEC are provided in Form 8-K. The listing also provides further details about these events, such as press releases and data tables. The form must be filled out and filed with the SEC within four days of the occurrence of a triggering event. Timely filing of Form 8-K makes it easier to transfer the information contained in the 8-K to quarterly reports that are submitted on Form 10-K and Form 10-Q.

Events that trigger the filing of Form 8-K may include the resignation of a director, bankruptcy, disposition of assets, appointment of new executives, or other significant developments. The significance of some events — for example, the departure of an executive with a lofty job title but who, in fact, isn’t all that critical to the company’s operations — may be debatable. Most companies err on the side of caution, and may sometimes file an 8-K form for events that wouldn’t necessarily require it.

In some situations, the need to make an 8-K filing is unquestionable. Possible filing triggers include:

To get a better understanding of how reading an 8-K form can be helpful to investors, consider the following:

In the event that a company files for bankruptcy, the Form 8-K should provide an outline for how the company intends to reorganize itself under Chapter 11 or Chapter 7 (bankruptcy or liquidation). This is important for investors because it must include pertinent information about the company’s stock and when it plans to come out from bankruptcy, if at all.

In the event that a company is being delisted from an exchange, a Form 8-K is required as a means of notification to investors. In many cases, this event occurs because the company’s stock has consistently traded below the exchange’s minimum required price for an extended period of time. The form identifies the specifics of why a company is in non-compliance with the exchange listing requirements. Most companies are given a grace period to return to being in a state of compliance with all exchange requirements before they are removed entirely.

Form S-1 is an initial registration form that companies must issue to investors the first time they go public. The form contains the company’s prospectus, which is a precursor to an initial public offering (IPO). It is crucial for investors to be able to look at a company’s prospectus before it goes public because there is little available information for companies in these initial stages. Form S-1 provides information on the planned use of funds, the number of shares to be issued, the company’s business model, competition, offering price methodology, and risk factors.

There are two parts to Form S-1. The first part is the prospectus, explained above. It provides all pertinent historical and financial information about the company, what shares are going to be made available, and other key information that an investor may need to know. The second part of the form is optional. It simply includes information about the sale of securities that are still unregistered by the filer and provides information about the company’s financial statement scheduling (e.g. when its fiscal year begins).

If a filer intentionally fails to put any of the required information on the S-1, or documents information is a way that is misleading, the company can be held liable, both criminally and financially.

The SEC form S-4 is submitted by companies going through an exchange offer and contains material information related to a merger or acquisition. The filing is needed by investors looking to make quick gains from mergers or acquisitions. Therefore, companies submitting SEC filing S-4 are required to disclose essential facts about their financial and operating activities.

While not exactly the same, Form 11-K is similar to Form 10-K. SEC filing 11-K is filed pursuant to Section 15d of the SEC Act of 1934 and is also referred to as the Annual Report of Employee Stock Purchase, Savings, and Similar plans. It is a special report that a security issuer should submit alongside other annual reports at the end of their fiscal financial year. It includes registration, proxy solicitations, audit requirements, and other disclosures important to the investing public.

Companies must file a Form 11-K, but employee stock purchase plans need to make similar public disclosures. This is important because the primary objective of the form is to give shareholders — and any individuals who are considering an investment in a company — all of the necessary financial and operating information about the company. This enables investors to obtain a well-rounded view of the company and, hopefully, determine the best way to structure their investments.

Anyone who purchases more than 5% of a company’s publicly traded securities must submit Schedule 13D to the SEC. The document is also called the Beneficial Ownership Report. The filing reveals the names of the large shareholders in a company and the purpose(s) of the purchase of shares. Based on this information, investors can make informed investing and voting decisions. The SEC also requires a prompt amendment for any material changes disclosed in the schedule. A filer must promptly update Schedule 13D to reflect any material change, such as a significant increase in the percentage of the company’s outstanding shares that they own.

Sections of the Schedule 13D filing

Schedule 13D includes seven sections: