Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

Form 10-Q is a quarterly report containing financial statements and management discussion and analysis over the most recent quarter

Form 10-Q is a required quarterly report for companies that are subject to United States Securities and Exchange Commission (SEC) regulations. Unlike the annual Form 10-K, Form 10-Q is a more frequent update on a company’s financial position and operations.

Companies will file Form 10-Q three times a year (after the first three fiscal quarters) but will file the 10-K at year-end instead of the fourth quarter 10-Q. A Form 10-Q, or simply 10-Q, is sometimes called a quarterly report.

Form 10-Q is similar to Form 10-K but less detailed. Additionally, the financial statements in a 10-Q are near the beginning of the filing, unlike the 10-K. The financial statements in a Form 10-Q are considered unaudited, unlike in the 10-K, where a full audit is performed. A quarterly report is sometimes known as an Interim Report since it covers a period shorter than a year.

The regular filing of Form 10-Q allows investors to monitor a company’s financial health and operational success at more frequent intervals than annually.

Form 10-Qs can range anywhere from 20 pages to over 100 pages, depending on the company and industry. 10-Qs are extremely useful, especially for equity research professionals, since they are filed several times a year, and analysts don’t need to wait a year between filings.

10-Qs contain financial statements and management’s discussion and analysis of recent financial results. 10-Qs consist of both quantitative and qualitative disclosures. Let’s take a look at the most important sections for a financial analyst.

One of the most important components of a Form 10-Q is timely financial statements. Form 10-Q financial statements are prepared using U.S. Generally Accepted Accounting Principles (GAAP). As opposed to the 10-K, financial statements are typically at the beginning of the Form 10-Q filing (in a 10-K, they are usually presented in the middle and sometimes even as an exhibit).

However, the 10-Q contains unaudited financial statements, while a 10-K presents a company’s audited financial statements. While this sounds like a big deal, it’s usually not a problem outside of a company committing fraud or other misconduct.

Additionally, the notes to the financial statements will be less detailed than what is found in the 10-K. In particular, disclosures around a company’s debt, income tax and deferred taxes, or stock options won’t be as thorough as in the 10-K.

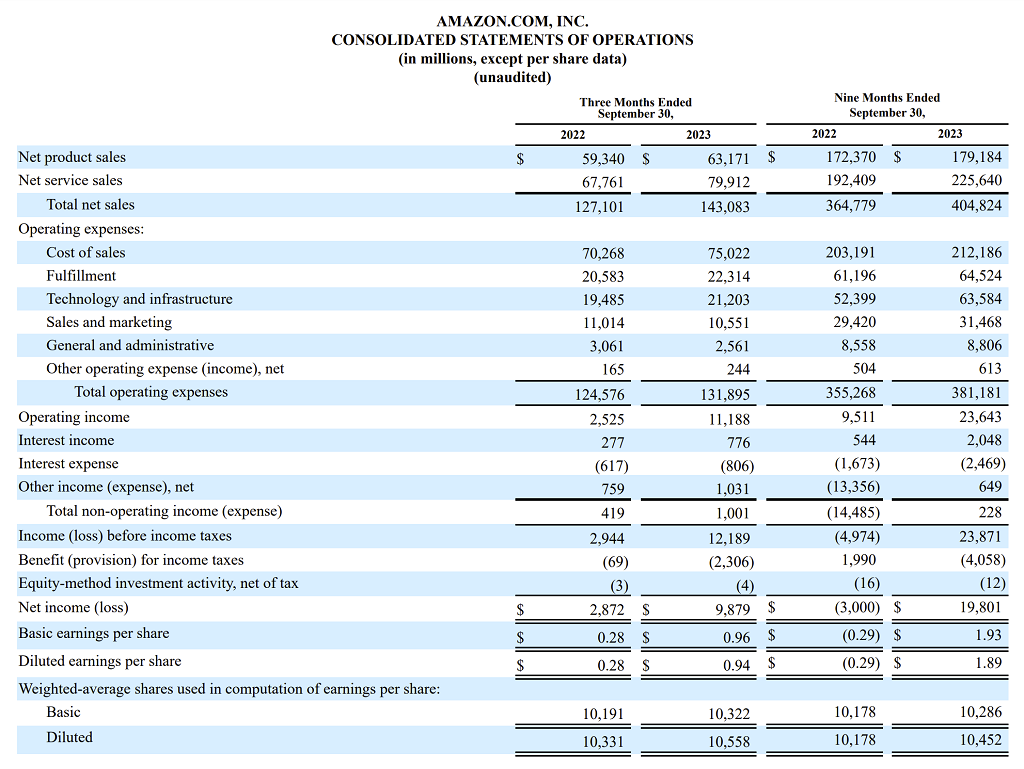

One thing to note, Form 10-Q will present financials from the most recent 3-month period, as well as the same comparable period in the previous year. Additionally, the 10-Q will provide year-to-date financial statements.

In the above screenshot, we can see that Amazon provides the company’s income statement for the Three Months Ended September 30 for both 2022 and 2023. To the right of that is the same information for the Nine Months Ended September 30. This is in contrast to the 10-K, which shows three years of income statement and cash flow statement data.

The Management Discussion and Analysis (MD&A) section of the 10-Q is widely used by analysts and other stakeholders and is a key part of Form 10-Q. The MD&A is management’s opportunity to discuss financial results, including revealing any significant events, trends, and risks that affect the financial data. Additionally, management might also provide financial guidance or present non-GAAP metrics.

In a 10-Q, the MD&A section will usually be after the notes to the financial statements, which differs from a 10-K, where the MD&A usually precedes the notes.

Any discussion of the company’s business will be quite abbreviated compared to a 10-K. In fact, more time is dedicated to discussing market risk exposures than the business description in a 10-Q.

Management will disclose information about the company’s exposure to various market risks like foreign currency exchange risks, commodity price risks, or interest rate risks.

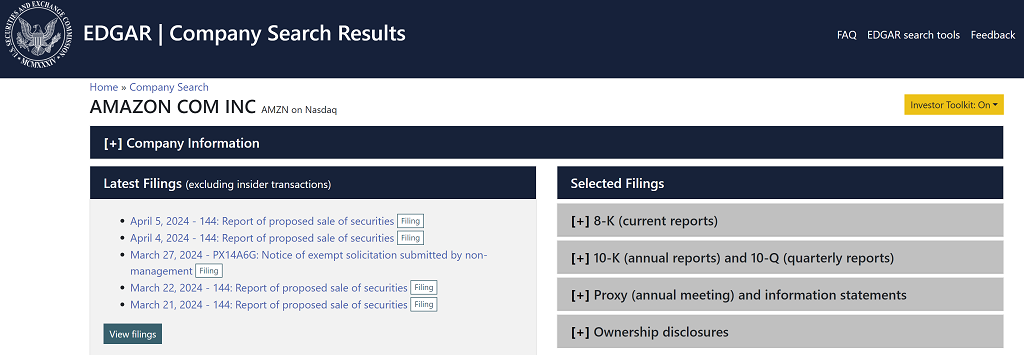

All 10-Qs are publicly available. The SEC provides the EDGAR database where users can easily search for 10-Qs (EDGAR is an abbreviation for Electronic Data Gathering, Analysis, and Retrieval System). Additionally, companies will post 10-Qs on their websites.

Below is a screenshot of Amazon’s filings as retrieved by EDGAR. On the right-hand side, you can see that 10-Ks and 10-Qs are highlighted under “Selected Filings.”

10-Q filing deadlines are set by the SEC and usually depend on the size of the company.

Deadlines are as follows:

If a company fails to submit a 10-Q (or 10-K) by the appropriate deadline, the company is required to file Form NT 10-Q (NT stands for “not timely”). NT filings must explain why the deadline wasn’t met. Once an NT form is filed, a company is still considered compliant as long as the delayed 10-Q is filed within five calendar days (15 calendar days for a 10-K).

Reasons companies don’t file on time include acquisitions, restructurings, or auditing delays, among other reasons.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

Thank you for reading CFI’s guide to Form 10-Q. To keep advancing your career, the additional CFI resources below will be useful: