Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

The investment made by both shareholders and debtholders in a company

Invested capital is the investment made by both shareholders and debtholders in a company. When a company needs capital to expand, it can obtain it either by selling stock shares or by issuing bonds. Shareholders are people who have purchased stock in a company and debtholders are those who have purchased bonds.

For a company, invested capital is a source of funding that enables them to take on new opportunities such as expansion. It has two functions within a company. First, it is used to purchase fixed assets such as land, buildings, or equipment. Secondly, it is used to cover day-to-day operating expenses, such as paying for inventory or paying employee salaries. A company may choose to invest capital funding over taking out a loan from a bank for several reasons.

For example, when a company issues stock shares, it has no obligation to issue dividends. This makes it a cheaper source of capital than paying interest on a bank loan. A company may also prefer to obtain funding through shares and bonds if it does not qualify for a large bank loan at a low interest rate.

For an investor, invested capital is evaluated using metrics such as the return on invested capital (ROIC) ratio. This ratio is used by an investor to determine the value of a company. A relatively higher ratio indicates a company is a value creator and is capable of utilizing invested funds to generate higher profits, as compared to other companies.

By dividing revenue by capital invested, the ratio shows the ability of a company to drive sales through its capital. A company that has a higher ratio compared to its peers means they are operating more efficiently.

The two ways to calculate the invested capital figure are through the operating approach and financing approach.

The formula for the operating approach is:

Where:

The formula for the financing approach is:

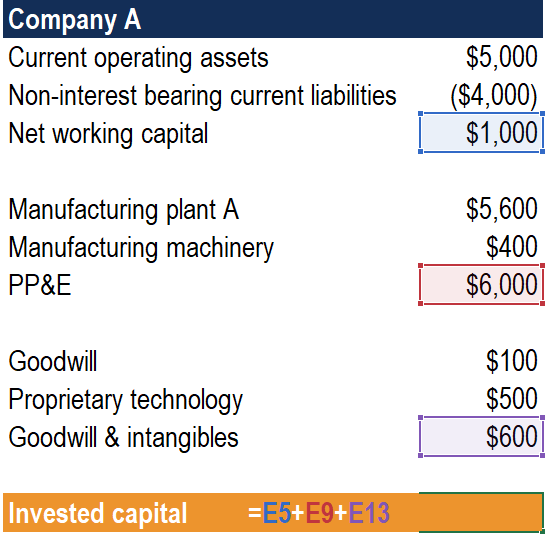

The following is the information for Company A:

For the operating approach, the numbers needed are (1) working capital, (2) PP&E, and (3) goodwill & intangibles. Firstly, to get the net working capital figure, subtract the non-interest-bearing liabilities from current operating assets.

Next, to get the PP&E, add the manufacturing plant A with manufacturing machinery. Lastly, to get the goodwill & intangibles, add the goodwill amount with proprietary technology. The last step toward getting the invested capital is to add the three categories together.

The following is the information for Company B:

For the financing approach, the main numbers needed are (1) total debt & leases, (2) total equity and equity equivalents, and (3) non-operating cash & investments. To calculate total debt & leases, add the short-term debt, long-term debt, and PV of lease obligations.

Next, to get the equity and equity equivalents, add the common stock and retained earnings together. Lastly, to get the non-operating cash and investments, add the cash from financing and cash from investing. The last step to get the capital invested is to add the three sums together.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

Thank you for reading CFI’s guide to Invested Capital. To keep advancing your career, the additional CFI resources below will be useful: