Get Specialized with our Financial Planning & Analysis (FP&A) Program

Support business leaders in their decision-making with best-in-class financial models to evaluate and forecast the financial performance of a company.

A budgeting process that allows a shared responsibility between the superiors and subordinates

Negotiated budgeting is a budgeting process that combines both top-down budgeting and bottom-up budgeting. The negotiated budgeting process does not impose the budget preparation process on a single level but rather allows shared responsibility between superiors and subordinates.

Unlike top-down budgeting, negotiated budgeting increases the involvement of lower-level managers, which makes it easier to set realistic targets. Employees also demonstrate a more personal interest in budget preparation since they feel that their contribution is recognized by management. The top managers agree to solicit suggestions from subordinates who are responsible for implementing the budget.

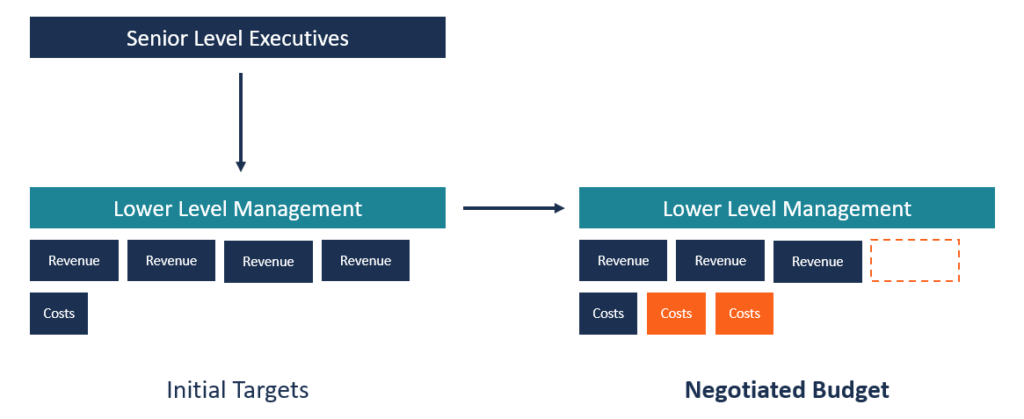

Companies follow the process below when preparing negotiated budgets:

The process starts with management preparing the targets for the next financial period. Usually, the top management uses historical performance data as a benchmark for setting the targets to be achieved.

Sometimes, the top-level executives may seek suggestions from lower-level managers on the targets for the next financial period. The prepared targets are then passed on to the lower-level managers for consideration.

The department-level managers receive the targets from the top-level managers and are required to prepare action plans based on the given targets. Unlike top-down budgeting, which limits the subordinates’ action plans to budget allocation, negotiated budgeting gives employees the flexibility to negotiate the projected revenue and costs.

The departmental projections can be higher or lower than the management targets. Such flexibility creates an incentive for employees to make suggestions.

After the creation of the action plans, both the superiors and subordinates meet to discuss the budget. The meeting acts as an open forum where subordinates can educate their superiors on the realities of the budget since they are the people tasked with implementing it.

The forum allows each party to present its views and negotiate the differing points until they come to a consensus. The goal is to reduce the difference in the cost estimates presented by each party until they agree on a budget that is acceptable to both sides.

Subordinates are often encouraged by their superior’s positive response to their suggestions, and they may surrender some of their demands to the superior’s advantage. However, the management retains the upper hand in the negotiations, and they can adjust the figures arrived at through the bottom-up budgeting process.

Once both parties have discussed and made suggestions on the budget, the changes should be incorporated into the budget. Usually, the departmental managers will be required to revise their budgets and projections to reflect what was agreed on.

Once the budget has been finalized, it is presented to the management for approval. The budget is then sent to the finance department for funding based on the projections agreed upon by management and subordinates.

Management’s role in the negotiated budgeting process is to provide direction for the company. The top managers are more experienced in planning than subordinates and are, therefore, best suited to set targets for the company. It takes less time since it does not require multi-level participation. If the employees were asked to prepare targets for the company, the budget preparation would take longer as the employees put forward their suggestions.

Another advantage of the top-down component is that the subordinates will better understand what the superiors expect in the next financial year. On the downside, the top executives possess limited knowledge of the specific departmental activities and may tend to underestimate the cost requirements.

The bottom-up element of a negotiated budget encourages commitment to the plan by involving the people who are responsible for budget implementation. A negotiated budget allows for shared responsibility between management and subordinates. It increases employee motivation, as compared to an imposed budget where employees are limited by the management’s targets.

When employees are allowed to prepare action plans on the revenue and cost projections for the next financial period, they will work together to take their plans to the next level until they reach the highest level for approval. Employees will take a personal interest in the plan. It will help boost their morale at work and motivate them to work hard to achieve the targets that they helped formulate.

CFI is a global provider of financial modeling courses and of the FMVA Certification. CFI’s mission is to help all professionals improve their technical skills. If you are a student or looking for a career change, the CFI website has many free resources to help you jumpstart your Career in Finance. If you are seeking to improve your technical skills, check out some of our most popular courses. Below are some additional resources for you to further explore:

CFI is a global provider of financial modeling courses and of the FMVA Certification. CFI’s mission is to help all professionals improve their technical skills. If you are a student or looking for a career change, the CFI website has many free resources to help you jumpstart your Career in Finance. If you are seeking to improve your technical skills, check out some of our most popular courses. Below are some additional resources for you to further explore:

Boost your confidence and master accounting skills effortlessly with CFI’s expert-led courses! Choose CFI for unparalleled industry expertise and hands-on learning that prepares you for real-world success.