Get Certified for

Commercial Banking (CBCA®)

Stand out and gain a competitive edge as a commercial banker, loan officer, or credit analyst with advanced knowledge, real-world analysis skills, and career confidence.

Financing for specific projects and assets

Project finance is the financial analysis of the complete life-cycle of a project. Typically, a cost-benefit analysis is used to determine if the economic benefits of a project are larger than the economic costs. The analysis is particularly important for long-term projects of growth CAPEX.

The first step of the analysis is to determine the financial structure, a mixture of debt and equity, that will be used to finance the project. Then, identify and value the economic benefits of the project and determine if the benefits outweigh the costs.

Now, let us break down each of the components of the project finance definition to get a detailed understanding of what it incorporates:

Project finance is generally used in oil extraction, power production, and infrastructure sectors. These are the most appropriate sectors for developing this structured financing technique, as they have low technological risk, a reasonably predictable market, and the possibility of selling to a single buyer or a few large buyers based on multi-year contracts (e.g. take-or-pay contracts).

Project finance is the structured financing of a specific economic entity – a Special Purpose Vehicle (SPV) – created by the sponsors using equity or debt. The lender considers the cash flow generated from this entity as the major source of loan reimbursement.

Hence, if the borrower has a debt default, the debt issuer has the right to seize the assets of the said SPV. However, they do not have the right to any further assets that are not part of the SPV, even if the liquidating assets of the SPV are not sufficient to cover the value owed due to default.

Cash flows generated by the SPV must be sufficient to cover payments for operating costs and to service the debt in terms of capital repayment and interest. Because the priority use of cash flow is to fund operating costs and to service the debt, only residual funds after the latter are covered can be used to pay dividends to sponsors undertaking the project.

To learn more, launch our free Corporate Finance Fundamentals course!

A sponsor (the entity requiring finance to fund projects) can choose to finance a new project using two alternatives:

Alternative 1 means that the sponsors use all the assets and cash flows from the existing firm to guarantee additional credit provided by lenders. If the project is not successful, then all the remaining assets and cash flows can serve as a source of repayment for all the creditors (old and new) of the combined entity (existing firm plus new project).

Alternative 2 means instead that the new project and the existing firm live two separate lives. If the project is not successful, project creditors have no (or very limited) claim on the sponsoring firm’s assets and cash flows. The existing shareholders then benefit from the separate incorporation of the new project into an SPV.

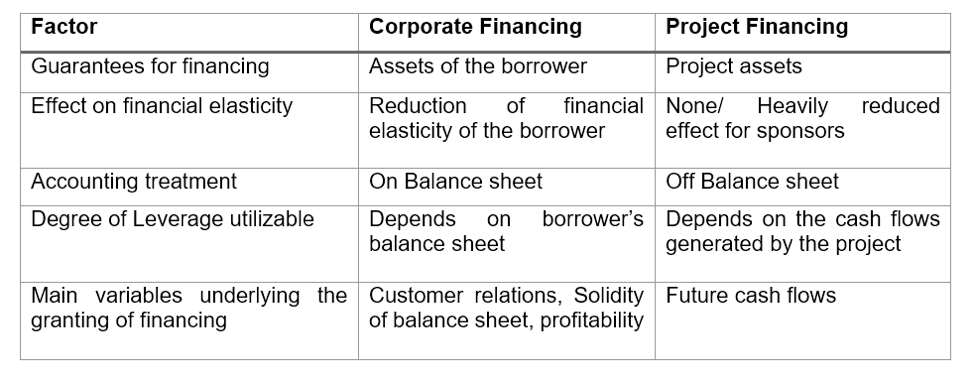

Now that we have a basic understanding of what project finance means, let us understand how it differs from corporate finance. The table below outlines key differences between the two financing types that need to be considered.

To learn more, launch our free Corporate Finance Fundamentals course!

By participating in a project finance venture, each project sponsor pursues a clear objective that varies depending on the type of sponsor. In brief, four types of sponsors are very often involved in such transactions:

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

Thank you for reading CFI’s guide to Project Finance. To learn more about how to value a business, or to prepare for a career in project finance, we’ve got all the resources you need! Here are some of our most popular resources related to project finance: