Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

"Managers follow a hierarchy when considering sources of financing"

The Pecking Order Theory, also known as the Pecking Order Model, relates to a company’s capital structure. Made popular by Stewart Myers and Nicolas Majluf in 1984, the theory states that managers follow a hierarchy when considering sources of financing.

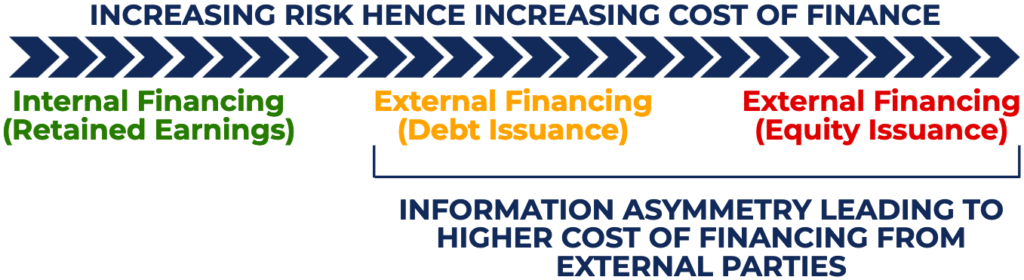

The Pecking Order Theory states that managers display the following preference of sources to fund investment opportunities: first, through the company’s retained earnings, followed by debt, and choosing equity financing as a last resort.

The following diagram illustrates the Pecking Order Theory:

The Pecking Order Theory arises from the concept of asymmetric information. Asymmetric information, also known as information failure, occurs when one party possesses more (better) information than another party, which causes an imbalance in transaction power.

Company managers typically possess more information regarding the company’s performance, prospects, risks, and future outlook than external users such as creditors (debt holders) and investors (shareholders). Therefore, to compensate for information asymmetry, external users demand a higher return to counter the risk that they are taking. In essence, due to information asymmetry, external sources of finance demand a higher rate of return to compensate for higher risk.

In the context of the Pecking Order Theory, retained earnings financing (internal financing) comes directly from the company and minimizes information asymmetry. As opposed to external financing, such as debt or equity financing, where the company must incur fees to obtain external financing, internal financing is the cheapest and most convenient source of financing.

When a company finances an investment opportunity through external financing (debt or equity), a higher return is demanded because creditors and investors possess less information regarding the company, as opposed to managers. In terms of external financing, managers prefer to use debt over equity – the cost of debt is lower compared to the cost of equity.

The issuance of debt often signals an undervalued stock and confidence that the board believes the investment is profitable. On the other hand, the issuance of equity sends a negative signal that the stock is overvalued and that the management is looking to generate financing by diluting shares in the company.

When thinking of the Pecking Order Theory, it is useful to consider the seniority of claims to assets. Debtholders require a lower return as opposed to stockholders because they are entitled to a higher claim to assets (in the event of a bankruptcy). Therefore, when considering sources of financing, the cheapest is through retained earnings, second through debt, and third through equity.

Suppose ABC Company is looking to raise $10 million for an investment project. The company’s stock price is currently trading at $53.77. Three options are available for ABC Company:

What would be the cost to shareholders for each of the three options?

Option 1: If management finances the project directly through retained earnings, the cost is $10 million.

Option 2: If management finances the project through debt issuance, the one-year debt would cost $10.8 million ($10 x 1.08 = $10.8). Discounting it back one year with the management’s fair rate would yield a cost of $10.09 million ($10.8 / 1.07 = $10.09 million).

Option 3: If management finances the project through equity issuance, to raise $10 million, the company would need to sell 200,000 shares ($53.77 x 0.93 = $50, $10,000,000 / $50 = 200,000 shares). The true value of the shares would be $10.75 million ($53.77 x 200,000 shares = $10.75 million). Therefore, the cost would be $10.75 million.

As illustrated, management should first finance the project through retained earnings, second through debt, and lastly through equity.

The pecking order theory relates to a company’s capital structure in that it helps explain why companies prefer to finance investment projects with internal financing first, debt second, and equity last. The pecking order theory arises from information asymmetry and explains that equity financing is the costliest and should be used as a last resort to obtain financing.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

Thank you for reading CFI’s guide to Pecking Order Theory. To keep advancing your career, the additional CFI resources below will be useful: