Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

Assets that can be realized into cash within a short period

Quick assets are those assets that can be converted into cash within a short period of time. The term is also used to refer to assets that are already in cash form. They are considered to be the most liquid assets that a company owns.

The main assets that fall under the quick assets category include cash, cash equivalents, accounts receivable, and marketable securities. Companies use quick assets to compute certain financial ratios that indicate their liquidity and financial health. In particular, they’re used to calculate the quick ratio.

Contrary to other kinds of assets, quick assets comprise economic resources that can be quickly converted to cash.

Another requirement for an item to be classified as a quick asset is that while converting it to cash, there should be minimal or no loss in value. In other words, a company shouldn’t incur a high cost when liquidating the asset.

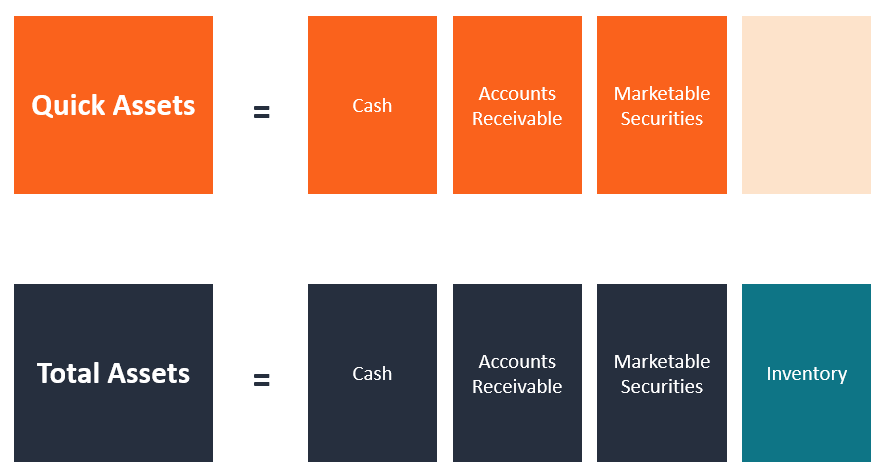

It is important to note that inventories don’t fall under the category of quick assets. This is because realizing cash from them takes time. The only way a business can convert inventory into cash quickly is if it offers steep discounts, which would result in a loss of value.

The majority of companies keep their quick assets in two primary forms: cash and short-term investments (marketable securities). By doing so, they hold enough capital to cover their operating, investing, and financing needs.

A company with a low cash balance in its quick assets can boost its liquidity by making use of its credit lines.

A major component of quick assets for most companies is their accounts receivable. If a business sells products and services to other large businesses, it’s likely to have a large number of accounts receivable. In contrast, a retail company that sells to individual clients will have a small number of accounts receivable on its balance sheet.

Quick assets make up part of current assets, which includes inventories. Thus:

As mentioned earlier, quick assets are used to calculate the quick ratio. This metric is used to determine a company’s capability to address its financial expenses in the short term by utilizing its most liquid assets. Given that it represents how well a company can utilize its near-cash assets to settle its current liabilities, it is also called the acid test. The formula for computing the quick ratio is:

Or,

When calculating the ratio, the first thing you need to do is look for each component in the current liabilities and current assets section of the balance sheet. Plug the corresponding values into the formula and compute.

Be sure to double-check the assets you’re using. The numerator should only consist of assets that are easy to convert into cash (typically within 90 days or less) without jeopardizing their value.

On the same note, the accounts receivable should only consist of debts that can be collected within a 90-day period.

Consider the balance sheet of Greenshaw Furnitures showing the following data:

The value of the company’s quick assets is $3 million ($200,000 + $300,000 + $2,500,000).

Let’s say Ashley’s Clothing Store plans to apply for a loan to renovate its storefront. The lending institution asks the owner for a balance sheet. Ashley’s Clothing Store’s financial statement shows the following:

The clothing store’s quick ratio is 1.21 ($10,000 + $5,000 + $2,000) / $14,000.

A high quick ratio is an indication that a company is utilizing its short-term assets effectively to meet its financial needs.

If a company reports an acid test ratio of 1, this indicates that its quick assets equal its existing liabilities. A ratio higher than 1 indicates that the company’s quick assets are more than sufficient to cover liabilities. The company is fully capable of paying current liabilities without tapping into its long-term assets and will still have cash or cash equivalents left over.

Long-term assets are those used to generate revenue. As such, selling those resources would hurt the company’s ability to generate revenue and also indicate that its current activities aren’t creating adequate profits to cover its current liabilities.

As seen in the example above, Ashley’s Clothing Store’s quick ratio is greater than 1. It means that it has enough quick assets to cover all its current liabilities and still has more left.

Companies should aim for a high quick ratio because it can help attract investors. It also increases the company’s chance of getting loans, as it shows creditors that it is able to handle its debt obligations.

Thank you for reading CFI’s guide to Quick Assets. To keep advancing your career, the additional CFI resources below will be useful: