Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

The minimum capital that banks should keep as a reserve to reduce the risk of insolvency

Risk-weighted assets is a banking term that refers to an asset classification system that is used to determine the minimum capital that banks should keep as a reserve to reduce the risk of insolvency. Banks face the risk of loan borrowers defaulting or investments flatlining, and maintaining a minimum amount of capital helps to mitigate the risks.

The different classes of assets held by banks carry different risk weights, and adjusting the assets by their level of risk allows banks to discount lower-risk assets. For example, assets such as debentures carry a higher risk weight than government bonds, which are considered low-risk and assigned a 0% risk weighting.

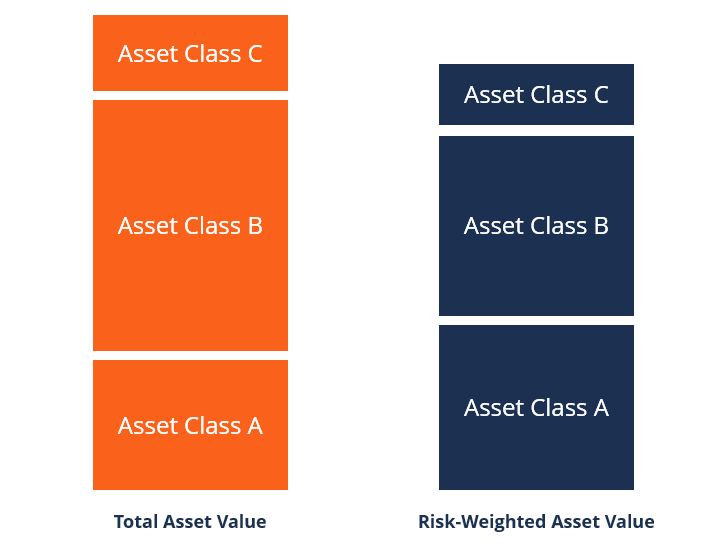

When calculating the risk-weighted assets of a bank, the assets are first categorized into different classes based on the level of risk and the potential of incurring a loss. The banks’ loan portfolio, along with other assets such as cash and investments, is measured to determine the bank’s overall level of risk. This method is preferred by the Basel Committee because it includes off-balance sheet risks. It also makes it easy to compare banks from different countries around the world.

Riskier assets, such as unsecured loans, carry a higher risk of default and are, therefore, assigned a higher risk weight than assets such as cash and Treasury bills. The higher the amount of risk an asset possesses, the higher the capital adequacy ratio and the capital requirements. On the other hand, Treasury bills are secured by the ability of the national government to generate revenues and are subject to much lower capital requirements than unsecured loans.

The Basel Committee on Banking Supervision (BCBS) is the global banking regulator that sets the rules for risk weighting. The first step in international banking regulation started with the publication of the Basel I framework, which set the capital requirements for banks. It was followed by the Second Basel Accord of 2004 that amended the banking regulations on the amount of capital banks should maintain against their risk exposure. Basel II recommended that banks should hold adequate capital that is at least 8% of the risk-weighted assets.

The financial crisis of 2007/08 exposed the inefficiencies that existed in the banking industry that led to the collapse of large US banks. The main cause of the crisis was investments in sub-prime home mortgage loans that carried a higher risk of default than bank managers expected – or at least acknowledged.

Following the global financial crisis, the BCBS introduced the Basel III framework, which aimed to strengthen the capital requirements of banks. It also established new requirements for funding stability and liquid assets. Basel III requires banks to group their assets by risk category so that the minimum capital requirements are matched with the risk level of each asset. The framework is scheduled to take full effect on January 1, 2022.

When determining the risk attached to a specific asset held by a bank, regulators consider several factors. For example, when the asset being assessed is a commercial loan, the regulator will determine the loan repayment consistency of the borrower and the collateral used as security for the loan.

On the other hand, when assessing a loan used to finance the construction of coastal condominiums, the assessor will consider the potential revenues from the sale (or rental) of the condos and if their value is sufficient to repay the principal and interest payments. This is assuming that the condos serve as collateral for the loan.

If the asset being considered is a Treasury bill, the assessment will be different from a commercial loan, since a Treasury bill is backed by the government’s ability to continually generate revenues. The federal government has higher financial credibility, which translates to lower risk to the bank. Regulators require banks holding commercial loans on their balance sheet to maintain a higher amount of capital, whereas banks with Treasury bills and other low-risk investments are required to maintain far less capital.

Capital requirements refer to the minimum capital that banks are required to hold depending on the level of risk of the assets they hold. The minimum capital requirements set by regulatory agencies such as the Federal Reserve and the Bank for International Settlements (BIS) are designed to ensure that banks hold enough capital, proportionate to the level of risk of the assets they hold. The capital acts a cushion of cash if the bank incurs operational losses in the course of the operations.

CFI offers the Financial Modeling & Valuation Analyst (FMVA)™ certification program for those looking to take their careers to the next level. To keep learning and advancing your career, the following CFI resources will be helpful: