Homeowners Insurance

A type of property insurance that covers damages to an individual’s home and personal belongings

What is Homeowners Insurance?

Homeowners insurance refers to a type of property insurance that covers damages to property, personal belongings, and personal liability suffered when an insured peril occurs. The policy provides financial relief to the homeowner when the covered event causes damage to the property or injury to another person.

For example, when an unexpected event, such as a fire or burglary occurs, and the property or attached structures are damaged, homeowners insurance will compensate the homeowner for the losses and damages suffered.

The policy also provides coverage for accidents and bodily injuries suffered by visiting guests. A homeowners insurance policy includes a liability limit that determines the level of coverage of a policyholder should an unexpected event occur. Although homeowners insurance is not mandatory, homeowners are required to take out a policy when taking a mortgage loan.

Summary

- Homeowners insurance refers to a type of property insurance that covers damages to an individual’s home and personal belongings.

- A homeowners insurance policy also includes liability protection against injuries or accidents that occur in the home.

- Some of the perils covered in a homeowners insurance policy include fire, theft, vandalism, water, lightning, and civil unrest.

Types of Coverage in Homeowners Insurance

A standard homeowners insurance policy provides the following types of coverage:

Structure

Homeowners insurance covers the entire structure of a home and any connected structures, such as a garage and a cellar. If the structure is damaged by a covered loss, such as lightning, fire, hurricane, or other insured peril, the policy will cover the cost to rebuild or repair the structure.

Most homeowners insurance policies also provide coverage for other structures that are on the property but are detached from the home, such as a gazebo, detached garage, deck, etc., from certain risks.

Personal Belongings

The policy also protects personal belongings in a home, such as electronic devices and furniture. If an insured event, such as theft, fire, or flooding occurs, and the personal belongings are damaged, the policy will pay the cost to repair or replace the belongings.

Personal belongings coverage may include jewelry, silverware, and other luxury items, but there is a dollar limit if such items are destroyed or stolen. Still, homeowners can purchase extended coverage for the items whose value exceeds coverage limits.

Liability Protection

The liability protection covers damages and losses resulting from injuries caused to guests on the property or other expenses that come about due to the homeowner’s negligence. The coverage also includes damages caused by pets on the property. Liability coverage also pays the costs of defending the policyholder in court in case there is a legal dispute.

Liability protection may also cover the cost of an individual’s medical bills, physical disability from an accident at the property, as well as the loss of income. An excess liability policy may expand the coverage to include claims for libel and slander against the policyholder.

Additional Living Expenses

The additional living expenses coverage pays the temporary living expenses of the policyholder if the home is inhabitable due to the damage caused by an insured peril, such as a fire, storm, or other covered disasters. Some of the expenses covered include hotel booking costs, restaurant meals, etc.

What is Covered in Homeowners Insurance?

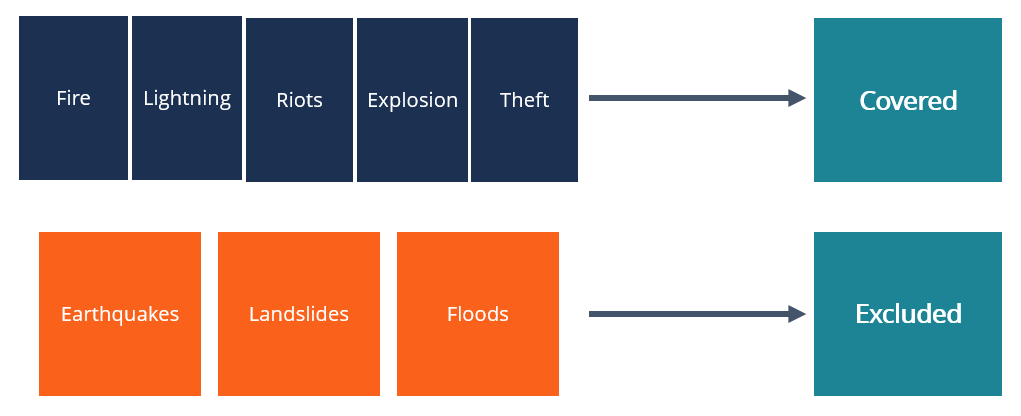

Generally, the perils covered in a homeowners insurance policy are indicated in the insurance policy declaration page of the policy signed by the policyholder and the insurer. A basic homeowners insurance policy will cover losses and damages caused by fire, lightning, civil riots, explosion, theft, smoke, and vandalism. The relevant perils are covered in detail below:

Fire

Fire is described in insurance terms as anything that sparks, glows, or produces flames. Homeowners insurance covers damages or losses to the structure or personal belongings caused directly by fire.

Lightning

Damages caused by lightning or fire caused by a lightning strike are also covered by a homeowners insurance policy. The policy also covers damages to home appliances and electrical systems that are caused directly by the lightning strike. It does not cover damages to electrical appliances caused by the power company.

Riots

Where a property suffers damages or losses due to a civil commission, a homeowners insurance policy will compensate the policyholder for the losses suffered. The riot must’ve involved at least three or more people.

Explosion

A homeowners insurance policy may vary when defining what constitutes an explosion. A basic policy may cover explosions that result from within the covered structure or attached structures. In some cases, the policy may cover explosions from outside the structure that cause damage to the insured property.

Theft

Where a homeowner suffers losses due to burglary, the insurance policy will pay the cost of repairing or replacing the stolen items. The coverage may be limited up to a certain dollar value unless the homeowner previously purchased an extended coverage that fully covers items such as jewelry, watches, and furs.

What Is Not Covered in Homeowners Insurance?

Homeowners insurance policy coverage is limited to selected perils and may exclude certain perils to reduce its risk exposure. For example, damages caused intentionally by oneself are excluded.

Other perils excluded from homeowners insurance include events caused by acts of war and acts of God, such as earthquakes, floods, landslides, and sinkholes. A homeowner living in an area prone to the excluded perils can get special coverage that protects them from the specific perils.

Additional Resources

CFI offers the Commercial Banking & Credit Analyst (CBCA)™ certification program for those looking to take their careers to the next level. To keep learning and developing your knowledge base, please explore the additional relevant resources below: