Get In-Demand Finance Certifications

A reserve of money that can only be used for particular projects or purposes

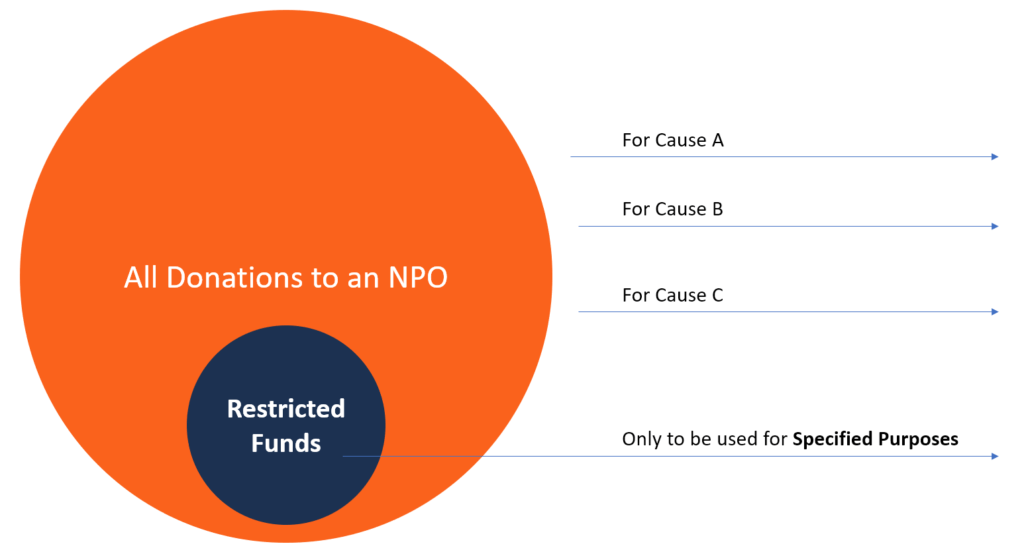

In the non-profit industry, restricted funds refer to a reserve of money that can only be used for specific projects or purposes. The funds can be restricted because the donor wants the money to go to a specific program or the donor wants the money to be utilized after a specific time or event, such as an anniversary. Restricted funds give donors assurance that their money is being used in the manner they desire.

When a donor gives money to a non-profit organization, he or she may specify whether their donation is restricted or can be used in any manner the organization sees fit. If the donor temporarily restricts how the funds can be utilized, the organization must use the funds for the designated purpose.

If the funds are permanently restricted, the donation acts as the principal amount, and only the interest earned can be spent on charitable activities. There may also be restrictions on how the interest amount can be spent. If the non-profit fails to comply with the directions of the donor, the latter may take legal action against the organization or demand a full refund of the donation.

The decision to make a donation – restricted or unrestricted – lies with the donor. The donor makes this designation through a letter accompanying the gift or through an explicit agreement with the non-profit organization. Non-profits can avoid confusion by offering a choice of designation when soliciting donations by direct mail or email. It can be achieved by adding a clause to that effect either on the donation form or in the gift acknowledgment.

For example, the American Red Cross offers donors the choice of donating to Disaster Relief, Local Red Cross, or where it is needed most. The designation reduces confusion where the donors do not explicitly state their preferred designation of the funds.

However, most non-profit organizations request unrestricted funds when soliciting donations. They include a statement in the email or direct mail solicitation that the donor is giving an unrestricted gift to the organization. This gives them flexibility in allocating funds to specific programs where the funds are needed most. An exemption to this is when the non-profit is soliciting funds toward a specific goal such as a scholarship fund or building fund.

The designation that specifies the type of donation is contained in a document called the “gift instrument.” A gift instrument is the award document that is written by a foundation or an individual donor outlining how the funds will be used. Restricted funds are grouped into the following two categories:

A temporarily restricted fund is usually time-bound and can be used for a specific purpose within a specified period. When the purpose for which it was intended is completed, or the time allowed has ended, the money becomes unrestricted or stopped. For example, a donation toward a scholarship fund is terminated when the recipient graduates from the university program. Similarly, if donors were contributing toward the construction of a building, the fund is terminated when the building project has been completed.

A permanently restricted fund invests the gift and then uses the interest earned to fund specific purposes designated by the donor. The funds are deposited into an endowment fund that supports specific projects or the non-profit organization in general. The non-profit is only allowed to use the interest and investment returns to support specific activities of the organization. Permanently restricted funds do not expire.

The Financial Accounting Standards Board (FASB) issued guidelines relating to the recording of revenues earned by non-profits in 1996. The guidelines are contained in FASB 116, which requires that all contributions received from donors must be grouped as either unrestricted, temporarily restricted, or permanently restricted.

The classifications must also be recorded separately in the organization’s financial statements. This makes it easy to track each donation and how it has been utilized. When the purpose or time restrictions are met, a journal entry is made and any remaining funds in these accounts can be transferred to an unrestricted funds account.

A non-profit should maintain separate unrestricted, temporarily restricted, and permanently restricted funds during the budgeting process. If the funds are managed as one fund, the non-profit may make decisions based on larger numbers than the donors allocated.

For example, if the funds total $500,000, and the restricted funds amount to $300,000, the non-profit cannot utilize the latter for unrestricted purposes.

A non-profit organization can implement an internal control system that tracks how donations are spent and alerts management once the fund time and purpose restrictions have been met. The funds are then transferred to unrestricted fund accounts since the donor’s wishes have been fulfilled.

The organization should also train its staff on how to identify and record expenditures that should be allocated to restricted funds. Correctly allocating funds to the right purpose keeps the donors happy and helps the organization avoid legal issues over the misappropriation of funds.

When making solicitations for donations, non-profit organizations need to provide donors with the option of designating their contributions as restricted or unrestricted funds. If the donors specify that their gifts are restricted, then the organization is under a moral obligation to honor the wishes of the donor.

There is also a legal obligation since the law requires that non-profits should utilize the donations for the purpose which the donors intended. If for any reason the non-profit fails to honor the donor’s wishes and utilizes the funds for other unintended purposes, the donor can demand a refund of his or her donation. The donor is also at liberty to sue the organization for misappropriation of funds or make a report against the charity at the Attorney General’s office in the state where the non-profit is located.

Thank you for reading CFI’s explanation of Restricted Funds. To keep learning and advancing your career, the additional CFI resources below will be useful:

Below is a break down of subject weightings in the FMVA® financial analyst program. As you can see there is a heavy focus on financial modeling, finance, Excel, business valuation, budgeting/forecasting, PowerPoint presentations, accounting and business strategy.

A well rounded financial analyst possesses all of the above skills!

CFI is the global institution behind the financial modeling and valuation analyst FMVA® Designation. CFI is on a mission to enable anyone to be a great financial analyst and have a great career path. In order to help you advance your career, CFI has compiled many resources to assist you along the path.

In order to become a great financial analyst, here are some more questions and answers for you to discover:

Learn accounting fundamentals and how to read financial statements with CFI’s online accounting classes.

These courses will give you the confidence to perform world-class financial analyst work. Start now!

Boost your confidence and master accounting skills effortlessly with CFI’s expert-led courses! Choose CFI for unparalleled industry expertise and hands-on learning that prepares you for real-world success.