Get Certified for

Capital Markets (CMSA®)

From equities and fixed income to derivatives, the CMSA certification bridges the gap from where you are now to where you want to be — a world-class capital markets analyst.

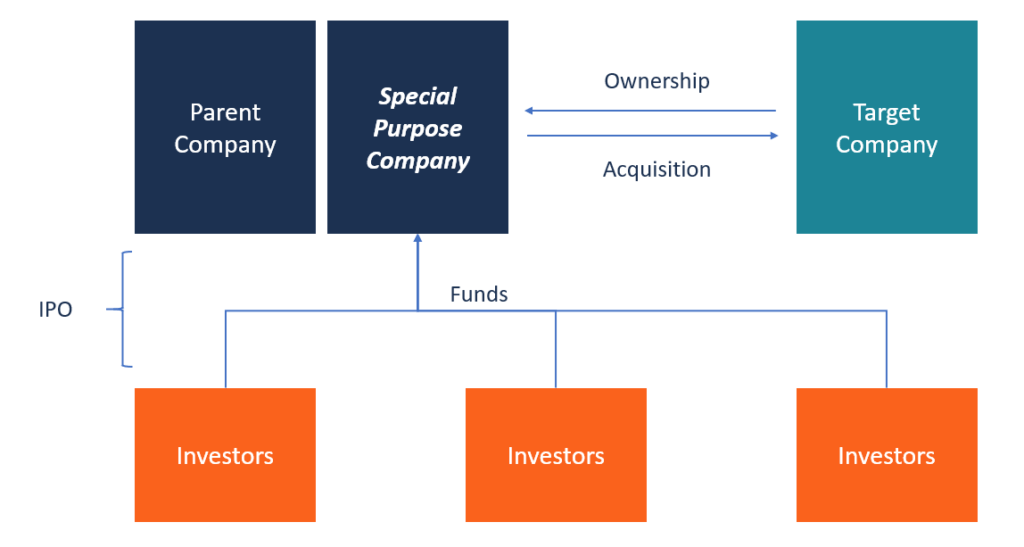

An entity formed for the sole purpose of raising investment capital through an IPO

A special purpose acquisition company (SPAC) is a corporation formed for the sole purpose of raising investment capital through an initial public offering (IPO). Such a business structure allows investors to contribute money towards a fund, which is then used to acquire one or more unspecified businesses to be identified after the IPO. Therefore, this sort of shell firm structure is often called a “blank-check company” in popular media.

When the SPAC raises the required funds through an IPO, the money is held in a trust until a predetermined period elapses or the desired acquisition is made. Therefore, a SPAC doesn’t conduct any business, does not sell anything and typically only holds the money raised in its own IPO.

In the event that the planned acquisition is not made or legal formalities are still pending, the SPAC is required to return the funds to the investors.

A special purpose acquisition company is formed by experienced business executives who are confident that their reputation and experience will help them identify a profitable company to acquire. Since the SPAC is only a shell company, the founders’ reputation may become the selling point when sourcing funds from investors. The founders often hold an interest in a specific industry when starting a special purpose acquisition company.

A SPAC may also be founded by a team of well-connected private investors like billionaire Bill Ackman, institutional investors, private equity or hedge funds, or even high-profile CEOs like Richard Branson and even Donald Trump. These financiers are called Sponsors.

The founders and sponsors provide the starting capital for the company and they stand to benefit from a sizeable stake in the acquired company.

When issuing the IPO, the management team of the SPAC contracts an investment bank to handle the IPO. The investment bank and the management team of the company agree on a fee to be charged for the service, usually about 10% of the IPO proceeds. The securities sold during an IPO are offered at a unit price, which represents one or more shares of common stock.

The prospectus of the SPAC mainly focuses on the sponsors, and less on company history and revenues, since the SPAC lacks performance history or revenue reports. All proceeds from the IPO are held in a trust account until a private company is identified as an acquisition target.

After the SPAC has raised the required capital through an IPO, the management team has 18 to 24 months to identify a target and complete the acquisition. The period may vary depending on the company and industry. The fair market value of the target company must be 80% or more of the SPAC’s trust assets.

Compared to an IPO, the SPAC is much less risky for the target company. In a SPAC acquisition, the target company only needs to sign a deal with the SPAC for a fixed amount of money at a negotiated price. Whereas if the company decides to go the IPO route, the target company is uncertain about the size, price, or even potential demand.

If the SPAC is successful in acquiring a target company, the founders will profit from their stake in the new company, usually 20% of the common stock, while the investors receive an equity position according to their capital contribution.

In the event that the predetermined period lapses before an acquisition is completed, the SPAC is dissolved, and the IPO proceeds held in the trust account are returned to the investors. When running the SPAC, the management team is not allowed to collect salaries until the deal is completed. The founders, in that case, would be out-of-pocket any expenses incurred to set up the SPAC in the first place

A SPAC floats an IPO to raise the required capital to complete an acquisition of a private company. The capital is sourced from retail and institutional investors, and 100% of the money raised in the IPO is held in a trust account. In return for the capital, investors get to own units, with each unit comprising a share of common stock and a warrant to purchase more stock at a later date.

The purchase price per unit of the securities is usually $10.00. After the IPO, the units become separable into shares of common stock and warrants, which can be traded in the public market. The purpose of the warrant is to provide investors with additional compensation for investing in the SPAC.

The founders/sponsors of the SPAC will purchase founder shares at the onset of the SPAC registration, and pay nominal consideration for the number of shares that results in a 20% ownership stake in the outstanding shares after the completion of the IPO.

The shares are intended to compensate the management team, who are not allowed to receive any salary or commission from the company until an acquisition transaction is completed.

The units sold to the public comprise a fraction of a warrant, which allows the investors to purchase a whole share of common stock. Depending on the bank issuing the IPO and the size of the SPAC, one warrant may be excisable for a fraction of a share (either half, one-third or two-thirds) or a full share of stock.

For example, if a price per unit in the IPO is $10, the warrant may be exercisable at $11.50 per share. The warrants become exercisable either 30 days after the De-SPAC transaction or twelve months after the SPAC IPO.

The public warrants are cash-settled, meaning that the investor must pay the full cost of the warrant in cash to receive a full share of stock. Founder warrants, on the other hand, may be net settled, meaning that they are not required to deliver cash to receive a full share of stock. Instead, they are issued shares of stock with a fair market value equal to the difference between the stock trading price and the warrant strike price.

Thank you for reading CFI’s guide to Special Purpose Acquisition Company (SPAC). To keep learning and advancing your career, the following CFI resources will be helpful: