Get Certified for

Capital Markets (CMSA®)

From equities and fixed income to derivatives, the CMSA certification bridges the gap from where you are now to where you want to be — a world-class capital markets analyst.

A financial arrangement between two counterparties to buy or sell equity at a specified date, amount, and price

Equity futures definition: An equity futures contract is a financial arrangement between two counterparties to buy or sell equity at a specified date, amount, and price.

Finance professionals use these instruments to capitalize on stock price movements or protect portfolios against market volatility — all without direct share ownership. Unlike equities futures, which involve direct stock ownership, equity futures track the price of an individual stock or index as a derivative.

The power of equity futures leverage stands out as a crucial advantage. By investing just a portion of the total contract value upfront, you can maximize your market exposure. However, this amplified position cuts both ways, potentially multiplying your returns or losses.

When comparing equity futures vs. equity options, the main difference is obligation. Futures contracts must be fulfilled at expiration, while options give you the flexibility to abandon your position. Additionally, daily settlement means your positions reflect real-time market movements through immediate profit and loss adjustments.

At maturity, contracts are either physically settled (shares exchanged) or cash-settled based on price differences. Though equity futures provide sophisticated trading opportunities, success demands strategic planning and thorough risk assessment.

In a futures contract, two parties have opposing views on an equity’s future value. The bullish party expects the price to rise and seeks to buy, while the bearish party expects it to fall and seeks to sell. They enter into a futures contract to lock in the price for a future exchange.

An equity futures contract must contain the following components that are agreed upon between the counterparties:

Futures contracts are used for two purposes: speculation and hedging. Speculators predict the future value of the equity and use futures to lock in the price. For example, if an investor is bullish on a stock, they may enter a futures contract to buy the stock in the future. If the speculation was right, the investor would use the contract to buy the stock for less than its market value.

The second purpose of hedging is to mitigate the potential losses of investment. For example, an investor currently invests in an index but worries that it may drop in value in the future. They can enter a futures contract to sell the index to hedge against a price drop. If the index ends up losing value, the investor would’ve already locked in a delivery price and can sell the stock for more than its market value.

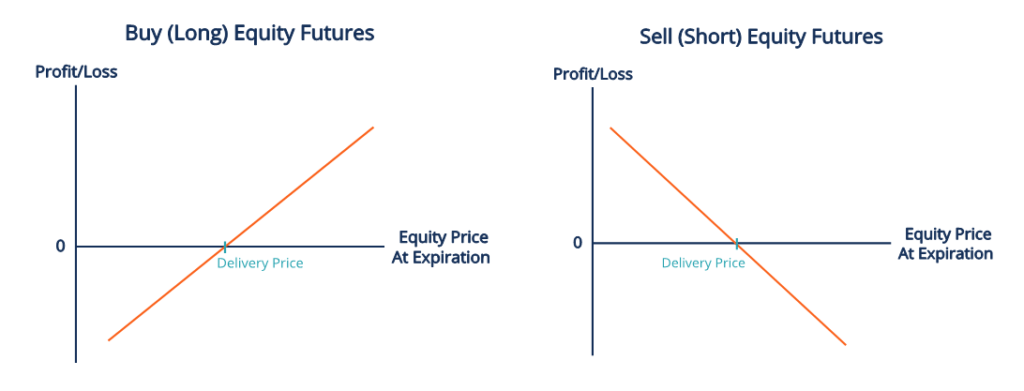

Futures are a zero-sum game, so there is bound to be a winner and a loser. The above graph illustrates the idea.

For the party buying the equity, they make a profit if the equity’s market price at expiration is greater than the delivery price – meaning that they can buy the equity for cheaper than the market value. However, if the equity’s market price falls below the delivery price, they end up having to pay more than the market price for the equity.

This is the exact opposite for the seller. The profits realized from one party are the losses from the other party (minus any fees taken from intermediaries).

In equity futures trading, leverage and margin serve distinct purposes. Leverage enables control of large positions with minimal upfront investment, magnifying potential gains and losses. Margin represents the required deposit to open and maintain positions, protecting against significant losses.

The futures market uses a mark-to-market settlement to adjust account balances daily based on a price change. Traders monitor equity futures quotes to track contract prices, assess market sentiment, and position their trades. Understanding these components is essential for effective risk management and smart trading decisions.

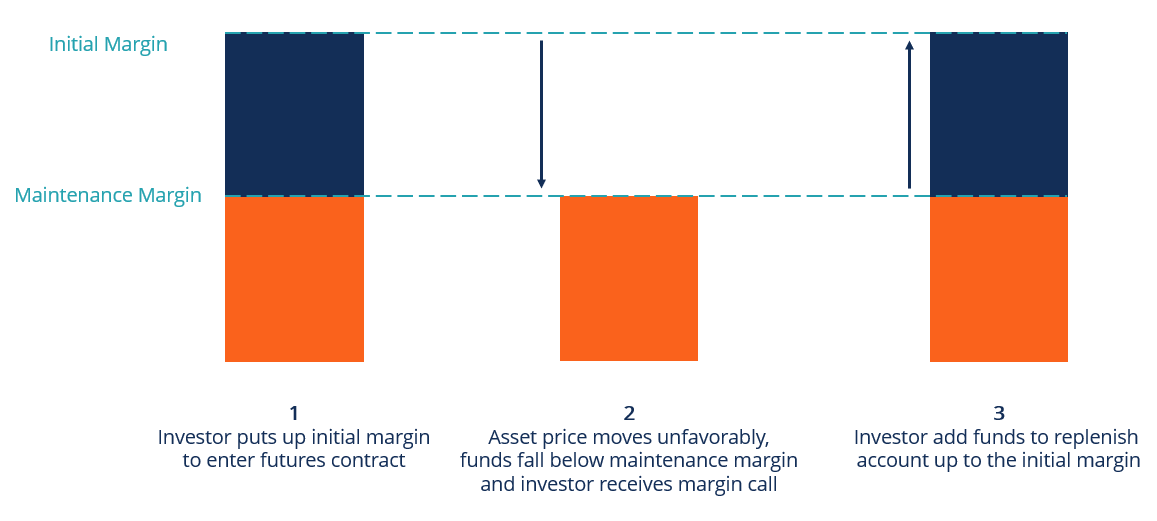

Margin acts as a security deposit required from each party throughout the contract period. Instead of exchanging the full contract value upfront, parties post margin to ensure contract completion.

Margins adjust daily through mark-to-market (MTM) settlement based on underlying equity prices. As market values shift, both contract delivery prices and margin amounts update to maintain original terms.

Example: When a contract’s delivery price of $100 rises to $110, the buyer receives a $10 margin credit while the seller’s margin decreases by $10 — reflecting the new market price.

There are two margins in a futures contract:

The initial margin represents the deposit each party must provide to enter the contract, typically calculated as a percentage of the contract’s value.

The maintenance margin sets the minimum balance maintained throughout the contract. If funds drop below this level, the party receives a margin call requiring additional funds to restore the initial margin.

Leverage in equity futures trading allows you to control a large position with a relatively small upfront investment. Instead of paying the full value of a futures contract, you only need to deposit a fraction of the total cost, known as the margin. This borrowed capital increases both potential gains and losses, making leverage a powerful but risky tool.

Market movements have magnified effects with leverage. Even small price changes can create substantial profits or losses. Maintaining adequate margin is crucial — falling below minimum requirements triggers margin calls demanding additional funds.

Two parties enter an equity futures contract to exchange 1,000 shares in six months. They agree on a delivery price of $500,000, an initial margin of 10%, and a maintenance margin of 5% of the notional value.

At the start of the agreement, both parties put up (500,000 x 10%) = $50,000 as the initial margin. Now, suppose that the shares fall $30,000 in value. The new delivery price is adjusted to (500,000 – 30,000) = $470,000.

Because the buyer gets to buy the shares for a lower delivery price in the future, the difference is accounted for in the margin today. $30,000 is taken from the buyer’s margin: (50,000 – 30,000) = 20,000.

The buyer’s margin account now falls below the maintenance margin of 5% (500,000 x 5% = $25,000). Therefore, the buyer receives a margin call to replenish their account up to the initial margin. The $30,000 taken from the buyer’s margin is placed into the seller’s margin.

While both instruments enable stock price speculation and risk management, their mechanics differ. Options grant the right to buy or sell at a set price before expiration, while trading futures binds parties to complete the transaction at a predetermined price.

Both instruments serve distinct roles in trading and portfolio management, with choices depending on risk tolerance and market strategy.

Learn more about Equity Derivatives in CFI’s guide.

When you trade futures, you’ll find both compelling opportunities and significant risks. Your success depends on mastering both aspects to build effective strategies.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

CFI is the official provider of the Capital Markets & Securities Analyst (CMSA)® certification program, designed to transform anyone into a world-class financial analyst.

To keep learning and developing your knowledge of financial analysis, we highly recommend the additional resources below: