Get Certified for

Capital Markets (CMSA®)

From equities and fixed income to derivatives, the CMSA certification bridges the gap from where you are now to where you want to be — a world-class capital markets analyst.

A technique used to estimate the market price of fixed income securities that are not actively traded

Matrix pricing is an estimation technique used to estimate the market price of securities that are not actively traded. Matrix pricing is primarily used in fixed income, to estimate the price of bonds that do not have an active market. The price of the bond is estimated by comparing it to corporate bonds with an active market, and that have similar maturities, coupon rates, and credit rating. This relative estimation process can be very helpful for debt valuation of private companies, which typically don’t report as much information as public companies.

Another use of matrix pricing is for bond underwriting, which can be used to estimate what the market’s required rate of return on the bond will be.

Yield to Maturity (YTM) is the total expected return from a bond if the bond is held until maturity, i.e., until the end of its lifetime, and all coupon are reinvested at the same rate.

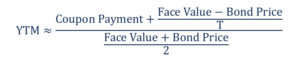

If we assume that coupon payments don’t change over time, then:

The formula shown above describes a polynomial in YTM. An approximate formula for the Yield to Maturity is the following:

Learn more about YTM on CFI’s Fixed Income Fundamentals Course!

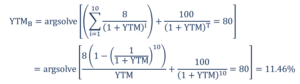

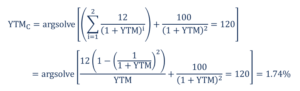

Bond A is a 6-year 10% annual coupon payment bond that is not actively traded on the market. Bond B is a 10-year 8% annual coupon payment bond that is actively traded on the market and with a market price of $80. Bond C is a 2-year 12% annual coupon payment bond that is actively traded on the market and with a market price of $120. All bonds come with a face value of $100. In order to price Bond A:

1. Calculate the yield to maturity of Bonds B and C.

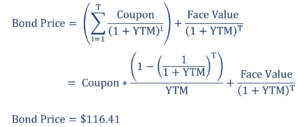

2. The estimated market discount rate of the 6-year 10% bond is the arithmetic mean of YTMB and YTMC. Therefore, YTMA = (11.46% + 1.74%) / 2 = 6.6%. An alternative method to calculate YTMA is to take the geometric mean of YTMB and YTMC.

3. Therefore, the estimated market price of Bond A is given by the following formula:

The estimated market price of Bond A based on Bonds B and C is $116.41. The estimation method is called matrix pricing because it uses a matrix like the one shown above.

Thank you for reading CFI’s guide on Matrix Pricing. To keep learning and advancing your career, the following resources will be helpful: