Get Certified for

Capital Markets (CMSA®)

From equities and fixed income to derivatives, the CMSA certification bridges the gap from where you are now to where you want to be — a world-class capital markets analyst.

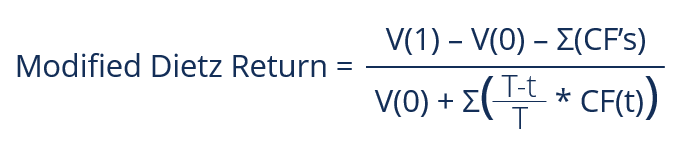

The Modified Dietz Return calculates the rate of return of an investment portfolio which includes the cashflows in and out of the portfolio

In modern portfolio theory, the Modified Dietz Return or Modified Dietz Method (“MDM”) is a commonly used algebraic method used to calculate the rate of return of an investment portfolio that includes the cash flows of the portfolio.

The method accounts for the timing of when the cash flows come in and out of the portfolio in order to properly weigh the impact of these cash flows on the portfolio’s return.

The MDM is considered to be an extremely precise and exact measurement of portfolio returns due to accounting for timing, as opposed to the Simple Dietz Method, which assumes that all cash flows are collected in the middle of an investment period.

Unlike the Modified Internal Rate of Return and the Internal Rate of Return (IRR), the Modified Dietz Return is not an expected return and is backward-looking, doesn’t use expected value, and calculates the realized return of the portfolio.

Named after Peter O. Dietz – an academic whose works were extremely influential in measuring the returns of pension investment funds – the Modified Dietz formula was created to better understand and provide more transparency for the return an investment portfolio made. This statistic has been around since the 1960s when computers weren’t as common to calculate exact returns.

Investment portfolios constantly see cash flows coming in and going out, such as transfers of cash, securities, or other instruments. This makes it hard to track of how much money the portfolio made. Thus, the Modified Dietz Return formula was created to incorporate the timing and magnitude of the cash flows throughout the entire investment horizon.

Hence, the MDM takes several factors into account, including:

Simply put, in any given time period, flows that occur earlier in the period would have a higher weight on the return of the portfolio when compared to flows that happened later in that same time period.

The Modified Dietz Method is widely used by investment companies in reporting returns for investors. In particular, the MDM is a very good approximation of an investment’s money-weighted rate of return (“MWRR”), which shows the rewards and penalties that an investor receives from the individual timing of their contributions and withdrawals.

As part of the CFA Institute’s Global Investment Performance Standards (“GIPS”), the Modified Dietz Return is one of the acceptable calculation methods of calculating daily-weighted external cashflow adjusted returns.

Where:

One of the main components of the formula is its ability to account for the timing of cash flows. The formula accounts for such a fact by taking the sum of the weighted cash flows, weighted by when they occurred throughout the investment horizon.

It is achieved by taking the difference between the length of the investment horizon (T) and the timing of the cash flow (t) and dividing the difference by the investment horizon (T), then multiplying the result by the magnitude of the cash flow that happened at t; the product will be the weighted cash flow.

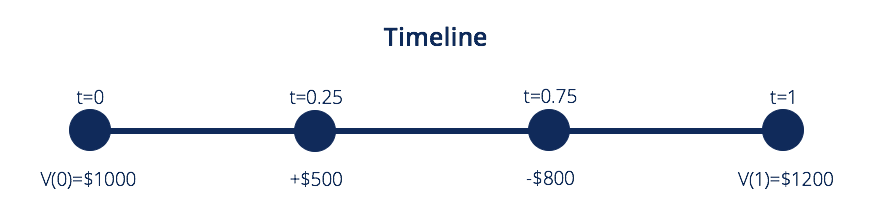

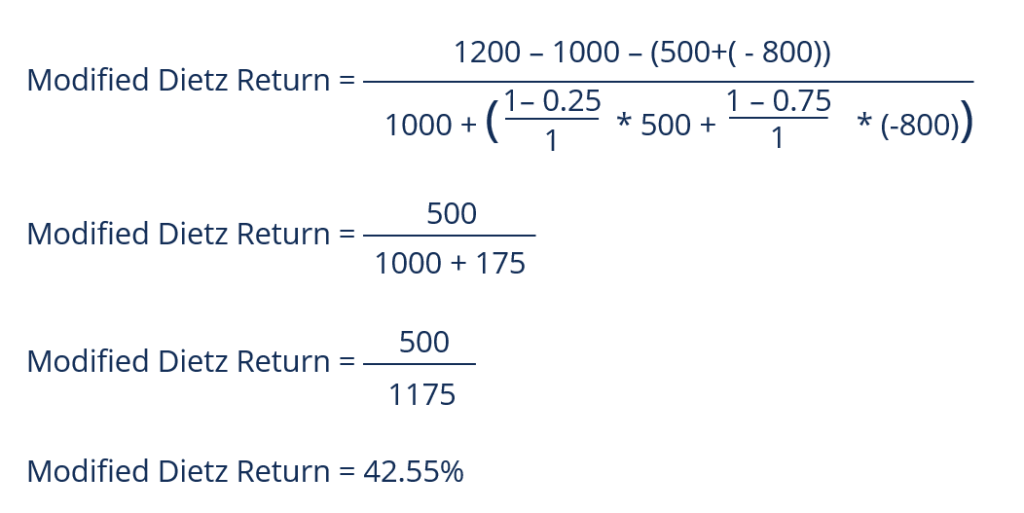

An individual invests $1,000 in an investment portfolio for one year. At the end of the year, the portfolio rose in value to $1,200. During the investment horizon, at the end of the first three months, the investor deposited $500 into the portfolio.

However, at the end of the nine-month period, the investor withdrew $800. To understand the portfolio’s performance, the investor must calculate the rate of return that accounts for the timing of the withdrawals and deposits made.

Thus:

The Modified Dietz Return formula exhibits disadvantages when one or more large cash flows occur during the investment period or when the investment is very volatile, and experiences returns that are significantly non-linear. Another disadvantage is that the investor needs to know the value of the investment both at the beginning and end of the investment horizon.

Additionally, the investor must adopt a way to keep track of the cash flows coming in and out of the portfolio. It is important to know when to use the Modified Dietz Return to get an accurate understanding of how the investment portfolio performed.

Thank you for reading CFI’s guide on Modified Dietz Return. To keep advancing your career, the additional resources below will be useful: