Get Certified for

Capital Markets (CMSA®)

From equities and fixed income to derivatives, the CMSA certification bridges the gap from where you are now to where you want to be — a world-class capital markets analyst.

The change in the value of a security due to a change in interest rates

Modified duration, a formula commonly used in bond valuations, expresses the change in the value of a security due to a change in interest rates. In other words, it illustrates the effect of a 100-basis point (1%) change in interest rates on the price of a bond.

Modified duration illustrates the concept that bond prices and interest rates move in opposite directions – higher interest rates lower bond prices, and lower interest rates raise bond prices.

The formula for modified duration is as follows:

Where:

In order to arrive at the modified duration of a bond, it is important to understand the numerator component – the Macaulay duration – in the modified duration formula.

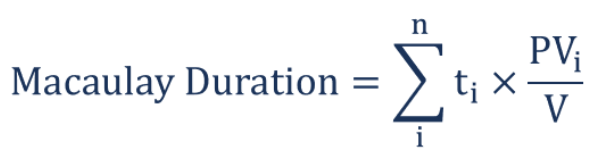

The Macaulay duration is the weighted average of time until the cash flows of a bond are received. In layman’s term, the Macaulay duration measures, in years, the amount of time required for an investor to be repaid his initial investment in a bond. A bond with a higher Macaulay duration will be more sensitive to changes in interest rates.

The formula for Macaulay duration is as follows:

Where:

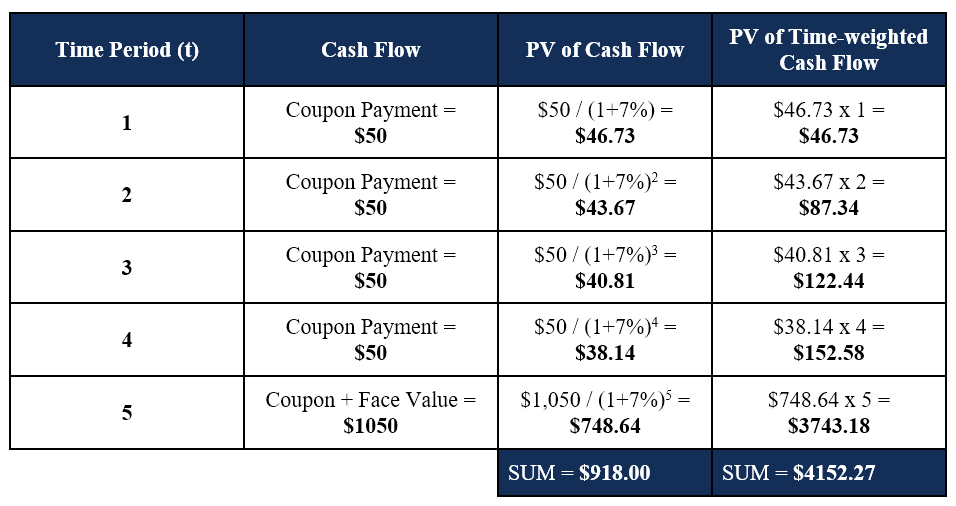

Below is an example of calculating Macaulay duration on a bond.

Tim holds a 5-year bond with a face value of $1,000 and an annual coupon rate of 5%. The current rate of interest is 7%, and Tim would like to determine the Macaulay duration of the bond. The calculation is given below:

The Macaulay duration for the 5-year bond is calculated as $4152.27 / $918.00 = 4.52 years.

Now that we understand and know how to calculate the Macaulay duration, we can determine the modified duration.

Using the example above, we simply insert the figures into the formula to determine the modified duration:

The modified duration is 4.22.

How do we interpret the result above? Recall that modified duration illustrates the effect of a 100-basis point (1%) change in interest rates on the price of a bond.

Therefore,

The modified duration provides a good measurement of a bond’s sensitivity to changes in interest rates. The higher the Macaulay duration of a bond, the higher the resulting modified duration and volatility to interest rate changes.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

Thank you for reading CFI’s guide on Modified Duration. To keep advancing your career, the additional resources below will be useful: