Get Certified for

Capital Markets (CMSA®)

From equities and fixed income to derivatives, the CMSA certification bridges the gap from where you are now to where you want to be — a world-class capital markets analyst.

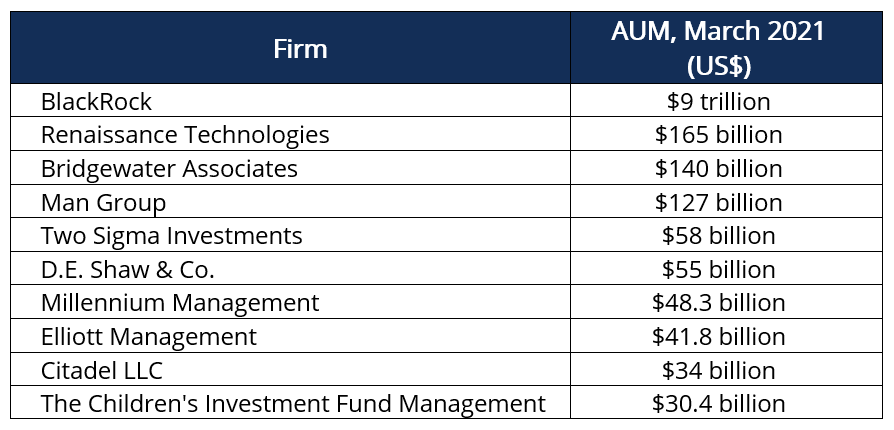

A quant fund uses mathematical and statistical techniques, as well as automated algorithms and advanced quantitative models, to invest and execute trades

A quant fund (short for quantitative fund) is an investment fund that uses mathematical and statistical techniques together with automated algorithms and advanced quantitative models to make investment decisions and execute trades. There is no human intellect and judgment involved in investment selection and related decisions.

Quant funds operate using computer-based models, which mitigate risks and losses related to human fund management. The funds are often considered to be a form of alternative investments because they are non-traditional by nature. Just like any other investment fund, quant funds aim to outperform the market by placing funds with liquid and publicly traded assets in a superior way. In financial terms, the goal is to generate alpha (excess return).

Quantitative theory, which is the backbone of quant funds, was originally applied to finance by Robert Merton. Quantitative finance combined with mathematics (calculus) led to developments such as the modern portfolio theory, the Black-Scholes option pricing model, and other strategies.

The quantitative models used by quant funds are designed to detect investment opportunities in the market. Hence, competition between quant developers is to create a more superior model. The complex mathematical models carry out the buy/sell decisions without human intervention.

Quant funds use algorithmic investment strategies that are systematically programmed to manage a fund and make investment decisions. There is no direct intervention of human fund managers with their judgments, experience, opinions, and emotions.

Quant funds use quantitative analysis compared to traditional funds that use fundamental analysis. Quant strategies are often called Black Box due to the level of secrecy surrounding their algorithms. Quant models also work best when they are back-tested, and they are said to perform better in bull markets but perform like other generic strategies in bear markets.

The substantial growth of quant funds in recent years can be attributed to several factors, including big data solutions and greater access to a wider range of market data. Quant fund models are more efficient and effective with more data than less, which made the big data age an opportune period to complement their growth.

The advancements and innovation in technology and automation also positively impacted the growth of quant funds by augmenting the data that they could work with. It enabled quant funds to receive strong feeds for a comprehensive analysis of scenarios and sensitivities. Quants use proprietary models to increase their chance of beating the market. There are also off-the-shelf programs that can be obtained for funds that require simplicity.

A quant fund is a hybrid of passive index funds and actively managed funds as it carries characteristics of both in terms of management. In a passive fund, the fund manager decides the timing of entry and exit of an investment. In quant funds, the timing decisions are made by the computer programs.

The quantitative investment process is usually broken down into three essential stages, i.e., input system, forecasting engine, and portfolio construction.

This stage is where all the necessary inputs are provided. They include market data, rules, and company data. Market data includes interest rates, inflation, GDP growth rate, etc. Company data includes revenue growth, earnings growth, cost of capital, dividend yield, price-earnings, etc.

At the input stage, stocks with undesirable factors such as high volatility, huge debt burden, inefficient capital allocation, and other related factors are removed from the quantitative model. This is an initial screening mechanism used to remove the undesirable elements beforehand and leave companies that are more likely to generate alpha. The model rules are also defined at this juncture.

The forecasting stage is where estimations for expected return, price, risk parameters, and other factors are generated. The evaluation of stocks is also done at this stage.

The portfolio composition and construction occur at this stage. The composition is done using optimizers or heuristics-based systems. An optimum portfolio is constructed by the quantitative model by assigning an appropriate weight for each stock to generate desired returns and reduce risk at acceptable levels.

Quant strategies are formulated to identify and target the underlying factors responsible for the outperformance of certain assets over others or the market. The quant model describes the underlying factors and back-test models to show factors that are viable for analysis.

The model is then implemented based on a set of defined rules that assist in screening assets to be included in a portfolio. Hence, quants will aim to identify the factors and design strategies that best extract them in a process called factor investing. The chief objective is to pursue alpha.

Factors are characteristics inherent in groups of financial assets that describe the different risk/return metrics from the market. Popular factors targeted by quants include low volatility, value, small size, quality, high yield, liquidity, and momentum. The factors are found across sectors and asset classes, historically earning a long-term risk premium. They can be explained by the table below:

Investors can target single-factor models or construct multi-factor portfolios. Quant funds have started allocating assets across factors as opposed to allocating across asset classes as in traditional portfolios. This is because of the observation that asset classes are showing more correlation with each other in contrast to factors that show a high degree of uncorrelation.

The most common quant strategies are smart-beta and risk premia, which are explained below:

Smart-beta refers to investment in portfolios that use a combination of both passive and active investing. The smart-beta approach is similar to an intersection between traditional value investing and the efficient markets hypothesis.

It is a long-only strategy using alternatively constructed indices to exploit market inefficiencies and underlying risk factors. It is factor-driven and can tilt towards one or more factors through reweighting benchmark indices to tilt them towards low volatility stocks which can generate improved risk-adjusted returns that surpass the benchmark. Benchmark indices include the S&P 500 Index or the MSCI Index, which weigh stocks by market capitalization and are proxies for broad market exposure. They also passively show the equity risk premium.

Smart-beta funds are also known as custom indices and can also be constructed using high-yielding quality assets, where stocks are selected according to the strategy rules transparently. Smart-beta funds include a strong beta element, indicating that they are closely correlated to the market.

The risk premia strategy targets factors through long-short trades with the sole purpose of generating absolute returns. The strategy sheds off much of the beta element to deliver positive returns even during bear markets.

Risk premia strategies also employ leverage and derivatives to amplify returns or hedge against risks. A model long-short value strategy involves a long position on undervalued stocks and, at the same time, short-selling the expensive stocks in a portfolio on a price-to-book value basis.

Risk premia strategies offer a higher chance of capturing alpha through a long position on undervalued stocks and short-selling of overvalued stocks, thereby capturing the risk premium from both sides. They are arguably a better strategy than a smart beta strategy.

A risk premia fund can, to a greater extent, eliminate risks associated with market exposure. However, some costs are incurred when short-selling, as it involves borrowing assets. The longer the short position, the riskier and more costly the position can become. It is even more costly shorting small-cap stocks, which results in the portfolio losing the benefits of the size factor.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

CFI is the official provider of the global Capital Markets & Securities Analyst (CMSA)® certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional CFI resources below will be useful: