Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

Assumes that the current fair price of a stock equals the sum of all company’s future dividends discounted back to their present value

The Dividend Discount Model (DDM) is a quantitative method for valuing a company’s stock price, assuming that the current fair price equals the sum of all future dividends discounted to present value.

The dividend discount model was developed under the assumption that the intrinsic value of a stock reflects the present value of all future cash flows generated by a security. At the same time, dividends are essentially the positive cash flows generated by a company and distributed to the shareholders.

Generally, the dividend discount model provides an easy way to calculate a fair stock price from a mathematical perspective, with minimum input variables required. However, the model relies on several assumptions that cannot be easily forecasted.

Depending on the variation of the dividend discount model, an analyst requires forecasting future dividend payments, the growth of dividend payments, and the cost of equity capital. Forecasting all the variables precisely is almost impossible. Thus, in many cases, the theoretical fair stock price is far from reality.

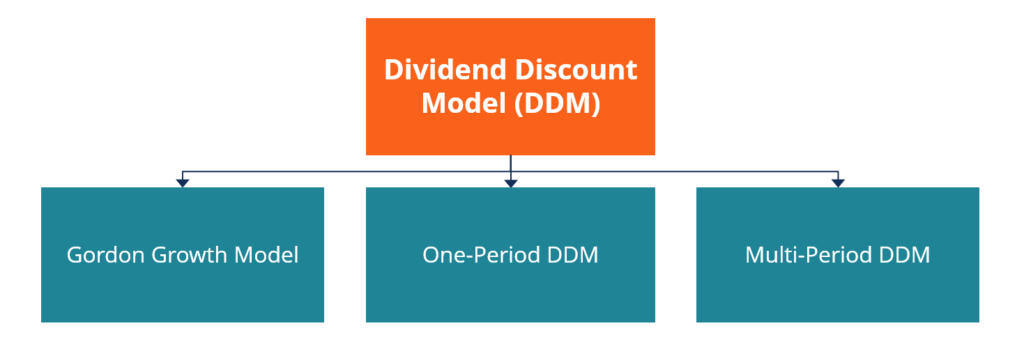

The dividend discount model can take several variations depending on the stated assumptions. The variations include the following:

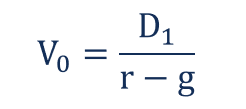

The Gordon Growth Model (GGM) is one of the most commonly used variations of the dividend discount model. The model is called after American economist Myron J. Gordon, who proposed the variation. The GGM assists an investor in evaluating a stock’s intrinsic value based on the potential dividend’s constant rate of growth.

The GGM is based on the assumption that the stream of future dividends will grow at some constant rate in the future for an infinite time. The model is helpful in assessing the value of stable businesses with strong cash flow and steady levels of dividend growth. It generally assumes that the company being evaluated possesses a constant and stable business model and that the growth of the company occurs at a constant rate over time.

Mathematically, the model is expressed in the following way:

Where:

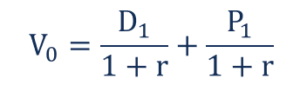

The one-period discount dividend model is used much less frequently than the Gordon Growth model. The former is applied when an investor wants to determine the intrinsic price of a stock that he or she will sell in one period (usually one year) from now.

The one-period DDM generally assumes that an investor is prepared to hold the stock for only one year. Because of the short holding period, the cash flows expected to be generated by the stock are the single dividend payment and the selling price of the respective stock.

Hence, to determine the fair price of the stock, the sum of the future dividend payment and that of the estimated selling price must be computed and discounted back to their present values.

The one-period dividend discount model uses the following equation:

Where:

The multi-period dividend discount model is an extension of the one-period dividend discount model wherein an investor expects to hold a stock for multiple periods. The main challenge of the multi-period model variation is that forecasting dividend payments for different periods is required.

In the multiple-period DDM, an investor expects to hold the stock they purchased for multiple time periods. Therefore, the expected future cash flows will consist of numerous dividend payments and the estimated selling price of the stock at the end of the holding period.

The intrinsic value of a stock (via the Multiple-Period DDM) is found by estimating the sum value of the expected dividend payments and the selling price, discounted to find their present values.

The model’s mathematical formula is below:

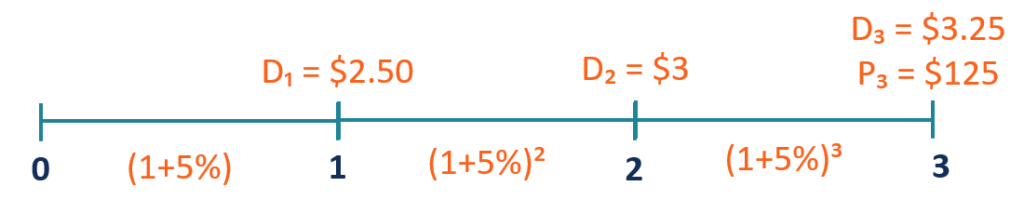

You are an investment analyst. Your client asked you to assess the viability of the investment in ABC Corp. The client expects to hold the investment for three years and sell it at the end of the holding period (end of the third year).

You’ve forecasted that ABC Corp. will pay dividends of $2.50 in the first year, $3 in the second year, and $3.25 in the third year. You expect that at the end of the third year, the selling price of the company’s stock will be $125 per share. The estimated cost of capital is 5%. The current stock price is $110 per share.

In order to assess the viability of the investment, you should determine the intrinsic value of the company’s stock. It can be found using the multiple-period dividend discount model. By inputting the known variables into the formula, the intrinsic stock value can be calculated in the following way:

The intrinsic value of the company’s stock is $115.89, which is more than its current stock price ($110). Therefore, we can say that the stock is currently undervalued.

A shortcoming of the DDM is that the model follows a perpetual constant dividend growth rate assumption. This assumption is not ideal for companies with fluctuating dividend growth rates or irregular dividend payments, as it increases the chances of imprecision.

Another drawback is the sensitivity of the outputs to the inputs. Furthermore, the model is not fit for companies with rates of return that are lower than the dividend growth rate.

The Dividend Discount Model (DDM) is a valuation method asserting that a stock’s fair value equals the present value of all its future dividends. It offers a streamlined way to estimate intrinsic value, requiring only forecasts of dividend payments, growth rates, and the cost of equity.

The DDM can take several variations: the Gordon Growth Model, which assumes perpetual, constant dividend growth; the One‑Period Model, which applies when holding a stock for only one period; and the Multi‑Period Model, which extends valuation across multiple holding periods.

Companies with fluctuating dividend growth rates or irregular dividend payments may find the Dividend Discount Model (DDM) not ideal, because imprecision becomes more likely. Additionally, the sensitivity of the outputs to the inputs makes the model not suitable for companies with a higher dividend growth rate than the rate of return.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

Thank you for reading CFI’s guide to the Dividend Discount Model. To keep advancing your career, the additional resources below will be useful: