Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

Different ways to discount cash flows

All three types of cash flow – FCFF vs FCFE vs Dividends – can be used to determine the intrinsic value of equity, and ultimately, a firm’s intrinsic stock price. The primary difference in the valuation methods lies in how the cash flows are discounted. All three methods account for the inclusion of debt in a firm’s capital structure, albeit in different ways.

Utilizing the provided worksheet, we can illustrate how the different types of cash flows (FCFF vs FCFE vs Dividends) reconcile, how they are valued, and when each type is most appropriately used for valuation.

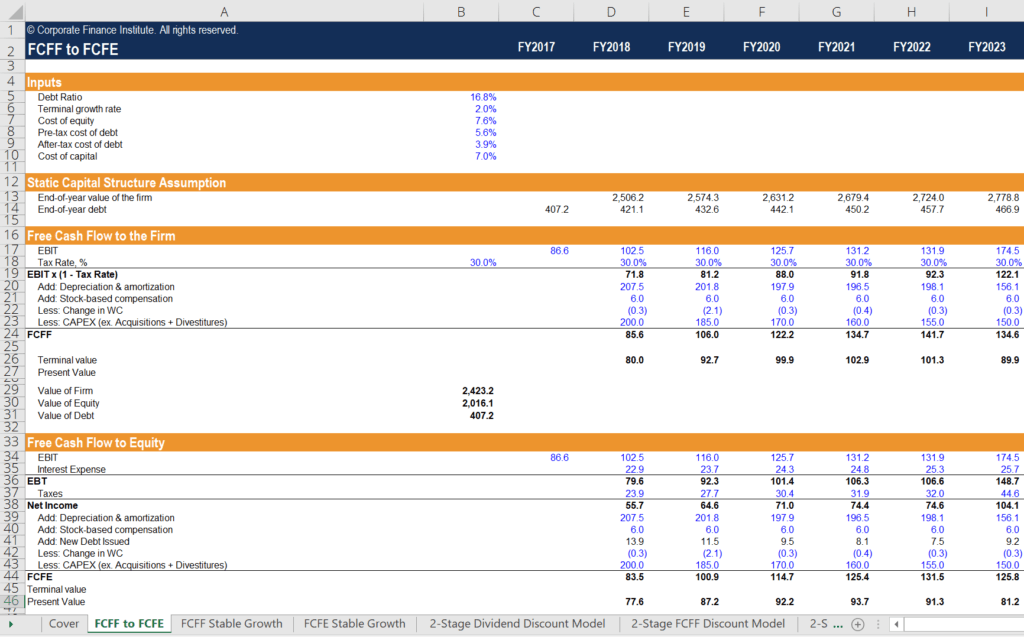

Free cash flow to the firm (FCFF) is the cash flow available to all the firm’s suppliers of capital once the firm pays all operating and investing expenditures needed to sustain its existence. Operating expenditures include both variable and fixed costs necessary to generate revenues. Investing activities include expenditures by a company on its property, plant, and equipment.

They also include the cost of intangible assets, along with short-term working capital investments such as inventory. Also included are the deferred payments and receipts of revenue in its accounts payable and receivable. The remaining cash flows are those that are available to the firm’s suppliers of capital, namely its stockholders and bondholders.

Free cash flow to equity (FCFE) is the cash flow available to the firm’s stockholders only. These cash flows are inclusive of all of the expenses above, along with net cash outflows to bondholders.

Using the dividend discount model is similar to the FCFE approach, as both forms of cash flows represent the cash flows available to stockholders. Between the FCFF vs FCFE vs Dividends models, the FCFE method is preferred when the dividend policy of the firm is not stable, or when an investor owns a controlling interest in the firm.

To reconcile FCFF with FCFE, we must make important assumptions about the firm’s financials and capital structure. First, we must assume that the capital structure of the firm will not change over time. This is an important assumption because if the firm’s capital structure changes, then the marginal cost of capital changes.

Second, we must work with the same fundamental financial variables for both methods. Finally, we must apply the same tax rates and reinvestment requirements to both methods.

The first thing we notice is that we arrive at the same equity valuation with both methods. The first difference between the two methods is the discount rate applied. The FCFF method utilizes the weighted average cost of capital (WACC), whereas the FCFE method utilizes the cost of equity only.

The second difference is the treatment of debt. The FCFF method subtracts debt at the very end to arrive at the intrinsic value of equity. The FCFE method integrates interest payments and net additions to debt to arrive at FCFE.

We hope you’ve enjoyed CFI’s analysis of FCFF vs FCFE vs Dividends. CFI offers the Financial Modeling and Valuation Analyst (FMVA) certification program, designed to transform anyone into a world-class financial analyst. To keep learning and developing your knowledge of financial analysis, we highly recommend the additional CFI resources below:

Below is a break down of subject weightings in the FMVA® financial analyst program. As you can see there is a heavy focus on financial modeling, finance, Excel, business valuation, budgeting/forecasting, PowerPoint presentations, accounting and business strategy.

A well rounded financial analyst possesses all of the above skills!

CFI is the global institution behind the financial modeling and valuation analyst FMVA® Designation. CFI is on a mission to enable anyone to be a great financial analyst and have a great career path. In order to help you advance your career, CFI has compiled many resources to assist you along the path.

In order to become a great financial analyst, here are some more questions and answers for you to discover:

Learn accounting fundamentals and how to read financial statements with CFI’s online accounting classes.

These courses will give you the confidence to perform world-class financial analyst work. Start now!

Boost your confidence and master accounting skills effortlessly with CFI’s expert-led courses! Choose CFI for unparalleled industry expertise and hands-on learning that prepares you for real-world success.