Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

Using prior losses to lower future taxes

A net operating loss (NOL) or tax loss carryforward is a tax provision that allows firms to carry forward losses from prior years to offset future profits, and, therefore, lower future income taxes. The way a tax loss carryforward works is that a schedule is generated to track all cumulative losses, which are then applied in future years to reduce profits until the balance in the TLCF is zero. An NOL carryforward schedule is commonly used in financial modeling.

Tax loss carryforwards exist so that the total lifetime taxes for a firm will, in theory, be the same no matter how their profits and losses are spread out.

A company that had a loss of $10 million in 2018 and a profit of $10 million in 2019 with a 30% tax rate would pay zero tax in 2018 and $3 million in 2019. Its total profit before tax in 2018 and 2019 combined was zero, yet it paid $3 million in taxes.

Compare that to a different company that also had $0 of profit in 2018 and $0 of profit in 2019. This company would pay zero taxes and had a total pre-tax profit of $0.

So why would the first company pay $3 million in taxes while the second company paid none? The first company is much worse off due to the distribution and timing of its profits.

To address this issue, tax loss carryforwards were created.

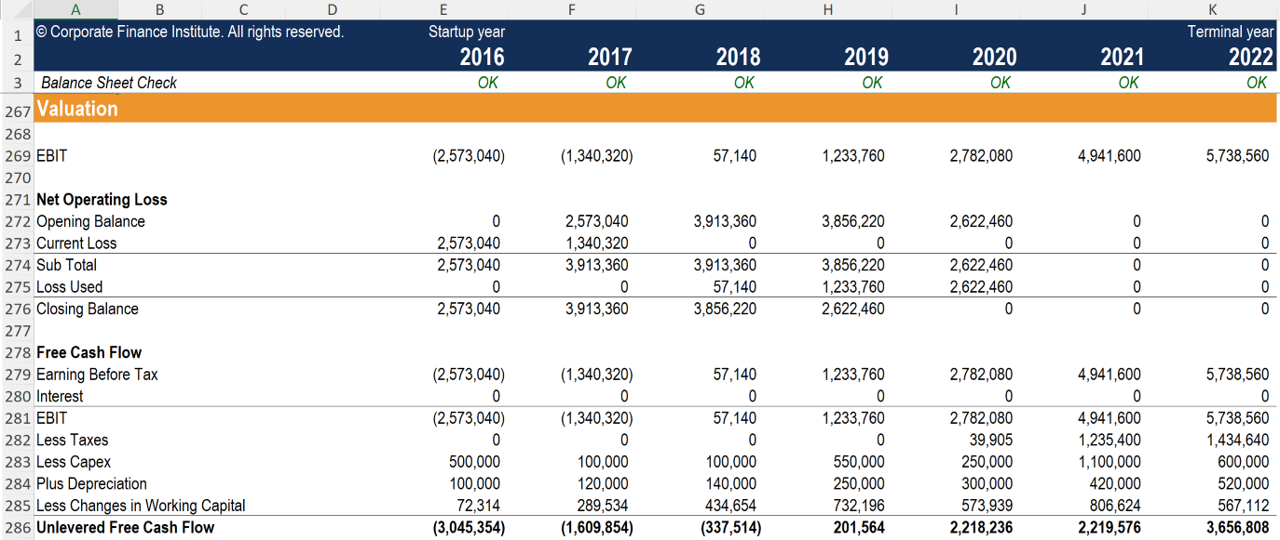

The easiest way to keep track of a TLCF schedule is to create a model in Excel. In the screenshot below, you can see how a financial analyst creates the schedule.

Below is a screenshot of a tax loss carryforward schedule built in Excel. This is taken from CFI’s e-commerce/startup financial modeling course, in which a company has the ability to carry forward losses due to the significant losses expected to be incurred by the business in its first few years of operation.

The best way to learn how to build a TLCF schedule is by practicing. By using the example provided, you can see how it was designed and test yourself to create your own in Excel. If you want a completed example to work with, check out CFI’s financial modeling templates library of completed models from beginner to advanced.

Typically, when an acquisition is structured as a stock acquisition, the acquiring company obtains the ability to use the target’s NOLs going forward. However, there may be limits placed on the usage of these acquired NOLs. For example, in the United States, the usage of acquired NOLs is governed by Internal Revenue Code (IRC) Section 382.

There are two main components of Section 382 — limitation and ownership change. An ownership change occurs when one or more 5% shareholders increase their ownership, in aggregate, by more than 50% over a testing period. Obviously, an acquisition will trigger a change in ownership.

After the acquisition, the acquiring company may deduct the acquired NOLs against its taxable income after calculating the Section 382 base limitation. The formula used in calculating the base limitation amount is:

Fair Market Value of the Target Corporation Stock x Federal Long-Term Tax Exempt Rate = Base Limitation Amount

When calculating the base limitation amount, the fair market value depends on potential adjustments as set forth in Internal Revenue Service (IRS) regulations. The IRS publishes the federal long-term tax-exempt rate monthly.

The base limitation formula drastically limits the usage of acquired NOLs.

Learn more by reading a helpful guide on Internal Revenue Code 382 from Cornell Law School.

Always consult a professional tax advisor before filing any tax forms.

Below is a break down of subject weightings in the FMVA® financial analyst program. As you can see there is a heavy focus on financial modeling, finance, Excel, business valuation, budgeting/forecasting, PowerPoint presentations, accounting and business strategy.

A well rounded financial analyst possesses all of the above skills!

CFI is the global institution behind the financial modeling and valuation analyst FMVA® Designation. CFI is on a mission to enable anyone to be a great financial analyst and have a great career path. In order to help you advance your career, CFI has compiled many resources to assist you along the path.

In order to become a great financial analyst, here are some more questions and answers for you to discover:

Learn accounting fundamentals and how to read financial statements with CFI’s online accounting classes.

These courses will give you the confidence to perform world-class financial analyst work. Start now!

Boost your confidence and master accounting skills effortlessly with CFI’s expert-led courses! Choose CFI for unparalleled industry expertise and hands-on learning that prepares you for real-world success.