Get Certified for

Capital Markets (CMSA®)

From equities and fixed income to derivatives, the CMSA certification bridges the gap from where you are now to where you want to be — a world-class capital markets analyst.

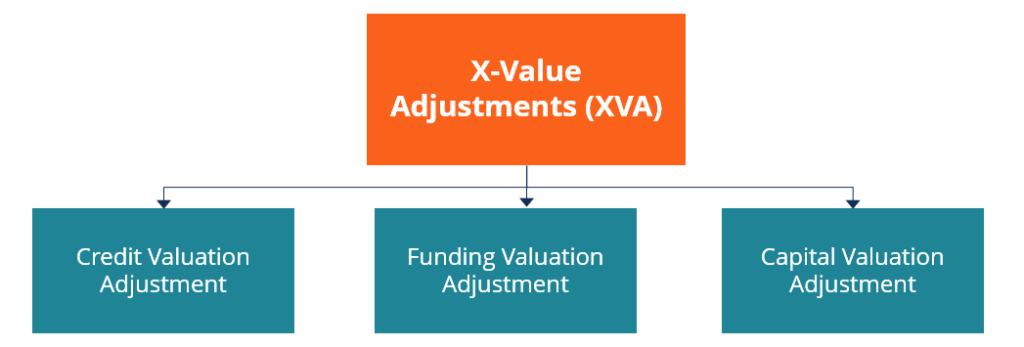

A collective term that covers the different types of valuation adjustments relating to derivative contracts

XVA, or X-Value Adjustment, is a collective term that covers the different types of valuation adjustments relating to derivative contracts. The adjustments are made to account for the account funding, credit risk, and capital costs. When initiating new trades in the derivatives market, traders incorporate XVA into the price of the derivative instrument.

Traditionally, the pricing of derivative instruments relied on the Black-Scholes risk-neutral pricing framework. It was used based on the assumption that funding was done at the risk-free rate. XVA was introduced to deal with the shortcomings of the Black-Scholes pricing model. It adjusts the Black-Scholes frame to account for risks that the model fails to capture.

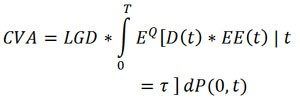

Credit Valuation Adjustment (CVA) estimates the value of counterparty credit risk. It takes into account the possibility that the other party in the transaction will default. It is the difference between the risk-free portfolio and the true portfolio value.

CVA Formula

![]()

Where:

L* is obtained as follows:

![]()

Where:

Assuming that the recovery rate at default is a known constant, the general expression of the CVA is as follows:

The mathematical expression above confirms that there exists a correlation between bank exposure and credit quality of the counterparty.

CVA Desk

In tier one investment banks, a CVA desk is created out of the trading desk. The secret to running a CVA desk is to strike a balance between risk-taking and active hedging. The CBA desk hedges for potential losses caused by a counterparty default. The other function is to reduce the capital required under the Basel III calculation.

FVA refers to the funding cost of an uncollateralized OTC derivative instrument that is priced above the risk-free rate. It concerns estimating the present value of market funding costs into the pricing of a derivative on the first day rather than spreading the cost over the life of the derivative. FVA depends on the size and timing of the underlying exposures and market funding rates

A net funding cost (where FVA is greater than zero) or benefit (where FVA is less than zero) occurs when an uncollateralized derivative is hedged with cleared contracts that require cash collateral. Funding valuation adjustment is influenced by the difference between the bank’s cost of funds and the interest rate used by the clearinghouse. Banks obtain their funds at the LIBOR rate whereas clearing houses uses the risk-free rate on cash deposits.

The following are the main component adjustments of FVA:

The funding benefit adjustment arises when the bank acquires a derivative in a liability position. For example, a bank purchases a derivative with a negative market value in exchange for cash. The cash can then be invested in revenue-generating ventures. In the absence of cash, the bank resorts to raising external funding, which can be costly for the company.

It is the opposite of funding benefit adjustment. A funding cost adjustment arises when a bank acquires a derivative with a positive value. Rather than receiving cash, the bank pays cash for the asset position derivative. The cost incurred to fund the purchase is seen as a form of raising funding for investment.

Capital valuation adjustment differs from credit valuation adjustment. Banks are required by law to hold large capital reserves in preparation for unexpected market and operational losses. Subsequently, BASEL III increased the capital reserve requirements for banks that hold derivative contracts. Credit valuation adjustment captures the additional regulatory capital. The adjustment is associated with all derivative contracts, but it tends to be more punitive on OTC derivative trades that are not cleared.

Currently, there are challenges in using credit valuation adjustments due to differences in capital models among banks. Banks with standard capital models are often restrictive in factoring in future capital changes within the derivatives market.

On the other hand, banks using advanced methods are accommodative of future regulatory capital changes. Such measures are aimed at protecting the bank from writing long-dated contracts that may be affected by future regulatory capital requirements.

Thank you for reading CFI’s guide on XVA (X-Value Adjustment). To keep learning and developing your knowledge of financial analysis, we highly recommend the additional resources below: