S Corporation (S Subchapter)

A closely held corporation (LLC, partnership, or C Corporation) that is treated as a pass-through entity for federal tax purposes

What is an S Corporation (S Subchapter)?

An S Corporation (S Corp) is a closely held corporation (Limited Liability Company (LLC), partnership, or C Corporation) that is treated as a pass-through entity for federal tax purposes. It is created through election to be taxed under Subchapter S of Chapter 1 of the Internal Revenue Code. The tax status does not change the operations of the business, but it means that the corporation will not pay federal income tax; rather, the tax burden will be passed on to shareholders.

The S Corporation elects to pass income, losses, deductions, and credits through to their shareholders for federal income tax reasons. Hence, shareholders will report income, losses, deductions, and credits on their own individual tax returns. LLCs, partnerships, and sole proprietorships can elect to be taxed as S Corporations; however, sole proprietorships need to first convert to a corporation or an LLC before an election to Subchapter S status.

The term S Corporation in full means “Small Business Corporation” and is inextricably very popular with small businesses. S Corporations, as highlighted above, can be LLCs or partnerships that elect to be taxed under section 1362(a) S Corporation tax status (Subchapter S of Chapter 1), enacted in 1958 through Congress. Income is taxed at the shareholder level annually. Therefore, payments to shareholders are distributed tax-free.

To note, however, is that S Corporations are not treated the same in all states. Some states disregard Subchapter S tax status totally, and they do not offer them any tax relief or fiscal advantages. For example, California imposes a 1.5% franchise tax on the net income of S Corps. Some states require additional state-specific modalities and requirements to be completed as a prerequisite for the election of Subchapter S tax status.

In addition to the unique features of S Corporations, they are expected to follow general corporation procedures that apply to C Corporations, such as filing articles of incorporation, holding board and shareholder meetings, voting on major decisions, and similar requirements on the establishment of legal and accounting procedures.

Summary

- An S Corporation is a closely held corporation (LLC, partnership, or C Corporation) that is treated as a pass-through entity for federal tax purposes.

- S Corporations do not pay federal income tax, but the tax burden is passed on to shareholders through shareholder distributions.

- S Corporation shareholders will report income, losses, deductions, and credits on their own individual tax returns.

Mechanics of an S Corporation

The S Corporation works like any other corporation through the relevant by-laws that govern corporations. The major difference is that S Corporations do not pay federal corporate income tax like other corporations. S Corporations pay tax through their individual income tax returns, which is called pass-through taxation.

After filing their Articles of Incorporation, shareholders must file Form 2553 with the Internal Revenue Service (IRS) for the election of Subchapter S status. The form must be signed by all shareholders.

S Corporations submit tax return Form 1120S and Schedule K-1 for each shareholder with the IRS. Schedule K-1 indicates the amount of income received by the respective shareholder annually and forms the basis for the calculation of annual income tax payable.

Filing Requirements for S Corporations

To become an S Corporation, an entity must elect to be taxed as an S Corporation. It is possible whether the business is incorporated as an LLC, partnership, or a C Corporation. The following are the requirements:

- No more than 100 shareholders. Nevertheless, one person can own an S Corporation.

- The entity must be registered within the United States (domestic corporation).

- Shareholders must be individuals (U.S. citizens or legal residents of the U.S.) and certain exempt organizations such as trusts, estates, and charitable organizations.

- Non-resident shareholders, C Corporations, LLCs, and certain partnerships are not permitted to be shareholders of S Corporation. Even other S Corporations cannot be shareholders of an S Corporation unless they own 100% of the target S Corporation.

- S Corporations can only issue one class of stock. It means no preference shares or other types of stock except possibly common stock. However, they can issue voting and non-voting stock.

For more information, check out CFI’s Forms of Business Structure course.

Election Options for Different Entities

The election to be an S Corporation is completed through the following process for C Corporations, LLCs, and sole proprietorships respectively:

- C Corporations – Corporations elect to be taxed as S Corporations through submission of Form 2553: Election by a Small Business Corporation to the IRS.

- LLCs – LLCs file Form 8832: Entity Classification Election and Form 2553. To note is that an LLC does not need to change its corporate form from an LLC; it retains its LLC status but is taxed as an S Corporation. However, LLCs must elect to be taxed as a corporation before it makes the election for S Corporation status under section 1362(a).

- Sole Proprietorship – Sole proprietorships must convert to a corporate status or an LLC before the election of S Corporation status.

Election Window

An election for tax status should be made not more than two months and fifteen days in the year the election is supposed to take effect. Looking at a calendar year, the last day of the election should be March 15th. However, an election can be made anytime during the prior year for election to take effect the following year.

Advantages of S Corporations

1. Limited Liability Protection

S Corporations are separate legal entities that provide limited liability to shareholders. It means shareholders are protected from losing their personal assets and estates from claims by business creditors involving lawsuits and debts. It does not matter if the claims come from contracts or litigation. Hence, S Corporation’s shareholder assets are protected.

2. Pass-Through Taxation

An S Corporation’s income, losses, credits, and deductions are passed through to the shareholders without being taxed at the corporate level. The process is called pass-through taxation, and S Corporations are known as pass-through entities for federal (and other states) income tax purposes.

They benefit by avoiding double taxation of income, which is synonymous with C Corporations, where income is taxed at the corporate level as corporate tax and at the shareholder level as dividend tax. S Corporation shareholders may qualify for a 20% qualified business income (QBI) deduction on their shareholder income.

3. Ability to Receive Salary and Income Distribution

Shareholders in an S Corporation can receive both salaries and income distributions from the company, which will result in a lesser tax bill. An S Corporation deducts salary from company expenses before distributing income to shareholders.

Furthermore, income distributions are not subject to self-employment tax. It is, however, important to know that the IRS may investigate the reasonableness of salaries paid to shareholders, as well as the division between income distributions and salaries.

4. Conversion Made Easy

It easy for S Corporations to easily convert to a C Corporation by filing the required election forms with the IRS.

5. Stock Transferability

S Corporation stock is freely transferable, and shareholders can sell their interest without the need for the approval of other shareholders, nor does it result in adverse tax consequences. It also creates a liquid market for the trading of S Corporation stock.

To learn more, see CFI’s Forms of Business Structures course.

Benefits of S Corporations

S Corporations offer exclusive benefits that are not shared by other corporations, such as:

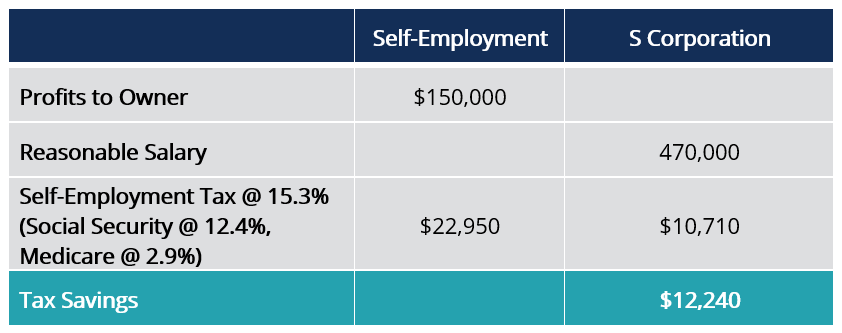

1. Self-Employment Tax Savings

Self-employment tax savings such as Social Security and Medicare are realized for S Corporations. Tax savings can be as much as 15.3% per dollar. Owners will receive reasonable salaries and share of profits, which are not subject to self-employment tax.

The owner of an S Corporation will save a self-employment tax of $12,240 than if they were self-employed.

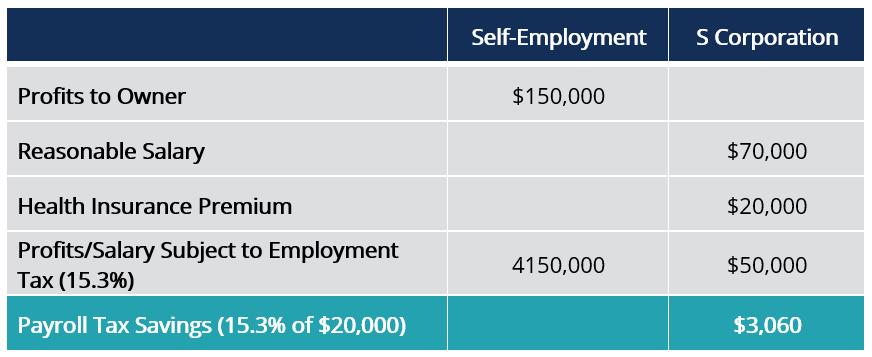

2. Savings on Health Insurance Tax

Shareholders of S Corporations have an opportunity to save additional payroll tax on family health insurance coverage if it is included in their salaries. Spouses are not eligible for coverage under a subsidized health insurance plan.

Salaries that include health insurance premiums are taxable, but the amount of the premium paid is deductible, as premiums are exempt from employment taxes. Hence, employment health insurance premiums are deductible on shareholder income tax returns, resulting in income tax savings.

S Corporation shareholders will be able to save $3,060 in payroll income tax.

3. Personal Expense Deduction Under an Accountable Plan

Shareholder employees are not allowed to deduct personal business expenses on their individual tax returns. However, S Corporation shareholder employees can get reimbursements for their personal expenses from the business. For it to be possible, S Corporations should set up an Accountable Plan that requires personal expenses to be substantiated for business purposes.

4. Deferment of Taxes Under Retirement Planning

S Corporations can provide retirement contributions of 25% of employee contributions or $71,250 (25% of the limit of $280,000) under the Simplified Employee Pension Individual Retirement Arrangement (SEP IRA). There are, however, no catch-up contributions at the age of 50 years plus SEP IRAs.

Contributions should be made on or before the employee tax return is due. Hence, shareholders under S Corporation can defer individual income under 401(k) from taxes. It reduces employer SEP IRAs’ contribution limit.

Nonetheless, the deferred income tax payment will eventually need to be paid. Consequently, the quantum of contributions reduces the SEP IRAs contribution limit, and income withdrawn from the contribution will be eligible for tax.

5. Cash Method Accounting

S Corporations shareholders who don’t own inventory can use cash method accounting instead of the complicated accrual-based accounting. Shareholders can benefit through applying cash-based accounting rules, in which income is taxable when received and expenses are deductible when paid.

Disadvantages of S Corporations

1. One Type of Stock

S Corporations limit stocks to only one type – common stock. Hence, the business is unable to raise funds through other means such as the issuance of preferred stock, etc.

2. Restrictions on Type of Shareholders

There are restrictions on the type of shareholders S Corporations can adopt through limiting ownership to individuals and certain exempt organizations such as trusts and estates. It means non-inclusion of C Corporations, LLCs, and other S Corporations (unless they own 100% of the target S Corp), thereby inhibiting certain institutions with capital.

3. Strict Shareholder Funds Allocation Requirement

S Corporations are required to strictly distribute profits and losses according to the number of shares held by each shareholder. This is different from LLCs, which can share profits; however; they like depending on their circumstances.

4. End of Calendar Year-End

S Corporations are supposed to adopt a fiscal year-end in December. It may disadvantage other entities to operate and report efficiently if December is not a fit for their operations for a year-end month.

Additional Resources

CFI is the official provider of the Commercial Banking & Credit Analyst (CBCA)™ certification program, designed to transform anyone into a world-class financial analyst.

To keep learning and developing your knowledge of financial analysis, we highly recommend the additional resources below:

Accounting Crash Courses

Learn accounting fundamentals and how to read financial statements with CFI’s online accounting classes.

These courses will give you the confidence to perform world-class financial analyst work. Start now!

Boost your confidence and master accounting skills effortlessly with CFI’s expert-led courses! Choose CFI for unparalleled industry expertise and hands-on learning that prepares you for real-world success.