Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

Measures employed by a company to lock out hostile takeover attempts

Shark repellent refers to measures employed by a company to lock out hostile takeover attempts. The measures may be periodic or continuous efforts exerted by management to make special amendments to its bylaws.

The bylaws become active when a takeover attempt is made public to the company’s management and shareholders. It fends off unwanted takeover attempts by making the target less attractive to the shareholders of the acquiring firm, hence preventing them from proceeding with the hostile takeover.

Some takeover attempts can be beneficial to shareholders since the potential takeover gives them an opportunity to maximize their shareholdings’ value, and shark repellent measures deny them that opportunity. However, a successful takeover attempt is also likely to result in the termination of the management’s services and their replacement with a new team from the acquirer’s company.

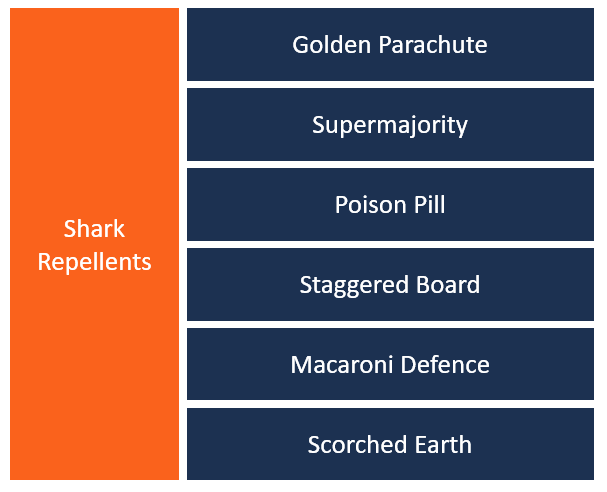

There are several shark repellent measures that companies can take to counter hostile takeovers. Most of the measures are included in the company’s charter and bylaws, which make the company less attractive to acquire. Some common examples of shark repellents include:

A golden parachute involves including a provision in an executive’s contract that gives them a fairly large compensation in the form of cash or stock if the takeover attempt succeeds. The provision makes it more expensive and less attractive to acquire the company since the acquirer will incur a large debt in the sum of money to pay the senior executives.

The clause mainly protects the senior management who are likely to get terminated if the takeover process becomes successful. However, some executives may intentionally insert the clause to make it unattractive for the acquirer to pursue the forced acquisition.

A supermajority is a defense tactic that requires more than an ordinary majority of the shareholders (usually 70%-80%) to approve the takeover. This makes it difficult for the acquiring company to convince shareholders to accept the initiative since the acquirer will be required to purchase a large number of stocks in order to ensure that the takeover will be approved. The supermajority requirement is usually stated in the company’s bylaws, and it becomes activated at any time an acquirer initiates a takeover attempt.

A poison pill is any strategy that creates a negative financial event and leads to value destruction after a successful takeover. The most common form of poison pill is including a provision that enables existing shareholders to buy extra shares at a large discount during a takeover process. The provision is triggered when the acquirer’s stake in the company reaches a certain point (20% to 40%). The purchase of additional shares dilutes the existing shareholders’ stake, making the shares less attractive and making it more difficult and more expensive for the potential acquirer to obtain a controlling interest in the target company.

The tenures of all the directors of the company are staggered over several years, such that the directors of the company are elected at different periods. Some directors are elected every two years, while others serve for a period of four years. Staggering the directors’ tenures makes it difficult for an acquirer to influence a majority of the directors at the same time since the company will elect new members of the board every two years.

The macaroni defense allows the company to sell a large number of bonds that must be redeemed at a future date when an acquirer attempts a takeover against the company. The bonds are redeemed at a high price to make it less attractive for the acquiring entity to proceed with the takeover.

This tactic is borrowed from the military – it involves destroying anything along the way that the enemy might find useful during the battle. The scorched earth strategy is applied during takeover threats by making the company less attractive to the acquirer. It may involve excessive dilution of shares through extreme poison pills.

In 1983, wines and spirits maker Brown Forman Corporation initiated a takeover of Lenox Corporation, a leading producer of bone china ceramics and collectibles, by offering to buy the latter’s shares at $87 each. At the time, Lenox’s shares were trading at $60 on the New York Stock Exchange. In a bid to protect itself from the takeover threat, Lenox offered its shareholders a special cumulative dividend in the form of preferred shares that were convertible to common stock shares.

The proposal would’ve given shareholders the right to purchase additional shares at steep discounts at Brown Forman Corporation if the takeover attempt was successful. The action made the company less attractive to the acquirer since the shares would be diluted when the preferred stocks were converted to shares of the acquirer. Brown Forman Corporation was later forced to raise its offer and get into a negotiated agreement with the directors of Lennox Corporation.

CFI is the official provider of the Financial Modeling and Valuation Analyst (FMVA)™ certification program, designed to transform anyone into a world-class financial analyst. To keep learning and developing your knowledge of financial analysis, we highly recommend the additional CFI resources below: