Get Certified for

Capital Markets (CMSA®)

From equities, fixed income to derivatives, the CMSA certification bridges the gap from where you are now to where you want to be — a world-class capital markets analyst.

How processing errors and biases impact investors

Over 1.8 million professionals use CFI to learn accounting, financial analysis, modeling and more. Start with a free account to explore 20+ always-free courses and hundreds of finance templates and cheat sheets.

Behavioral finance is the study of the influence of psychology on the behavior of investors or financial analysts. It also includes the subsequent effects on the markets. It focuses on the fact that investors are not always rational, have limits to their self-control, and are influenced by their own biases.

In order to better understand behavioral finance, let’s first look at traditional financial theory.

Traditional finance includes the following beliefs:

Learn more in CFI’s Behavioral Finance Course!

Now let’s compare traditional financial theory with behavioral finance.

Traits of behavioral finance are:

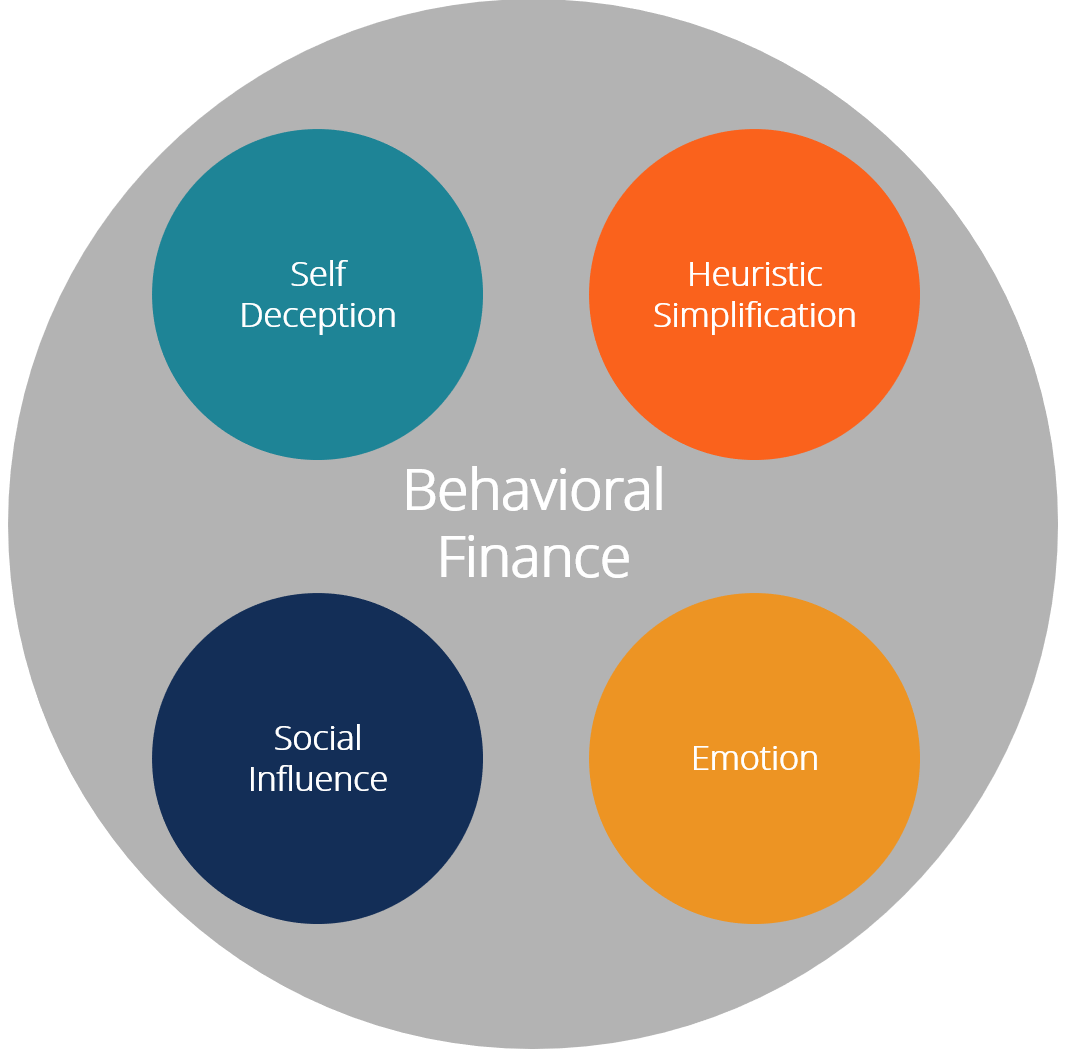

Let’s explore some of the buckets or building blocks that make up behavioral finance.

Behavioral finance views investors as “normal” but being subject to decision-making biases and errors. We can break down the decision-making biases and errors into at least four buckets.

Learn more in CFI’s Behavioral Finance Course!

The concept of self-deception is a limit to the way we learn. When we mistakenly think we know more than we actually do, we tend to miss information that we need to make an informed decision.

We can also scope out a bucket that is often called heuristic simplification. Heuristic simplification refers to information-processing errors.

Another behavioral finance bucket is related to emotion, but we’re not going to dwell on this bucket in this introductory session. Basically, emotion in behavioral finance refers to our making decisions based on our current emotional state. Our current mood may take our decision-making off track from rational thinking.

What we mean by the social bucket is how our decision-making is influenced by others.

Behavioral finance seeks an understanding of the impact of personal biases on investors. Here is a list of common financial biases.

Common biases include:

There are ways to overcome negative behavioral tendencies in relation to investing. Here are some strategies you can use to guard against biases.

There are two approaches to decision-making:

Relying on reflexive decision-making makes us more prone to deceptive biases and emotional and social influences.

Establishing logical decision-making processes can help protect you from such errors.

Get yourself focused on the process rather than the outcome. If you’re advising others, try to encourage the people you’re advising to think about the process rather than just the possible outcomes. Focusing on the process will lead to better decisions because the process helps you engage in reflective decision-making.

Behavioral finance teaches us to invest by preparing, by planning, and by making sure we pre-commit. Let’s finish with a quote from Warren Buffett.

“Investing success doesn’t correlate with IQ after you’re above a score of 25. Once you have ordinary intelligence, then what you need is the temperament to control urges that get others into trouble.”

Learn more in CFI’s Behavioral Finance Course!

Thank you for reading CFI’s guide on Behavioral Finance. To continue learning, these resources will be useful: