Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

A registered company that purchases a portion of or all the rights to another company

An acquirer is a registered company that purchases a portion of, or all the rights to, another company. The acquiring company takes over the management of another company by obtaining a majority stake in the target, effectively giving it control of the company through stock voting rights. Alternatively, the acquirer may simply purchase the company outright.

An acquirer can also be a financial institution that acquires rights to service and manage a merchant’s bank account. The acquirer signs up the merchant and offers to manage their bank account. With the account, a merchant is able to accept credit and debit card payments from clients signed up with various card associations. Some popular card associations include American Express, Mastercard, Visa, Discover, China UnionPay, etc.

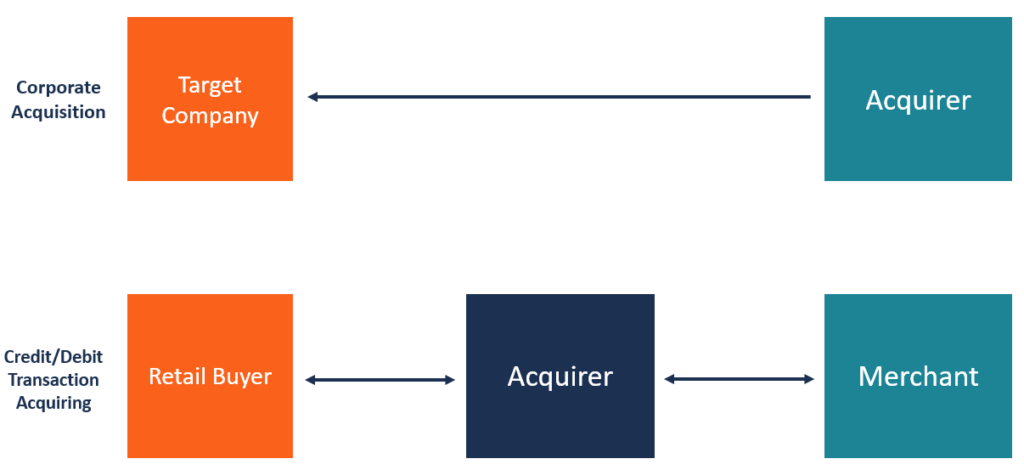

A corporate acquisition is a situation when the acquirer purchases all or part of the shares of another company in order to gain control of the management of the target. The acquirer is able to take over the target company when it acquires more than 50% of the company’s voting stock.

The acquisition often involves buying a majority stake in the company’s stock in order to exert more influence over the decisions of the board of directors. The acquirer believes that, by gaining control of the target, the company will grow its infrastructure and expand its market dominance.

When a company is planning to expand its operations, it considers acquiring an existing company more beneficial than expanding on its own. Rather than starting afresh in a new territory, the acquired company will provide existing infrastructure, personnel, a brand name, and an existing customer base.

This means that the acquirer can start building from the existing resources in order to grow its market share in the new territory. The acquirer will also benefit from cost reductions since it won’t need to spend a lot of money on market research to determine the suitability of the new market.

An acquirer is also known as a merchant bank, an acquiring bank, or a merchant acquirer. An acquirer may be a bank or a financial institution that is a licensed member of a card association such as Visa and Mastercard, and its role is to sign up merchants to allow them to accept electronic payments in their locations. In essence, the acquirer authorizes credit card payments from clients and connects the issuing bank on behalf of the merchant.

When a client makes a credit or debit payment to the merchant, the acquirer must be contacted for the payment to be processed and cleared. The type of payments that the merchant acquirer accepts will depend on the number of their processing relationships with card associations.

If the acquirer holds only one right to a single card processor, it means other branded card processors will not be accepted. Most acquirers typically enter into processing relationships with a network of providers, which allows merchants to enjoy a seamless experience when accepting card payments.

When processing the electronic payment to the merchant’s bank account, the acquirer will charge varying fees as provided in the acquirer-merchant agreement. The fees may be charged per month or per transaction. The fees are used to cover the costs associated with network processing.

The acquiring bank is responsible for creating and managing the merchant account on behalf of the merchant. When a client makes a payment using a credit or debit card, the acquirer must decide whether to approve or reject the transaction based on the information received from the card network and issuing bank.

Once a transaction is made, the acquirer receives an authorization request and then forwards this information to the issuing bank for approval. Once approved, the payment is deposited in the merchant’s bank account. If it is rejected, the payment is reversed to the client’s account, and no amount is deposited in the merchant’s account.

The acquirer also takes the risk for the processed transaction. The acquirer must deal with various payment processing risks that can affect electronic payments. Some of the risks include card chargebacks, card reversals, and card refunds.

A chargeback occurs when there is a dispute between the merchant and the cardholder because the goods or services were not received, goods received were faulty, or other issues arise that question the validity of the transaction. The chargeback is initiated by the cardholder through the issuing bank.

A card reversal occurs when the merchant cancels a previously authorized transaction before any settlements have been made. A card refund occurs when the merchant voluntarily returns the funds to the cardholder for various reasons.

The acquirer is the bank or financial institution that manages the merchant’s bank account. The contract entered into by the acquirer and the merchant allows the latter to accept credit and debit card transactions from cardholders. When a cardholder makes a payment to the merchant, the merchant sends an authorization request to the acquirer, who then sends a request for approval to the specific issuing bank.

The issuer (also known as the issuing bank) is the bank or financial institution that provides credit and debit cards to consumers for use in making electronic payments. The issuing bank issues the credit cards on behalf of card networks such as American Express, Visa, and MasterCard. The issuer provides a line of credit to the cardholder and provides the financial backing for the transactions carried out using the card.

CFI is the official provider of the global Financial Modeling & Valuation Analyst (FMVA)™ certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional CFI resources below will be useful: