EBITDAL

Earnings Before Interest, Tax, Depreciation, Amortization, and Special Losses

What is EBITDAL (Earnings Before Interest, Tax, Depreciation, Amortization, and Special Losses)?

EBITDAL stands for Earnings Before Interest, Taxes, Depreciation, Amortization and Special Losses. It is a non-GAAP measure of a company’s earnings that also accounts for special losses that it usually does not expect to incur on a regular basis.

EBITDAL is a variation of EBITDA but is significant in the sense that it also accounts for special losses that a company incurs during the financial year. It helps evaluate a company’s profitability without considering its financing decisions, accounting decisions, unusual and unforeseen expenses and losses, as well as its tax environment.

What are Special Losses?

Special losses can be referred to as sudden or unexpected expenses incurred by an organization during the financial year. They are non-recurring expenses that arise out of unforeseen events or activities. Special losses are not specifically defined by the Financial Accounting Standards Board (FASB) as EBITDAL is not a GAAP measure.

The losses can be considered as extraordinary or non-recurring items. Special losses can range from unexpected physical destruction on account of a natural disaster to accounting losses brought on by an ill investment decision or the unexpected loss of an asset.

Formula for EBITDAL

EBITDAL is calculated using the profit and loss or income statement. It is not a line item on the income statement but is to be derived by using the line items that are accounted for in the statement.

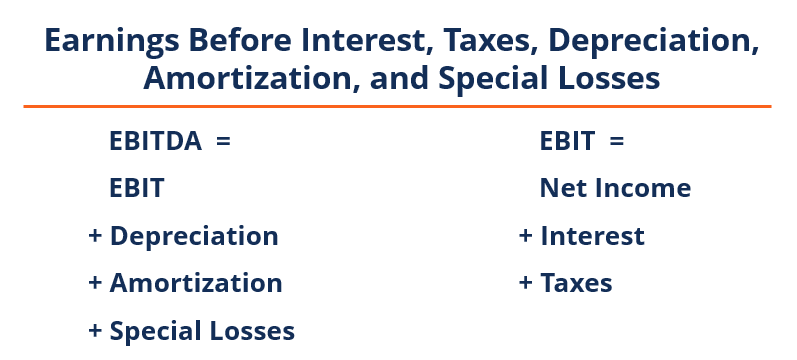

EBITDAL = EBIT + Depreciation + Amortization + Special Losses

Uses of EBITDAL

1. Financial performance

EBITDAL helps measure a company’s financial performance by evaluating its earnings before the inclusion of interest, taxes, depreciation, amortization, and special losses.

2. Comparison

EBITDAL eliminates the direct impact of interest, taxes, depreciation and amortization, and special losses. The calculation of EBITDAL facilitates an easier comparison of the operating performance of companies. It helps the users of financial information analyze a company’s operating decisions by eliminating the effects of the above-mentioned expenses.

Limitations of EBITDAL

1. Deceptive measure

EBITDAL can be a deceptive measure of financial performance. It does not take into account important expenses that are applicable to every organization such as interest, taxes, and depreciation. Hence, it may not provide an accurate picture of the financial strength of an organization.

2. Window dressing

EBITDAL is often used as an attempt to window dress financial results because it eliminates major expenses such as interest and tax. It may be used to boost a company’s profitability while comparing its financial strength to other companies.

3. Financial inaccuracy

Since EBITDAL is not regulated by GAAP, it is up to the financial analyst to decide what to include and exclude in its calculation. Such a practice is especially common in the case of special losses. Hence, it can produce inaccurate financial results.

More Resources

CFI is the official provider of the Financial Modeling & Valuation Analyst (FMVA)™ certification program for those looking to take their careers to the next level. To keep learning and advancing your career, the following CFI resources will be helpful:

Accounting Crash Courses

Learn accounting fundamentals and how to read financial statements with CFI’s online accounting classes.

These courses will give you the confidence to perform world-class financial analyst work. Start now!

Boost your confidence and master accounting skills effortlessly with CFI’s expert-led courses! Choose CFI for unparalleled industry expertise and hands-on learning that prepares you for real-world success.