Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

"The capital structure of a company does not affect its overall value"

The M&M Theorem, or the Modigliani-Miller Theorem, is one of the most important theorems in corporate finance. The theorem was developed by economists Franco Modigliani and Merton Miller in 1958. The main idea of the M&M theory is that the capital structure of a company does not affect its overall value.

The first version of the M&M theory was full of limitations as it was developed under the assumption of perfectly efficient markets, in which the companies do not pay taxes, while there are no bankruptcy costs or asymmetric information. Subsequently, Miller and Modigliani developed the second version of their theory by including taxes, bankruptcy costs, and asymmetric information.

This is the first version of the M&M Theorem with the assumption of perfectly efficient markets. The assumption implies that companies operating in the world of perfectly efficient markets do not pay any taxes, the trading of securities is executed without any transaction costs, bankruptcy is possible, but there are no bankruptcy costs, and information is perfectly symmetrical.

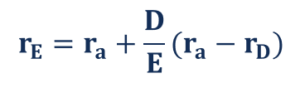

Proposition 1 (M&M I):

![]()

Where:

The first proposition essentially claims that the company’s capital structure does not impact its value. Since the value of a company is calculated as the present value of future cash flows, the capital structure cannot affect it. Also, in perfectly efficient markets, companies do not pay any taxes. Therefore, the company with a 100% leveraged capital structure does not obtain any benefits from tax-deductible interest payments.

Proposition 2 (M&M I):

Where:

The second proposition of the M&M Theorem states that the company’s cost of equity is directly proportional to the company’s leverage level. An increase in leverage level induces a higher default probability to a company. Therefore, investors tend to demand a higher cost of equity (return) to be compensated for the additional risk.

Conversely, the second version of the M&M Theorem was developed to better suit real-world conditions. The assumptions of the newer version imply that companies pay taxes; there are transaction, bankruptcy, and agency costs; and information is not symmetrical.

Proposition 1 (M&M II):

![]()

Where:

tc = Tax rate

The first proposition states that tax shields that result from the tax-deductible interest payments make the value of a levered company higher than the value of an unlevered company. The main rationale behind the theorem is that tax-deductible interest payments positively affect a company’s cash flows. Since a company’s value is determined as the present value of the future cash flows, the value of a levered company increases.

Proposition 2 (M&M II):

The second proposition for the real-world condition states that the cost of equity has a directly proportional relationship with the leverage level.

Nonetheless, the presence of tax shields affects the relationship by making the cost of equity less sensitive to the leverage level. Although the extra debt still increases the chance of a company’s default, investors are less prone to negatively reacting to the company taking additional leverage, as it creates the tax shields that boost its value.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

Thank you for reading CFI’s guide to the Modigliani-Miller Theorem. To keep learning and developing your knowledge of financial analysis, we highly recommend the additional CFI resources below: