Hamada’s Equation

Used to differentiate a levered company’s financial risk from its business risk

What is Hamada’s Equation?

Hamada’s Equation falls under the corporate finance umbrella. It is used to differentiate a levered company’s financial risk from its business risk. It combines two theorems: the Modigliani-Miller Theorem and the Capital Asset Pricing Model (CAPM). Hamada’s equation is structured in a way that helps determine, first, a company’s levered beta, and thus, how best to structure its capital.

The equation gets its name from Robert Hamada, former dean of the University of Chicago Booth School of Business. He received his B.A. in Chemical Engineering from Yale University and his Ph.D. in Finance from the MIT Sloan School of Management.

Summary:

- Hamada’s Equation is a hybrid of the Modigliani-Miller and Capital Asset Pricing Model theorems.

- It is used to help understand how a company’s cost of capital will be affected when leverage is applied.

- Higher beta coefficients mean riskier companies.

The Modigliani-Miller Theorem and the Capital Asset Pricing Model

The Modigliani-Miller Theorem, created by Franco Modigliani and Merton Miller, is the basis for modern capital structure. It simply states that – outside of the costs for bankruptcy, taxes, skewed information, and an inefficient market – a company’s value should not be affected by how it is financed, whether it issues stock or debt.

The Capital Asset Pricing Model (CAPM) says that investors expect to earn money for taking risks and for the time value of money. The risk-free rate of the CAPM makes space for the time value of money. Beta is a measure of potential risk; riskier investments come with a higher beta.

While the statements above are clipped definitions, they give a brief overview and help to explain why Hamada’s equation is a sort of hybrid between the two theorems.

How Hamada’s Equation Works

A levered firm is one that is financed by both debt and equity. Hamada’s equation checks a levered company against an unlevered counterpart. This is useful in a number of areas, including:

- Risk management

- Capital structuring

- Portfolio management

- Finance

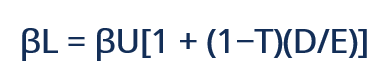

Essentially, it is utilized to understand the cost of capital of levered companies based on capital costs of similar companies. Similar companies would be those with comparable risk and, therefore, similar unlevered betas. Here’s what the formula written out looks like:

Where:

- βL = Levered beta

- βU = Unlevered beta

- T =Tax rate

- D/E = Debt to equity ratio

Why Is Hamada’s Equation Useful?

Hamada’s equation is useful because it is an in-depth analysis of a company’s cost of capital, showing how additional aspects of financial leverage relate to the overall riskiness of the business.

Beta is a metric used to show how risky a system is, and in regard to a company, how risky an operating system is or, more specifically, how risky an investing or financial system is. Investors and financial backers shouldn’t be willing to get behind a company that doesn’t operate on a financially sound plan. The Hamada equation reveals how a company’s beta changes with leverage. If the company’s beta coefficient is higher, it is riskier to invest in.

Additional Resources

CFI offers the Financial Modeling & Valuation Analyst (FMVA)™ certification program for those looking to take their careers to the next level. To keep learning and developing your knowledge base, please explore the additional relevant CFI resources below:

Analyst Certification FMVA® Program

Below is a break down of subject weightings in the FMVA® financial analyst program. As you can see there is a heavy focus on financial modeling, finance, Excel, business valuation, budgeting/forecasting, PowerPoint presentations, accounting and business strategy.

A well rounded financial analyst possesses all of the above skills!

Additional Questions & Answers

CFI is the global institution behind the financial modeling and valuation analyst FMVA® Designation. CFI is on a mission to enable anyone to be a great financial analyst and have a great career path. In order to help you advance your career, CFI has compiled many resources to assist you along the path.

In order to become a great financial analyst, here are some more questions and answers for you to discover:

- What is Financial Modeling?

- How Do You Build a DCF Model?

- What is Sensitivity Analysis?

- How Do You Value a Business?