Valuation Principles

The determination of the fair economic value of a company or business for various reasons

What are Valuation Principles?

Business valuation involves the determination of the fair economic value of a company or business for various reasons such as sale value, divorce litigation, and the establishment of partner ownership.

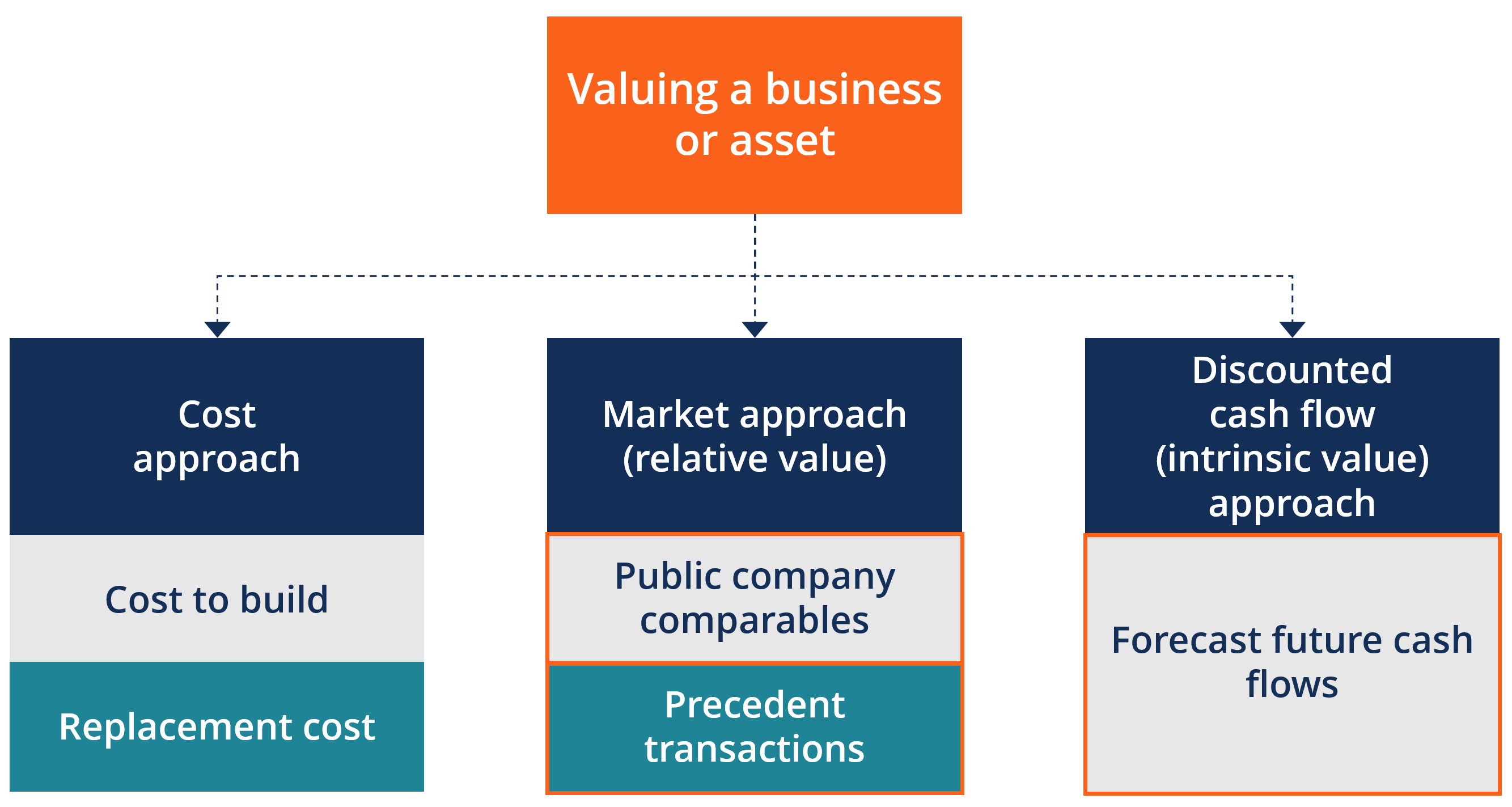

Image: CFI’s Business Valuation Modeling Course.

Key Principles of Business Valuation

The following are the key principles of business valuation that business owners who want to create value in their business must know.

1. The value of a business is defined only at a specific point in time.

The value of a privately-held business usually experiences changes every single day. The earnings, cash position, working capital, and market conditions of a business are always changing. The valuation prepared by business owners a few months or years ago may not reflect the true current value of the business.

The value of a business requires consistent and regular monitoring. This valuation principle helps business owners to understand the significance of the date of valuation in the process of business valuation.

2. Value primarily varies in accordance with the capacity of a business to generate future cash flow

A company’s valuation is essentially a function of its future cash flow except in rare situations where net asset liquidation leads to a higher value. The first key takeaway in the second principle is “future.” It implies that historical results of the company’s earnings before the date of valuation are useful in predicting the future results of the business under certain conditions.

The second key in this principle is “cash flow.” It is because cash flow, which takes into account capital expenditures, working capital changes, and taxes, is the true determinant of business value. Business owners should aim at building a comprehensive estimate of future cash flows for their companies.

Even though making estimates is a subjective undertaking, it is vital that the value of the business is validated. Reliable historical information will help in supporting the assumptions that the forecasts will use.

3. The market commands what the proper rate of return for acquirers is

Market forces are usually in a state of flux, and they guide the rate of return that is needed by potential buyers in a particular marketplace. Some of the market forces include the type of industry, financial costs, and the general economic conditions.

Market rates of return offer significant benchmark indicators at a specific point in time. They influence the rates of return wanted by individual company buyers over the long term. Business owners need to be wary of the market forces in order to know the right time to exit that will maximize value.

4. The value of a business may be impacted by underlying net tangible assets

This principle of business valuation measures of the relationship between the operational value of a company and its net tangible value. Theoretically, a company with a higher underlying net tangible asset value has higher going concern value. It is due to the availability of more security to finance the acquisition and lower risk of investment since there are more assets to be liquidated in case of bankruptcy.

Business owners need to build an asset base. For industries that are not capital intensive, the owners need to find means to support the valuation of their goodwill.

5. Value is influenced by transferability of future cash flows

How transferable the cash flows of the business are to a potential acquirer will impact the value of the company. Valuable businesses usually operate without the control of the owner. If the business owner exerts a huge control over the delivery of service, revenue growth, maintenance of customer relationships, etc., then the owner will secure the goodwill and not the business. Such a kind of personal goodwill provides very little or no commercial value and is not transferable.

In such a case, the total value of the business to an acquirer may be limited to the value of the company’s tangible assets in case the business owner does not want to stay. Business owners need to build a strong management team so that the business is capable of running efficiently even if they left the company for a long period of time. They can build a stronger and better management team through enhanced corporate alignment, training, and even through hiring.

6. Value is impacted by liquidity

This principle functions based on the theory of demand and supply. If the marketplace has many potential buyers, but there are a few quality acquisition targets, there will be a rise in valuation multiples and vice versa. In both open market and notional valuation contexts, more business interest liquidity translates into more business interest value.

Business owners need to get the best potential purchasers to the negotiating table to maximize price. It can be achieved through a controlled auction process.

Key Takeaways

The above are fundamental business valuation principles that determine the value of a business. The value of any business is usually determined at a specific point in time and is impacted by the company’s capacity to generate future cash flow, market forces, underlying net tangible assets, transferability of future cash flows, and liquidity.

Although they are technical valuation concepts, the basics of the valuation principles need to understood by business owners to help them increase the valuation of their businesses.

Related Readings

CFI is the official provider of the Financial Modeling and Valuation Analyst (FMVA)™ certification program, designed to transform anyone into a world-class financial analyst. To keep learning and developing your knowledge of financial analysis, we highly recommend the additional resources below:

Accounting Crash Courses

Learn accounting fundamentals and how to read financial statements with CFI’s online accounting classes.

These courses will give you the confidence to perform world-class financial analyst work. Start now!

Boost your confidence and master accounting skills effortlessly with CFI’s expert-led courses! Choose CFI for unparalleled industry expertise and hands-on learning that prepares you for real-world success.