Get Certified for

Financial Planning & Wealth Management Professional (FPWMP®)

Learn financial analysis & planning, portfolio management, and risk assessment.

A legal method that allows individuals with incomes higher than the Roth limitation to fund Roth IRAs

A backdoor Roth IRA is a legal method that allows individuals with incomes higher than the Roth limitation to fund Roth IRAs. It is also known as “Roth Conversion.” An individual can start by opening and funding a traditional IRA that does not contain any maximum income limitations, and then convert that traditional IRA to a Roth IRA.

The backdoor Roth IRA method is allowed by the International Revenue Service (IRS). Brokerages, banks, and other institutions that provide both traditional and Roth IRAs usually also offer assistance in this conversion.

Unlike in traditional IRAs, there are some restrictions on eligibility for Roth IRAs. One is a maximum income limitation, which may vary for different tax years determined by the IRS. For example, for the 2019 tax year, taxpayers who filed as a single person with a Modified Adjusted Gross Income (MAGI) above $137,000 were not eligible for Roth IRAs.

However, the law changed in 2010, and the IRS now allows high-income taxpayers to convert their traditional IRAs to Roth IRAs. Backdoor Roth IRAs offer an opportunity to those with incomes above the limit but still would like to fund a Roth IRA.

There are several ways to create a backdoor Roth IRA, and many institutions that offer IRA services can assist in the process to ensure steps are completed in compliance with the IRS rules.

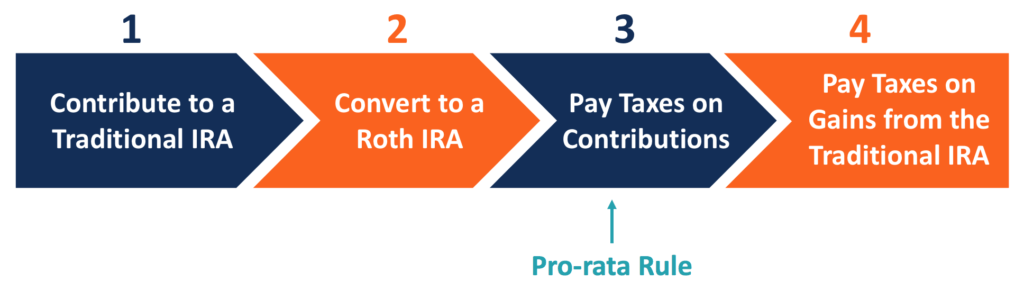

The first step is to open a traditional or another type of IRA with no income limitation and fund the account.

The second step is to make the conversion. It can be done by rolling over the funds that were contributed to the traditional IRA to a Roth IRA. The annual contribution limitation does not apply in this case, so the account owner can roll over as much as they choose. Another way is to convert the account to a Roth IRA entirely.

The next step is to settle the taxes for contributions. The contributions are tax-deductible for a traditional IRA but not for a Roth IRA. The Roth conversion is not a method to avoid taxes, which means the taxes deducted from the contributions made into the traditional IRA must be paid when money is moved into a Roth IRA. The IRS applies a pro-rata rule for the third stage.

The taxes on the rollovers from a traditional to a Roth IRA are determined by the proportion of the pre-tax and after-tax composition in the traditional account. For example, 60% of the money in the traditional IRA is pre-tax, and 40% is after-tax.

When money is converted from that account to a Roth IRA, 60% of that money is taxable no matter how much or from which part the money is converted. The pro-rata rule is implemented to the total IRA balance at the end of a year, regardless of the conversion date.

The traditional IRA might’ve already generated some gains by investing the contributions before it is converted into a Roth IRA. In this case, the account holder also needs to pay taxes for the gains, which are taxable for a traditional IRA. Therefore, brokerages usually suggest account holders start the conversion step immediately before the account begins generating any gains.

A backdoor Roth IRA allows individuals with income above the maximum limit to contribute to Roth IRAs and enjoy the benefits of the type of account. However, the method is not always advantageous, and there are some concerns that account holders need to pay attention to.

In 2017, the reversion of the backdoor Roth IRA (known as “recharacterization”) was banned. An individual must carefully consider whether it is more beneficial for them to hold a Roth IRA before processing the conversion.

The Roth five-year rule applies to the money converted from a traditional to a Roth IRA. After a Roth conversion, the account holder needs to wait for five years before they can withdraw any investment earnings from the account. Otherwise, a 10% penalty must be paid.