Get Certified for

Capital Markets (CMSA®)

From equities and fixed income to derivatives, the CMSA certification bridges the gap from where you are now to where you want to be — a world-class capital markets analyst.

Unit cost averaging, incremental averaging, or cost average effect

Dollar-cost averaging (DCA) is an investment strategy in which the intention is to minimize the impact of volatility when investing or purchasing a large block of a financial asset or instrument. It is also called unit cost averaging, incremental averaging, or cost average effect. In the UK, it is referred to as pound cost averaging.

DCA is a strategy in which instead of making one lump-sum purchase of a financial instrument, the investment is divided into smaller sums that are invested separately at regular predetermined intervals until the full amount of capital is exhausted.

The volatility of a financial instrument is the risk of upward or downward movement, which is inherently present in financial markets. DCA minimizes volatility risk by attempting to lower the overall average cost of investing.

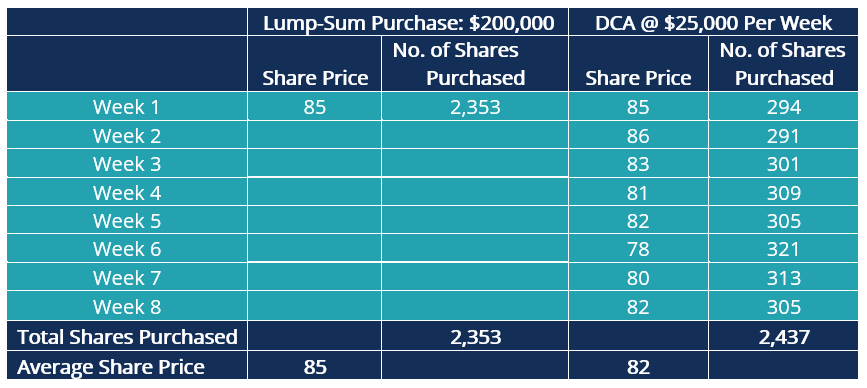

An investment of $200,000 in equities using DCA can be made over eight weeks by investing $25,000 every week in subsequent order. The table below illustrates the trades for lump-sum investment and DCA strategy:

The total amount spent is $200,000, and the total number of shares purchased with a lump-sum investment is 2,353. However, under the DCA approach, 2,437 shares are purchased, representing a difference of 84 shares worth $6,888 at the average share price of $82. Therefore, DCA can increase the number of shares purchased when the market is declining and can lead to fewer shares purchased if the share price is rising.

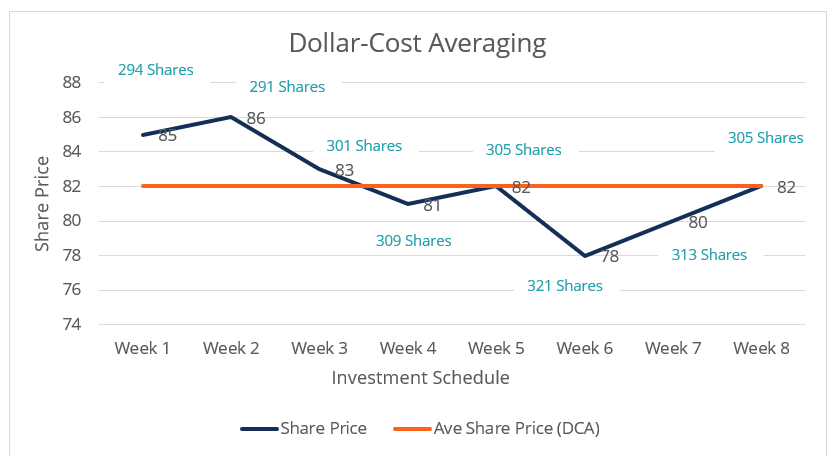

The dollar-cost averaging example above is better explained diagrammatically as below:

Variant strategies for dollar-cost-averaging to maximize profits include scaled-up buying of securities in a downtrend market instead of a fixed amount and periodic purchase. Conversely, in an uptrend market, where shares are bullish, a scaled plan to sell is adopted.

Dollar-cost averaging reduces investment risk, and capital is preserved to avoid a market crash. It preserves money, which provides liquidity and flexibility in managing an investment portfolio.

DCA avoids the disadvantage of lump-sum investing through the purchase of a security when its price is artificially inflated due to market sentiment, which results in the purchase of a lower than required quantity of a security. When the security price discovers its intrinsic price through a market correction or the bubble bursts, an investor’s portfolio will decline.

Some downturns are prolonged, further diminishing portfolio net worth. Using DCA ensures minimum loss and possibly high returns. DCA can reduce regret feelings through its provision of short-term, downside protection against a swift deterioration in a security price.

A declining market is often viewed as a buying opportunity; hence, DCA can significantly boost long-term portfolio return potential when the market starts to rise.

Buying market securities when prices are declining ensures that an investor earns higher returns. Using the DCA strategy ensures that you buy more securities than if you had purchased when prices were high.

Using the DCA strategy by investing periodic smaller amounts in declining markets assists in riding out market downturns. The portfolio using DCA can keep a healthy balance and leave the upside potential to increase portfolio value in the long term.

The strategy of adding money regularly to an investment account allows disciplined saving, as the portfolio balance increases even when its present assets are depreciating. However, a prolonged market decline can be detrimental to the portfolio.

Market timing is not a pure science that many investors, even professional ones, can master. Investing a lump sum at the wrong time can be risky, which can adversely affect a portfolio’s value significantly. It is difficult to predict market swings; hence, the dollar-cost averaging strategy will provide a smoothening of the cost of purchase, which can benefit the investor.

The phenomena of emotional investing brought about by various factors – such as making a huge lump-sum investment and loss aversion – is not unusual in behavioral theory. The use of DCA eliminates or reduces emotional investing.

A disciplined buying strategy through DCA makes the investor focus their energy on the task at hand and eliminates news and information hype from various media about the stock market’s short-term performance and direction.

Sufficient evidence exists that DCA can reduce the average dollar cost if applied with discipline and when favorable market conditions exist. However, other studies dispute the advantages, as well as the feasibility of conducting the DCA investment strategy successfully.

By systematically purchasing securities in small amounts over a certain period, investors run the risk of incurring high transaction costs, which can have the potential to offset the gains accrued by the current assets in the portfolio.

However, it will largely depend on the type of investment strategy, as some mutual funds come with a high expense ratio, which can adversely affect portfolio value in the medium- to long-term period.

DCA critics argue that an investment strategy should focus on the desired asset allocation to manage risk. Pursuing a DCA will further worsen uncertainty, as target asset allocation parameters will take longer to be reached. The economic and physical environments change over time; hence, investors should be able to flexibly realign their portfolios to protect against loss and take advantage of new opportunities.

However, for an investor pursuing DCA, the opportunity may be untenable. It is prudent for investors to place funds in a money market investment account-earning interest and awaiting profitable deployment to other strategic assets within the new desired asset allocation.

The theory of the risk and return dynamics is simple – high risk-high returns and low risk-low returns. Hence, following a DCA strategy to reduce risk will inevitably lead to lower returns. The market typically experiences longer sustained bull markets of rising prices than the opposite. Thus, a DCA investor is more likely to lose out on asset appreciation and greater gains than one that invests a lump sum.

The odds of not being able to attain increased returns are greater than the odds of avoiding overall portfolio value erosion. A study by U.S.-based investment advisor Vanguard in 2012 revealed that historically 66% of the time, a lump-sum investment would’ve produced much higher returns than DCA.

The task of monitoring each scheduled investment over a given time horizon by DCA is a complicated process, especially if, in the end, the difference compared to a lump-sum investment in terms of cost is negligible. The monitoring and tracking of each contribution incur time and energy, making it more complicated than a lump-sum investment.

Dollar-cost averaging (DCA) comes with benefits and drawbacks; however, the desire for a low-risk investment strategy may lead to lower returns.

On the benefits side, it’s possible to achieve a lower dollar-cost average for a security over time rather than a lump-sum investment, provided there are declining markets that do not become protracted.

An investor should aim to include DCA as an optional strategy, among other bolder strategies such as target asset allocation, diversification, and regular portfolio rebalancing.

Thank you for reading CFI’s guide on Dollar-Cost Averaging (DCA). To help you become a world-class financial analyst and advance your career to your fullest potential, these additional resources will be very helpful: