Dormant Account

An account with no activities – such as deposits and withdrawals – for a long period of time

What is a Dormant Account?

A dormant account refers to an account that has shown no activities – such as deposits and withdrawals – for a long period of time. Financial institutions need to make attempts to contact the owners of dormant accounts. If a dormant account has been unclaimed for a certain period of time, the resources held in that account must be transferred to the state’s treasury.

Summary

- An account will turn into a dormant account if it has not had any activities – such as deposits, withdrawals, money transfers, or checks written – for a long period of time.

- Financial institutions and the individual states determine whether an account is dormant, depending on their own policies.

- Financial institutions may charge service fees on dormant accounts. Also, they may automatically close a dormant account with zero balance.

Understanding Dormant Accounts

An account will turn into a dormant account if there has been no activity present for a long period of time. The activities include making deposits, withdrawals, and money transfers, or even simply logging into the account. The automatic posting of interests and dividends cannot be considered an activity.

Besides checking and saving accounts, other types of accounts can also become dormant accounts after being inactive for a certain period. Examples include pension fund accounts, 401(k) accounts, brokerage accounts, and other accounts carried by financial institutions.

The inactive period that turns a general account into a dormant account might be determined by the account providers. Different financial institutions have different dormant account periods, and the policies might change.

For example, the Canadian Imperial Bank of Commerce (CIBC) used to consider an interest-bearing account as a dormant account if it had been inactive (no deposits, withdrawals, or checks written) for 12 months. The bank also considers a non-interest-bearing account to be dormant after being inactive for six months. In February 2020, CIBC changed its policy, extending the period to 24 months for all personal deposit accounts.

Treatment of Dormant Accounts

According to their respective policies, different financial institutions treat their dormant accounts differently. Service fees might be collected on dormant accounts. Usually, the longer an account has been dormant, the higher the annual service fees that are charged.

Banks generally offer bank statements monthly for record-keeping for active accounts. They may charge to offer quarterly statements automatically for dormant accounts. If a dormant account has zero balance, the bank may close the account after a period of time. Accountholders can claim and re-activate their accounts by making deposits, withdrawals, transferring, or making bill payments, as well as contacting the service provider.

In the U.S., state laws set the inactive periods for dormant accounts. For example, brokerage, checking, and savings accounts become dormant after being inactive for at least five years in Delaware. In California, the period of dormancy is much shorter, which is only three years.

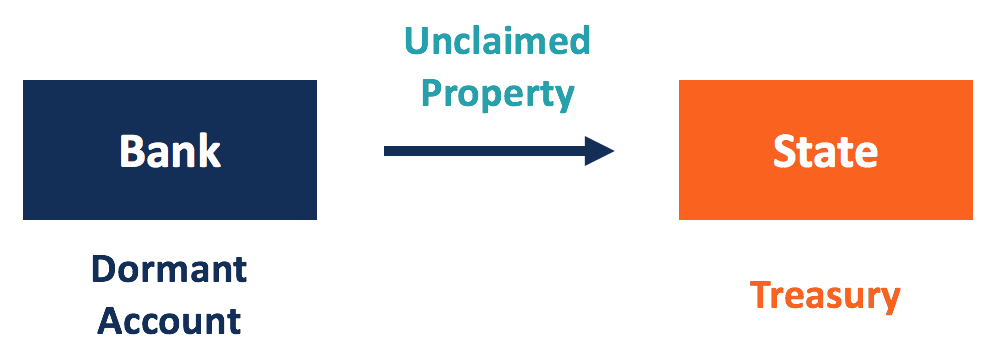

Financial institutions are also required to make attempts to contact the holders of dormant accounts through their most recent contact information. If an account has been dormant for a certain period and the financial institution cannot get in touch with the account holder, the resources held in that account will be considered unclaimed assets. The assets will be transferred to the state’s treasury according to the state’s law.

Escheatment Statute of Dormant Accounts

States apply the escheatment statute to dormant accounts. The escheatment statute gives governments the right to assets when the assets have been unclaimed. Financial institutions are required to transfer the unclaimed property from dormant accounts to the state’s fund for safekeeping.

The states will be responsible for record-keeping and returning the property if it is claimed. Owners need to file applications to claim the property.

Dormant accounts do not fall under the jurisdiction of the statute of limitations. The statute sets a period within which actions must be taken to enforce rights. It means the states will perpetually keep the unclaimed property collected from dormant accounts. Owners or beneficiaries can claim and recover their property at any time.

Related Readings

CFI is the official provider of the global Commercial Banking & Credit Analyst (CBCA)™ certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional CFI resources below will be useful: