Get Certified for

Financial Planning & Wealth Management Professional (FPWMP®)

Learn financial analysis & planning, portfolio management, and risk assessment.

The contribution made from one’s employee salary account to one’s employer-sponsored retirement plan

An elective-deferral contribution is an employee-authorized contribution made from an employee’s salary account to an employer-sponsored retirement plan. The employee needs to provide consent to the employer to deduct contributions. The funds contributed to retirement plans, including 401(k) and 403(b). Elective deferral contributions are a popular way to save for retirement as they have tax advantages and are auto-administered by the employer.

Elective deferral contributions allow for deferring the tax payments on income and investment capital gains. They are the pre-tax income contributions made to employer-sponsored retirement plans, such as 401(k) and 403(b). It allows an employer to deduct money from an employee’s paycheck and deposit it into the employee’s retirement account. The deduction reduces the employee’s pay, but it also reduces their annual taxable income.

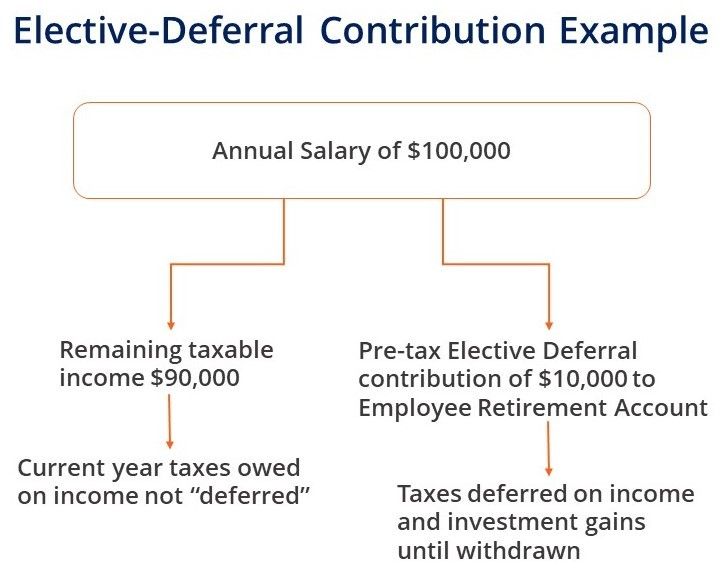

The above figure illustrates how elective deferral contributions work. Say a person with an annual salary of $100,000 contributes $10,000 as an elective deferral to the employer-sponsored retirement plan. It reduces the employee’s annual taxable income to $90,000. Hence, the employee would need to pay tax on $90,000 instead of $100,000. Taxes are deferred on the contributed amount of $10,000 and any derived investment gains until withdrawn from the account.

People usually withdraw at the time of their retirement or in an emergency. A tax penalty is applicable for early withdrawals. For example, an extra 10% tax as a penalty is applicable if an individual makes a withdrawal before age 59 ½. Furthermore, provincial and local taxes may apply for early withdrawals.

Retirement plans are of two types: pre-tax, post-tax accounts, or both. Pre-tax contributions may help reduce taxes during pre-retirement years, while post-tax contributions may reduce one’s taxes during retirement.

A pre-tax contribution is when an employee or employer places money into a retirement account (401(k) or traditional IRAs) before the assessment of taxes. A pre-tax account is also known as a “tax-deferred” account. It defers paying taxes on the contribution amount and the earnings generated until an individual withdraws from the account in the future.

The idea is that one will be in a lower income tax bracket in retirement, which allows more favorable tax rates than one would be during their peak earning years. By deferring taxes, one can reduce their tax bill on the funds in the account.

A country’s revenue service agency establishes contribution limits. For the United States, the Internal Revenue Service established contribution limits for an employee’s qualified retirement plan.

For 2020 and 2021, individuals under the age of 50 can contribute up to $19,500 to their retirement account or 100% of their compensation, whichever is less. Individuals above the age of 50 can make catch-up contributions of $6,500 more for a total of $26,000.

If the employee’s total contributions exceed the deferral limit, the difference is part of their gross income.

The employer can make matching contributions for an employee who contributes elective deferrals (for instance, 30 cents for each dollar deferred). Employer matching contributions can be discretionary (contributed in some years and not in others) or mandatory, depending on the employer’s decision.

The total contributions from both the employee and employer to an employee’s retirement plan cannot exceed the following, whichever is less:

To keep learning and developing your knowledge of financial analysis, we highly recommend the additional resources below: