Get Certified for

Capital Markets (CMSA®)

From equities and fixed income to derivatives, the CMSA certification bridges the gap from where you are now to where you want to be — a world-class capital markets analyst.

Businesses and institutions that manage money and provide intermediary services to transfer and allocate financial capital in an economy

The financial sector refers to the businesses and institutions that manage money and provide intermediary services to transfer and allocate financial capital in an economy.

Every business expansion, home purchase, and investment depends on a financial regulatory framework that moves money efficiently. The sector directs capital where needed most, ensuring economic stability and growth.

Three key banking fundamentals drive the finance sector:

Financial markets would be unpredictable without monetary policy, making growth uncertain.

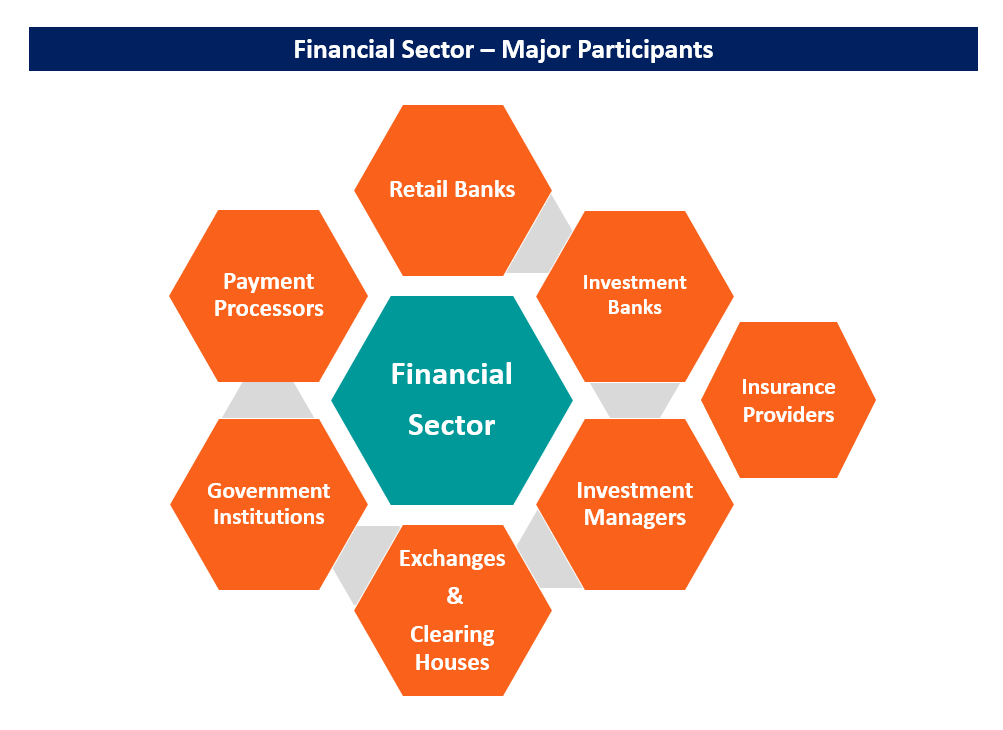

The institutions can be broken down into major categories as follows:

Retail banks are the classic deposit-taking institutions that accept cash deposits from savers and pay interest on those savings. They generate revenue by lending out the deposits to borrowers at a higher interest rate than is paid on savings.

The bank earns the differential between the interest paid on deposits and the interest earned from loans. Some well-known examples of retail banks worldwide are Bank of America, Royal Bank of Canada, BNP Paribas, Mitsubishi UFJ, and HDFC Bank. They are also known as commercial banks.

Investment banks are non-deposit-taking institutions that primarily focus on corporate finance. They provide advisory services to businesses to help them raise funds from the financial markets, e.g., helping a company raise equity via an Initial Public Offering (IPO). They also offer other services like prime brokerage, which are brokerage services like securities lending to large institutional clients.

Investment banks generate revenue primarily through fees earned from advisory and underwriting services. They also generate profits through trading in the financial markets.

Most commercial banks oversee an investment banking arm, though more recently, they are required to separate the two business units under the Dodd-Frank Act and other laws. Some well-known investment banks include Morgan Stanley, Barclays, and Goldman Sachs.

Investment managers are professional firms that provide investment management services to individual and institutional clients. They include various players, such as mutual fund and exchange-traded fund (ETF) managers and hedge funds.

Mutual fund and ETF managers primarily serve retail investors by offering pre-packaged investment vehicles. They generate revenue by charging a small fee for managing the total money, also called assets under management.

On the other hand, hedge fund clients are primarily institutions and a few high-net-worth individual investors. The term hedge fund here refers to the many kinds of alternative asset managers, such as private equity and venture capital, commodity trading advisors (CTAs), and highly specialized public markets investors.

Popular examples of investment managers include Fidelity (mutual funds), BlackRock (ETFs), D.E. Shaw (hedge fund), and Carlyle Group (private equity).

The government is a major player in the financial markets. Through its various institutions, it regulates the functioning of the markets. The central bank is the biggest and most influential government institution in any financial market

A central bank is the sole issuer of legal tender or currency in an economy. It also controls the interest rates in the domestic market and, in many cases, the exchange rate for a currency in the foreign exchange (FX) markets.

Outside the central banks, some securities regulators establish rules to regulate the functioning of financial markets. Securities regulators ensure that the financial markets operate fairly and transparently. To this end, they require elaborate disclosures from various players in the financial markets to ensure transparency and penalize those who engage in illegal activities like insider trading.

Some well-known government institutions include the Federal Reserve (central bank), the Securities and Exchange Commission (SEC), and the Federal Deposit Insurance Commission (FDIC).

These are venues where the actual trading of financial assets takes place. The most common kind of exchange is the stock exchange. For a stock to be traded on an exchange, it must be listed there.

Stock exchanges set specific criteria a company must meet to be listed. They collect orders from market participants and post them in an order book. As buy and sell orders match, trades are executed. Today’s electronic exchanges can execute millions of trades per day.

Clearing houses are responsible for settling accounts between various market participants. They are common in the derivatives market, where many contracts are cash-settled, i.e., one party pays the other based on the price of the underlying security. The clearinghouse assigns the payer, receiver, and amount of payment.

A clearing house is often called the Central Counterparty Clearing (CCP) party. An example is CME Clearing, the clearing house for the Chicago Mercantile Exchange (CME).

Payment processors are intermediaries that facilitate the exchange of funds between disparate parties. They network with various institutions and ensure a secure transfer of funds between them.

Payment processors process most day-to-day electronic transactions. Whenever one uses a debit or credit card, the payment processor securely transmits the transaction information to the user’s bank and routes the funds from the user’s account to the vendor’s account.

Payment processors generate revenue by charging a small fee on every transaction routed through their network. Examples of payment processors include Visa, MasterCard, Interac, and American Express.

Insurance providers encompass another large portion of the financial sector. They protect against unforeseen financial losses arising from accidents and disasters in exchange for a small premium paid regularly. They serve both individuals and institutions.

In the case of individuals, they provide products like life insurance, health insurance, auto insurance, and house insurance. For businesses, they provide products like marine insurance for goods on ships, data breach insurance, worker’s compensation insurance, etc.

There are also reinsurance companies that provide insurance to insurance companies. They help cover an insurance firm’s liabilities in case of a major disaster. Examples of insurance companies include Manulife and Munich Re (reinsurance).

Financial institutions support the economy and are prime investment opportunities. The sector offers a blend of stability and growth potential with options ranging from bank stocks to fintech firms.

Financial companies can act as economic indicators; they thrive when markets are strong and remain resilient in downturns, generating revenue from lending, investment management, and transaction fees. Investors tracking market shifts can benefit from financial market research to stay ahead of industry trends.

By staying informed, investors can capitalize on emerging opportunities in the financial sector.

In macroeconomics, the economy is often modeled as a circular flow between households, companies, and the government.

After the Great Financial Crisis, economists realized that the financial sector exerted a significant influence on the economy and must be included in their models. This led to the development of models that included the financial sector as an integral part of the economy, which was further necessitated by the introduction of unconventional monetary policy by central banks.

The financial industry offers a broad range of career paths, from traditional banking to fintech. Whether you’re interested in investment management, risk assessment, or digital finance, there’s a high-demand role to match your skills.

Success in finance requires analytical expertise, knowledge of emerging markets, and awareness of regulatory frameworks. Certifications can provide a competitive advantage in career advancement.

To counter the effects of an economic depression, central banks use expansionary monetary policy. The policy is implemented by increasing the monetary reserves available in the financial system. The expectation is that the reserves will be used for lending activities, thereby increasing economic activity.

A specific method of implementing monetary policy is known as quantitative easing (QE). Under QE, the central bank purchases high-quality securities from banks in exchange for cash. The cash is then used to meet the regulatory reserves and for increased lending and investment.

The finance sector isn’t just about banks and stock markets; it’s the engine that powers economic growth. Every business expansion, investment, and digital transaction relies on the financial sector’s ability to channel money efficiently. As AI, blockchain, and digital banking reshape the industry, success will belong to those who adapt, innovate, and stay ahead of change.

If you’re serious about advancing your career, now is the time to act. Join thousands of finance professionals who have gained a competitive edge with CFI’s industry-leading certifications. Build the expertise, credibility, and confidence to stand out in the financial services market. Start today—enroll now and take control of your financial future.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

CFI offers the Capital Markets & Securities Analyst (CMSA)® certification program for those looking to take their careers to the next level. To keep learning and advance your career, the following resources will be helpful: