Get Certified for

Financial Planning & Wealth Management Professional (FPWMP®)

Learn financial analysis & planning, portfolio management, and risk assessment.

A legal establishment where the entity’s profits flow directly to the investors/owners and only the investors or owners are taxed for the revenues

A flow-through entity – also known as a “pass-through entity” or “fiscally-transparent entity” – is a legal business entity where its profits flow directly to the investors/owners, and only the investors or owners are taxed on the income. The structure helps avoid double taxation, which is when an income from the same source is taxed both at a corporate and personal level.

A flow-through entity can be categorized into three types:

A sole proprietorship, also known as a sole trader, is a business owned and operated by a single individual. There is no legal distinction between the owner and the company—both operate as the same legal entity.

In such a case, the income of the entity is the same as the income of the sole owner of the entity. This income is reported by the individual in their personal tax returns (Schedule C). The Internal Revenue Services (IRS) also considers this as a disregarded entity since the revenue is treated the same as the owner’s personal income.

A limited liability company (LLC) is a business structure that combines flow-through taxation with limited liability – whereby the owners or partners are not personally responsible for the company’s debt obligations.

The entities are given the option to elect the tax structure that applies to them – a disregarded entity, a corporation, and so on. Several LLCs choose to be taxed as a partnership, where the profits/losses are allocated across the LLC owners/shareholders as per the formal ownership agreement and taxed individually.

S Corporations are closely held forms of LLCs, whereby ownership is limited to certain individuals, trusts, and estates, and less than 100 shareholders.

S Corporations are required to file corporate taxes, but profits are reflected in Schedule E of their personal income taxes. A new law states that from 2018-2025, an S Corporation allows shareholders to claim a 20% deduction from the tax on their share of profit.

There are two major reasons why owners choose a flow-through entity:

The entity’s income only goes through a single layer of tax rather than two – corporate tax and shareholder tax. It allows owners/shareholders to receive higher net returns on their investment.

Individuals generally cannot use the income earned through a source to offset losses from another. However, shareholders of a flow-through entity can deduct business losses from their personal incomes coming through other sources.

Although a flow-through entity brings several advantages to shareholders and owners, some drawbacks also need to be evaluated before a flow-through tax structure is elected for one’s entity.

Specifically, for sole proprietorships, there is always the dilemma in reinvesting the profits of the entity due to the burden falling on personal income taxes – even if the owners do not retain profits or pay dividends to themselves, they are taxed for it due to the direct flow-through.

Also, deducting charitable endowments is a complicated process in a flow-through entity. If a shareholder plans to allocate significant monetary donations to charities, they would be better off adopting the tax structure of C Corporations.

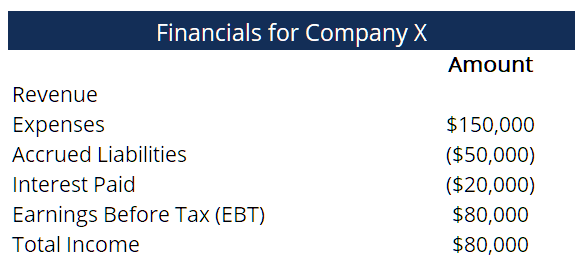

Company X is owned by two businessmen in Los Angeles. The basic financials of X are as follows:

Since it is a flow-through entity, the owners must report their earnings as income when filing personal income taxes. Given that it is a partnership, the income to each owner will be half of $80,000 – both will report an income of $40,000 each.

Assuming they do not receive multiple sources of income and that they aren’t married, as per the U.S. Income Tax Calculator, they would be taxed $6,202. It means, in all, the entity paid around $12,404 (double of $6,202) in taxes, which comes up to a 15.5% tax rate.

If it were not a flow-through entity, the corporate income tax rate applied to the entity’s total income would be 21%, as prescribed by U.S. laws and regulations in 2020. More so, it does not accommodate the additional taxes that would be paid when individual owners file their personal income taxes, thus losing more money compared to the 15.5% tax rate, making the adoption of a flow-through tax structure a beneficial choice.

To keep learning and advancing your career, the following resources will be helpful: