Royalty Trust

A corporation that acts as a mineral rights owner of mineral deposits, wells, and reservoirs

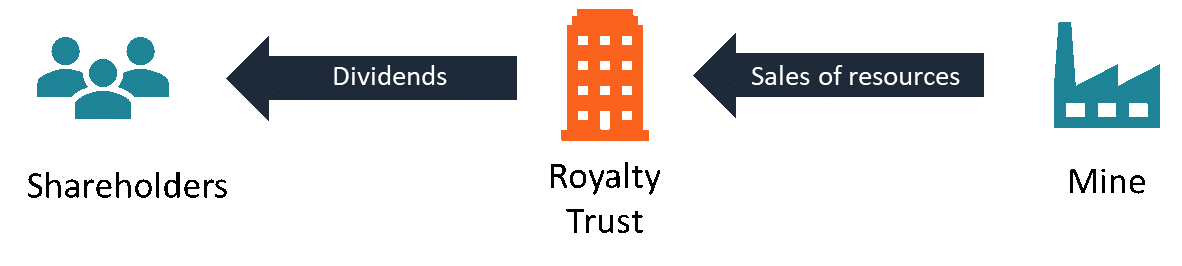

What is a Royalty Trust?

A royalty trust is a type of corporation that usually operates in the energy or resource mining industries and that has ownership rights to mineral deposits, wells, or reservoirs. The main purpose of royalty trusts is to distribute the generated resource sales income to shareholders.

If the major part of the trust’s income (90% or more) is distributed as dividends, there is no income tax to be paid on the corporate level, and shareholders only need to pay personal income tax. This system effectively eliminates the double-taxation problem that commonly applies to corporate income.

Characteristics of Royalty Trusts

Royalty trusts are most common in the United States and Canada. A royalty trust poses as a legal owner of a mining property and its resources, while the actual mining and operations are run by a third party (another company). The trusts don’t employ anyone directly engaged in the mining operations and are usually operated by financial institutions.

Royalty trusts usually own mature, well-developed mines or those that are past their peak. Existing oil and gas mines will gradually deplete, but usually require only minimum investments, while producing a significant cash flow. With relatively high yields, the royalty trust share price tends to drop when interest rates are high and rise during low interest rate periods.

All the abovementioned factors make royalty trusts a favorable option for investors who do not wish to own an actual mine, but who want exposure to the mining industry through stocks that typically offer high-yield dividends. In addition, royalty trusts offer speculative opportunities in the basic materials/commodities sector, without the need to invest in high-risk futures contracts.

Types of Royalty Trusts

Currently, there are two types of such trusts in North America: American and Canadian.

1. American Trusts

In the United States, royalty trusts are not legally allowed to buy any additional property or make any investments after the creation of the trust. Hence, the trusts mainly focus on maintaining existing assets, rather than on expanding their operations.

With depleting resources, this makes American trusts a potentially good short-term investment but may offer little long-term investment potential. Upon the full depletion of the royalty trust’s reserves, the trust will be effectively dissolved. Because of the inability of the trusts to reinvest in themselves, they do not qualify for the recent reduction of dividend income tax (15%).

2. Canadian Trusts

Canadian Royalty Trusts (“CanRoys”) are usually traded on the Toronto Stock Exchange (TSX) and generally provide higher yields than their American counterparts. The legal status of Canadian entities significantly differs from American trusts. In Canada, royalty trusts can be run as businesses and have their own employee base.

In addition, the trusts are allowed to make investments, raise or borrow money, and expand their operations, which makes them more flexible in the long term. However, there are some significant limitations that apply to CanRoys:

- They are mostly only listed on TSX.

- They are affected by the prevailing exchange rate.

- Canada imposes a 15% foreign withholding tax.

With the increased interest in CanRoys in recent years, the Canadian government became worried about losing nearly $1 billion in taxation due to the loophole royalty trusts created for taxpayers. In 2006, the Canadian government introduced Specified Investment Flow-Through (SIFT) rules that eliminated the loophole and required the trusts to pay corporate taxes on their dividend distributions at the full rate of 31.5%.

With the SIFT rule, 90% of CanRoys either transformed themselves into corporations or were simply liquidated. The incident dramatically dropped investor interest in CanRoys. However, with the recent introduction of Foreign Asset Income Trusts (FAITs), which, in essence, are CanRoys that own assets abroad and, therefore, are not subjected to the SIFT rules, the industry may see some revival.

Additional Resources

CFI is the official provider of the global Financial Modeling & Valuation Analyst (FMVA)™ certification program, designed to help anyone become a world-class financial analyst. To keep learning and advancing your career, the additional CFI resources below will be useful: