Get Certified for

Financial Planning & Wealth Management Professional (FPWMP®)

Learn financial analysis & planning, portfolio management, and risk assessment.

A legally binding relationship between a trustor and a trustee

A trust refers to a legally binding relationship in which one party, known as the trustor, gives another party, known as the trustee, the lawful right of property or assets that must be kept and used solely for the third party’s benefit, referred to as the “beneficiary.”

When a trust is established, legal protection is provided to the trustor’s assets. It ensures that the assets will be distributed accordingly to the desires of the trustor, provide tax advantages, and guarantee the privacy of inheritance after death.

Commonly, an individual would set up a trust in order to ensure that their children, grandchildren, or chosen beneficiaries are able to financially benefit from the inheritance they would receive from the trust’s property or assets.

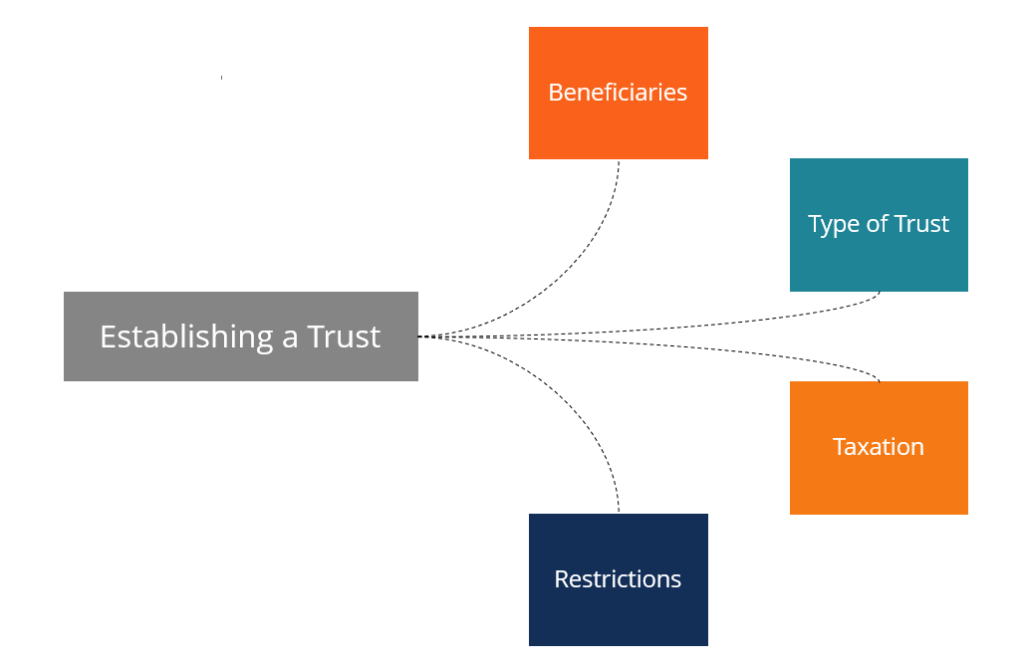

When an individual is thinking about establishing a trust for the eventual security of their loved ones, there is a number of items that the trustor should be aware of.

When establishing a trust, it is important to select the most ethical beneficiaries. In most cases, this is an individual’s family or close relatives.

There are several trusts that have varied restrictions and asset allocation. Choosing the correct trust that benefits both the trustor and beneficiaries is crucial.

Similar to the types of trusts available, taxation slightly changes for each trust. It is important to be aware of the tax treatment on items such as property, income, and financial instruments such as bonds and stocks.

Each trust has a very specific set of rules and restrictions. Before establishing a trust, an individual should be aware of every limitation in order to avoid legal implications.

For example, the mental stability of the trustor becomes a large restriction during the latter years of the trustor’s lifetime.

Establishing a trust fund is very important as it reduces the chances of family conflict, higher tax burdens, and excessive probate costs after an individual passes away.

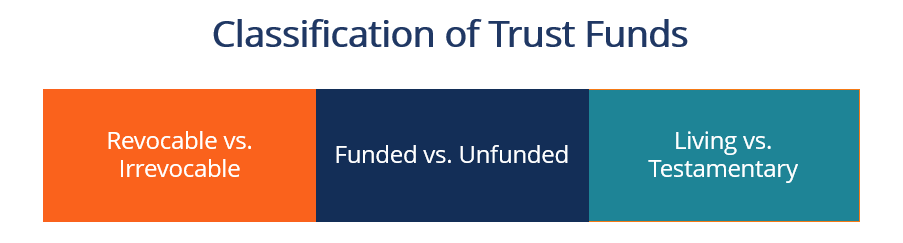

Within the law, there is a wide assortment of different trusts that are available which provide differentiated benefits and protection. For each of them, they will fall into a specific trust classification. They are categorized below:

A revocable trust is a trust that can be altered or terminated by the trustor during their lifetime.

An irrevocable trust refers to a trust that cannot be changed by the trustor once it is initially established. In some cases, a trust may become irrevocable after the trustor’s death.

A funded trust is a specific classification of a trust where assets are consistently put into it by the trustor during their lifetime.

An unfunded trust does not have funding and solely consists of the trust agreement. An unfunded trust can have the opportunity to become funded upon the trustor’s death. When a trust is unfunded, assets may be exposed, making it important to fund a trust.

A living trust, or an “inter-vivos trust,” is a legal document in which the trustor’s assets are used as a trust and can benefit them during their lifetime. The responsibility of these assets is given to the trustee, which is then transferred to the eventual beneficiaries once the trustor passes away.

A testamentary trust, or a “will trust,” is similar to a living trust except for the fact that the trust will only take effect after the death of the trustor, not during their lifetime.

Beyond the baseline classifications of a trust, there is a wide array of specific trust types an individual can choose to establish that all hold varied asset allocation and benefits.

A type of irrevocable trust that is established with only an insurance policy as the asset. An insurance trust is aimed at avoiding estate tax on any of the money that is awarded from the insurance policy after the individual passes away.

A type of trust that allows an individual to leave an amount up to the estate-tax exemption. The remains of the estate pass over to the spouse, without tax consequences.

A trust that allows the beneficiaries to be at least two generations down the bloodline. They are typically the trustor’s grandchildren.

A type of irrevocable trust where the beneficiary is a charitable organization. The organization becomes the trustee, and, as they invest, a regular stream of income can be generated from the trust.

A type of trust that is created for the benefit of a mentally or physically disabled person who will require lifetime care. Advantageously, establishing a special needs trust does not jeopardize any eligibility for supplemental government aid for the beneficiary.

A type of living trust where the beneficiaries are not aware of the assets that are held within the trust. A blind trust is used to reduce potential conflict of interest between the chosen beneficiaries.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

Thank you for reading CFI’s guide to Trusts. To keep learning and developing your knowledge, we highly recommend the additional resources below: