Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

Accounting for companies' investments in market securities

Available for sale securities are the default categorization of securities that companies decide to invest in for the purposes of benefiting their financial position. Unlike trading securities, available for sale securities are not bought or sold for the sole purpose of realizing a short-term capital gain.

They may be purchased as tools to diversify away some of the risks that a company’s investment portfolio currently carries. For example, a company may choose to invest in two industries that exhibit negatively correlated returns or invest in lower beta securities in order to hedge against investment risks.

Available for sale securities can also be bought with the intent to be held for the long-term, rather than realizing a quick capital gain. This investment strategy will rely upon finding undervalued securities that have a lot of upside potential. Available for sale securities can also be used to provide liquidity to a company in case cash is needed to finance its operations, repay its investors, or further develop its investment portfolio.

Available for sale securities can broadly be categorized into the following two categories:

Financing instruments refer to securities that are issued by a company in the form of bonds for the purposes of financing the business’s operations. The securities are recorded as liabilities on the company’s balance sheet since the company is expected to provide a certain return to investors who purchase the securities.

For bond investors, the issuing company is legally obligated to make coupon payments and repay the bondholders the face value of the bond at maturity.

Investment securities are securities purchased by a company for the purpose of making an eventual capital gain or to diversify away some of the risks of the company’s existing investment portfolio.

Companies that operate in a given industry may possess a knowledge advantage over external investors regarding factors that may affect stock prices, which is another reason why companies may choose to invest.

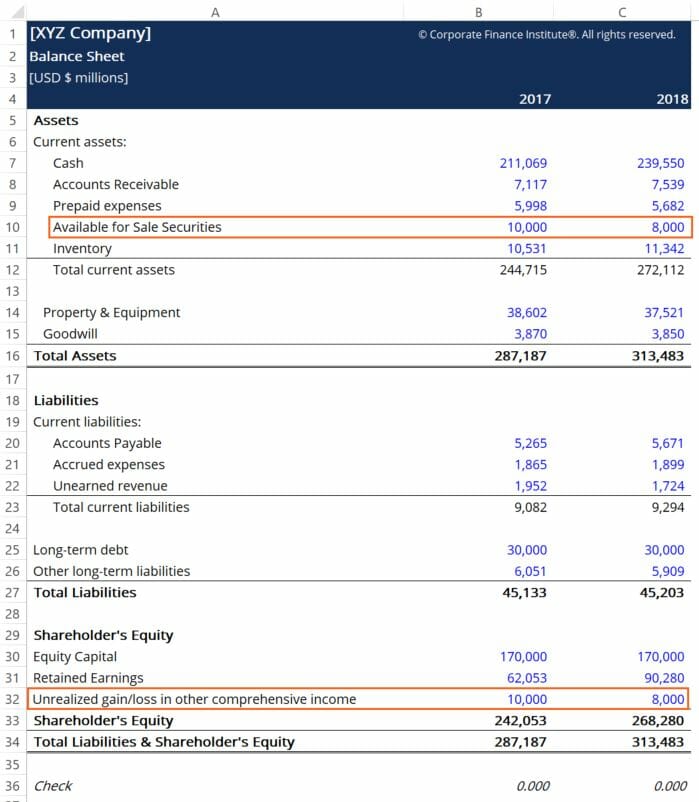

Available for sale securities are treated in the same way that trading securities are on the company’s financial statements, except for one difference. Changes in the fair value of the securities are recorded in an account titled “Unrealized gain/loss in other comprehensive income,” located in the shareholder’s equity section of the company’s balance sheet, as shown:

Journal entries to record changes in the fair value of the securities are also slightly different than with trading securities. The counter account to the “Unrealized Gain (Loss) on Available for Sale Securities” is the “Available for Sale Fair Market Adjustment” account, but both function in the same way as journal entry accounts for the trading securities function. An example is shown below:

Going with our example balance sheet above, we see that the available for sale securities lost $2 billion in value for the company over the course of the 2018 accounting period.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

CFI offers the Financial Modeling & Valuation Analyst (FMVA)® certification program for those looking to take their careers to the next level. To learn more about related topics, check out the following CFI resources: