Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

Profit-and-loss items with no noticeable effect on a company’s annual revenue

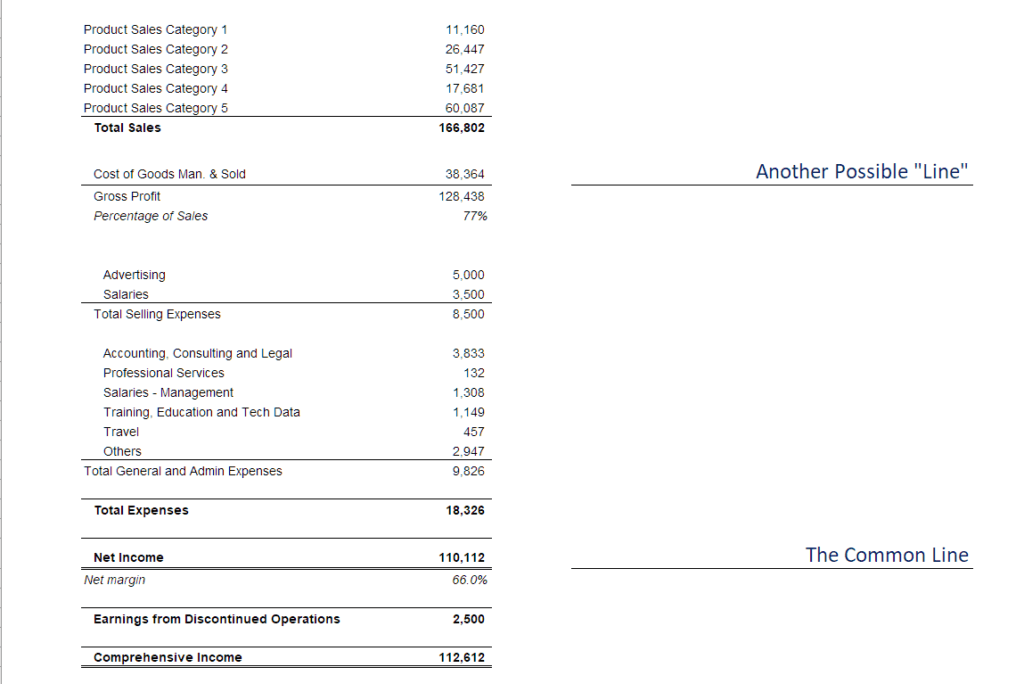

Below the Line refers to items in a profit and loss statement that are income or expense items that are not normally incurred in a company’s day-to-day operations. It includes exceptional and extraordinary items that relate to another accounting period or do not apply to the current accounting period.

Categorizing certain items in the financial statements below the line helps present results from a company’s normal operations separately.

An item is listed on the financial statement as below the line when it is excluded from the gross profit, and, therefore, does not affect the profit or loss from normal operations for that accounting period. For example, a company may earn a substantial non-recurring revenue in one accounting period, a revenue that does not relate to the company’s ordinary course of business.

Alternatively, a company may incur a large non-recurring cost that does not reflect the usual expenses incurred by the company. Excluding these items helps reveal the real financial results of the company without artificially inflating or understating the revenues for the accounting period.

A below the line gain – A company that’s in the business of manufacturing and selling water pumps to wholesalers may decide to dispose of one of its manufacturing plants. The company may sell the plant because it is underutilized or merely to improve its cash flow position. In any event, the company will receive a large, non-recurring revenue after selling the plant that might make the company appear financially healthy even if it is, in fact, in severe financial distress.

Therefore, the revenue should be separated out on the income statement because (A) it is an extraordinary or unusual instance rather than part of the company’s core business, and (B) including it would convey a misleading picture of the company’s actual financial results.

In the example above, we demonstrate the concept of below-the-line expenses or income. The “line” net income – commonly referred to as “the bottom line.” The term “below the line,” however, is often very loosely defined and some people may consider “Gross Profit” to be the “line.” In such cases, below-the-line expenses mean all expenditures that do not affect gross profit but will affect net income.

Exceptional items are gains or losses that are part of a company’s ordinary business dealings but that must be specifically disclosed due to their large size. GAAP requires these items to be noted on the company’s balance sheet for the year. Due to their material nature, exceptional items must be disclosed so that regulators and stakeholders know the actual financial standing of the company.

Exceptional items differ from extraordinary items in that extraordinary items involve gains or losses that are not part of the company’s core business operations. Extraordinary items comprise gains or losses that result from events that are infrequent and unusual. They are not expected to recur in the future and must, therefore, be separated from the ordinary operating expenses or incomes. Such items must be explained in the notes to the financial statements.

In January 2015, the GAAP principles were changed, scrapping the concept of extraordinary items. It eased the preparation of financial statements since accountants were no longer required to distinguish the extraordinary items.

The update also eliminated the need for auditors and regulators to assess if extraordinary items had been identified and classified as required by GAAP. Companies are still required to report and disclose unusual and infrequent transactions and their pre-tax effect on the company’s financials.

Some below-the-line items present companies with an opportunity to manipulate its profitability so that it appears more or less profitable than it is. For example, a company can dispose of one of its assets for a much higher value and use the excess funds to offset an operating loss on the income statement. By taking such an action, the company’s objective is to appear more profitable to investors and regulators than it actually is.

Also, a company may categorize some of the above-the-line expenses in the income statement as below-the-line items, as a way to convince investors that the company is financially stable. If the investors realize that the company is not performing as reported in the accounting books, the company may be investigated by regulators.

An example of a company that practiced creative accounting is Lehman Brothers. The company temporarily moved liabilities off its balance sheet by selling them, although they planned to buy them back immediately.

Above the line items refer to incomes and expenses that relate to the normal operations of a company. Unlike below the line items, these items count when calculating the profit earned or loss incurred during an accounting period.

Above the line may also refer to the gross profit earned by the business. The gross margin is calculated by taking the revenues for the year and deducting the Cost of Goods Sold (COGS). The COGS are the expenses incurred in the normal operations of the business to generate revenues.

They may include the cost of raw materials, wages of workers in the manufacturing line, and other direct manufacturing overheads. The items below the gross profit line are then below the line items that include operating expenses such as facilities rent, salaries, and utilities.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

CFI is the official provider of the global Financial Modeling & Valuation Analyst (FMVA®) certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional CFI resources below will be useful: