Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

A trade agreement in which one party (the consignor) provides goods to another party (the consignee) to sell

Consignment sales are a trade agreement in which one party (the consignor) provides goods to another party (the consignee) to sell. However, the consignee has the right to return unsold goods to the consigner. In other words, a consignment sale is an agreement in which a third party is entrusted with selling goods on behalf of the owner. Consignment sales are also called goods on consignment.

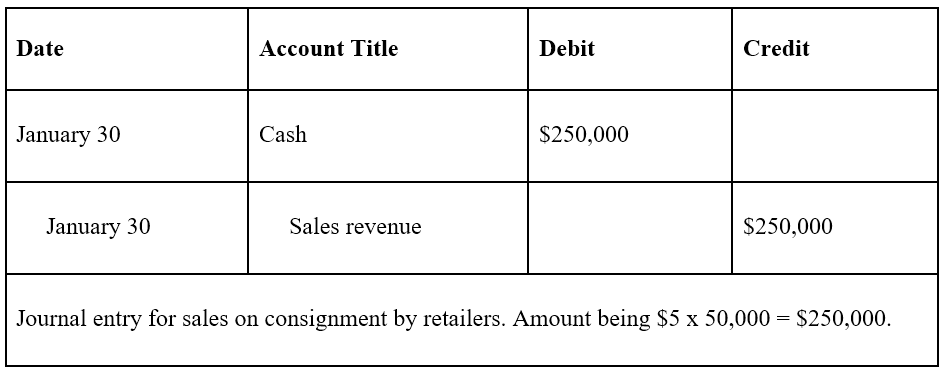

When the consignor sends goods to the consignee, a journal entry is not needed. However, when the consignee sells the goods received, they pay the consignor a predetermined sale amount. The consignor would then record a debit to cash and a credit to sales. They would also purge the related amount of inventory as a debit to cost of goods sold and a credit to inventory.

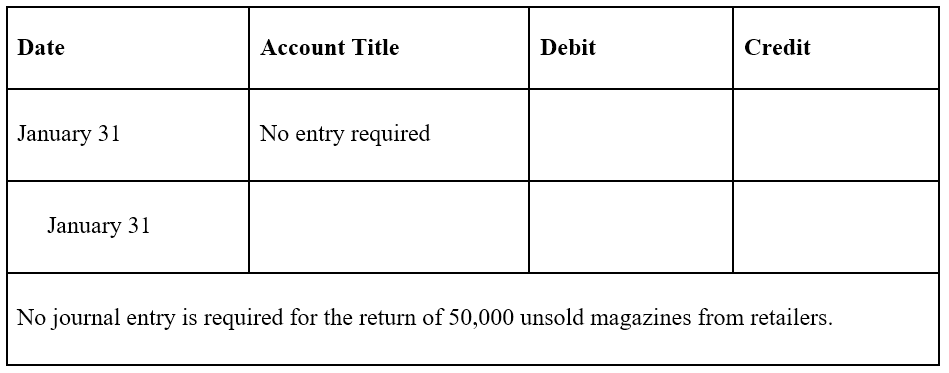

If the consignee is unable to sell all goods, they are able to return the goods to the consignor (before a specified date). Therefore, the consignor bears the risks and rewards of ownership, while the consignee is not required to pay for the goods until they are sold.

On January 1st, Company A sends 100,000 copies of its magazines to retailers to sell on consignment. The company specifies that the deadline to return unsold goods is January 31st. In this scenario, Company A is the consignor, while the retailers are the consignees.

The retail price per magazine is $10, and the price charged by Company A selling to the retailers is $5. Throughout the month of January, the retailers manage to sell 50,000 copies (the retailers notify Company A on January 30th). Therefore, there were 50,000 unsold magazines, which the retailers returned to Company A on January 31st. Additionally, each magazine costs Company A $1 to make.

The journal entries for Company A would be as follows:

Advantages to the consignor are:

Advantages to the consignee are:

Disadvantages to the consignor are:

Disadvantages to the consignee are:

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

CFI is the official provider of the global Financial Modeling & Valuation Analyst (FMVA)™ certification program, designed to help anyone become a world-class financial analyst. To keep learning and advancing your career, the additional CFI resources below will be useful:

Below is a break down of subject weightings in the FMVA® financial analyst program. As you can see there is a heavy focus on financial modeling, finance, Excel, business valuation, budgeting/forecasting, PowerPoint presentations, accounting and business strategy.

A well rounded financial analyst possesses all of the above skills!

CFI is the global institution behind the financial modeling and valuation analyst FMVA® Designation. CFI is on a mission to enable anyone to be a great financial analyst and have a great career path. In order to help you advance your career, CFI has compiled many resources to assist you along the path.

In order to become a great financial analyst, here are some more questions and answers for you to discover: