Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

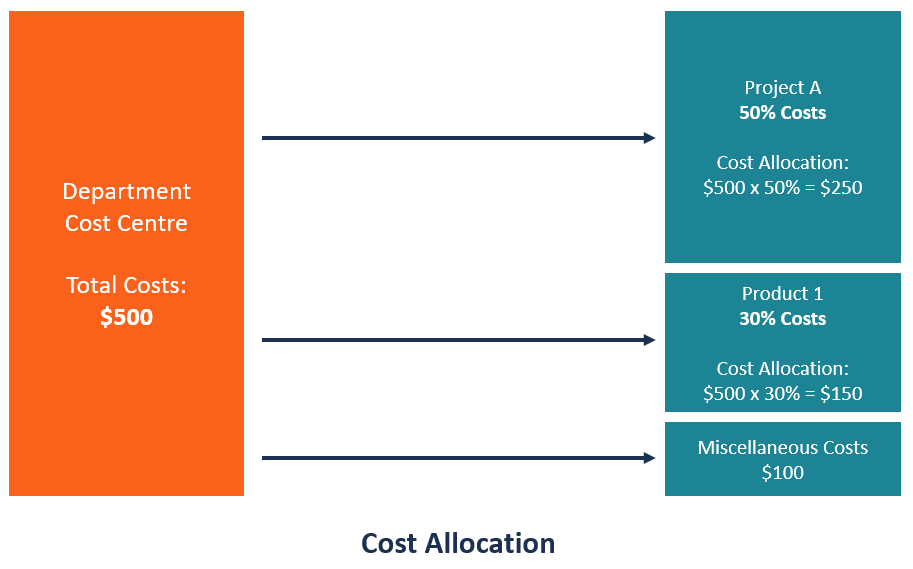

The process of identifying, accumulating, and assigning costs to costs objects

Cost allocation is the process of identifying, accumulating, and assigning costs to costs objects such as departments, products, programs, or a branch of a company. It involves identifying the cost objects in a company, identifying the costs incurred by the cost objects, and then assigning the costs to the cost objects based on specific criteria.

When costs are allocated in the right way, the business is able to trace the specific cost objects that are making profits or losses for the company. If costs are allocated to the wrong cost objects, the company may be assigning resources to cost objects that do not yield as much profit as expected.

There are several types of costs that an organization must define before allocating costs to their specific cost objects. These costs include:

Direct costs are costs that can be attributed to a specific product or service, and they do not need to be allocated to the specific cost object. It is because the organization knows what expenses go to the specific departments that generate profits and the costs incurred in producing specific products or services. For example, the salaries paid to factory workers assigned to a specific division are known and do not need to be allocated again to that division.

Indirect costs are costs that are not directly related to a specific cost object, like a function, product, or department. They are costs that are needed for the sake of the company’s operations and health. Some common examples of indirect costs include security costs, administration costs, etc. The costs are first identified, pooled, and then allocated to specific cost objects within the organization.

Indirect costs can be divided into fixed and variable costs. Fixed costs are costs that are fixed for a specific product or department. An example of a fixed cost is the remuneration of a project supervisor assigned to a specific division. The other category of indirect cost is variable costs, which vary with the level of output. Indirect costs increase or decrease with changes in the level of output.

Overhead costs are indirect costs that are not part of manufacturing costs. They are not related to the labor or material costs that are incurred in the production of goods or services. They support the production or selling processes of the goods or services. Overhead costs are charged to the expense account, and they must be continually paid regardless of whether the company is selling goods or not.

Some common examples of overhead costs are rental expenses, utilities, insurance, postage and printing, administrative and legal expenses, and research and development costs.

The following are the main steps involved when allocating costs to cost objects:

The first step when allocating costs is to identify the cost objects for which the organization needs to separately estimate the associated cost. Identifying specific cost objects is important because they are the drivers of the business, and decisions are made with them in mind.

The cost object can be a brand, project, product line, division/department, or a branch of the company. The company should also determine the cost allocation base, which is the basis that it uses to allocate the costs to cost objects.

After identifying the cost objects, the next step is to accumulate the costs into a cost pool, pending allocation to the cost objects. When accumulating costs, you can create several categories where the costs will be pooled based on the cost allocation base used. Some examples of cost pools include electricity usage, water usage, square footage, insurance, rent expenses, fuel consumption, and motor vehicle maintenance.

A cost driver causes a change in the cost associated with an activity. Some examples of cost drivers include the number of machine-hours, the number of direct labor hours worked, the number of payments processed, the number of purchase orders, and the number of invoices sent to customers.

The following are some of the reasons why cost allocation is important to an organization:

Cost allocation provides the management with important data about cost utilization that they can use in making decisions. It shows the cost objects that take up most of the costs and helps determine if the departments or products are profitable enough to justify the costs allocated. For unprofitable cost objects, the company’s management can cut the costs allocated and divert the money to other, more profitable cost objects.

Cost allocation helps determine if specific departments are profitable or not. If the cost object is not profitable, the company can evaluate the performance of the staff members to determine if a decline in productivity is the cause of the non-profitability of the cost objects.

On the other hand, if the company recognizes and rewards a specific department for achieving the highest profitability in the company, the employees assigned to that department will be motivated to work hard and continue with their good performance.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

Thank you for reading CFI’s guide to Cost Allocation. In order to help you become a world-class financial analyst and advance your career to your fullest potential, these additional resources will be very helpful: