Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

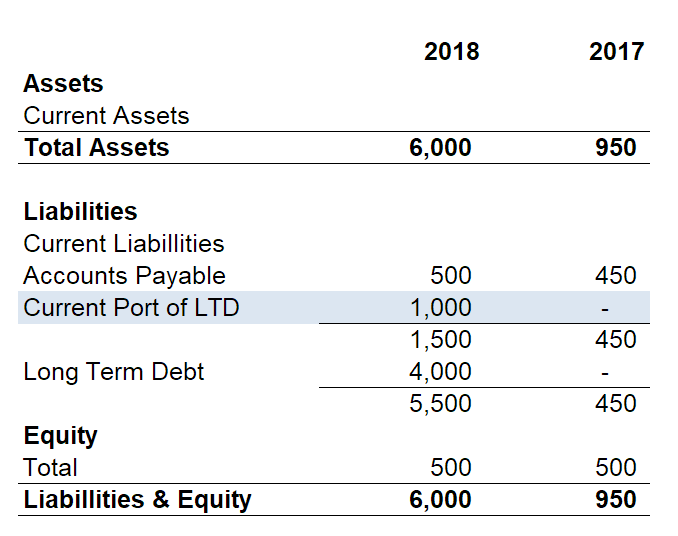

The portion of debt with a maturity of more than one year that is due within a year

Long-term debt is debt with a maturity of longer than one year. This can be anywhere from two years, to five years, ten years, or even thirty years. The current portion of long-term debt is the amount of principal and interest of the total debt that is due to be paid within one year’s time.

This is not to be confused with current debt, which is debt with a maturity of less than one year. Some firms will consolidate the two amounts into a generic current debt line item on the balance sheet.

An analyst should attempt to find information to build out a company’s debt schedule. This schedule outlines the major pieces of debt a company is obliged under, and lays it out based on maturity, periodic payments, and outstanding balance. Using the debt schedule, an analyst can measure the current portion of long-term debt that a company owes.

Borrower Inc. takes on a five-year loan of $5,000,000. The loan terms specify equal payments over the five years. The current portion of this long-term debt is $1,000,000 (excluding interest payments).

A company reduces this line item by making payments toward the debt. As payments are made, the cash account decreases but the liability side decreases an equivalent amount.

Alternatively, a company with good credit standing can “roll forward” current debt, by taking on more credit to pay this loan off. If the new credit taken on is long-term, then the current debt is effectively rolled into the future.

From a cash flow perspective, there is no impact on whether debt is classified as a current liability or non-current liability. In financial modeling, it may be necessary to produce a full set of financial statements, including a balance sheet where the current portion of long-term debt is shown separately.

This is simply to tie the numbers to the accounting records in a way that most accurately reflects the company’s financial position. There is no impact on valuation arising from how the debt is categorized.

To learn more, check out CFI’s financial modeling courses.

CFI is the official provider of the global Financial Modeling & Valuation Analyst (FMVA®) certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional resources below will be useful: