Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

A depreciation rule that assumes the depreciation on a fixed asset is halved for the first and additional last year

The half-year convention for depreciation assumes fixed assets have been in service for one-half of its first year despite when it was actually acquired. This rule is applied by tax authorities to restrict the maximum allowable claim for depreciation to one half of the annual amount.

The other half of the depreciation is applied to the final year the asset is depreciated, also under the assumption that the asset will no longer be used or disposed of halfway through that final year. The half-year convention applies to all forms of depreciation methods, such as straight-line depreciation, sum-of-the-years digits, modified accelerated cost recovery systems, and double-declining balance.

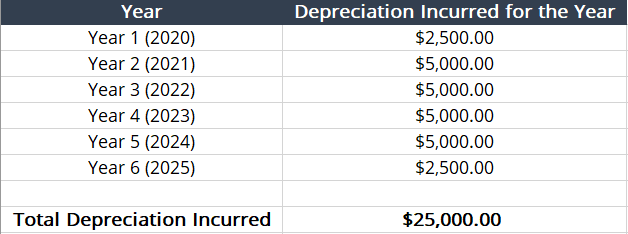

The allocation of depreciation for the half-year convention can be difficult to grasp. To get a better understanding, an example of a half-year convention with a depreciation schedule is shown below.

Example: Company A purchases a manufacturing machine for $25,000 on March 1, 2020. The manufacturing machine’s useful life is five years. With the application of a half-year convention, the depreciation schedule is as follows:

As the table shows, the first year of depreciation is halved due to the half-year convention. To make up for it, an extra year is added to the end of the depreciation schedule.

A depreciation convention is a rule that is used to determine four different criteria:

As a whole, depreciation conventions govern when and how depreciation is calculated.

As for the types of depreciation conventions, nine conventions govern when and how depreciation is calculated. The conventions are listed and discussed below:

How and when depreciation is calculated directly affects an organization’s tax status. A half-year convention does not require taxpayers to prove when the fixed asset was placed into service. Instead, the U.S. Internal Revenue Service (IRS) created a rule that assumes fixed assets are placed into service on July 1st of the year it was actually placed in service.

The IRS created the rule because taxpayers would be enticed to purchase fixed assets in the second half of the year and aggressively claim full depreciation deductions. As for taxpayers, the rule clearly outlines how much depreciation can be deducted in the first year as the asset is assumed to be put into service on July 1st.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

CFI is the official provider of the global Financial Modeling & Valuation Analyst (FMVA®) certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional CFI resources below will be useful: